Is OpenAI today’s earnings canary?

What to look out for today

Companies reporting on Wednesday, 29 April: Abbvie, ADP, Alphabet, Amazon, Etsy, Fiverr, Ford Motor, Lemonade, Markel Group, Meta Platforms, Microsoft, Qualcomm

Key data to move markets today

EU: Spanish Harmonised Index of Consumer Prices, Eurozone Business Climate, Consumer Sentiment and Economic Sentiment Indicator, French GDP, German CPI and German Harmonised Index of Consumer Prices

USA: Building Permits, Durable Goods Orders, Durable Goods ex-Defence Orders, Housing Starts and Nondefence Capital Goods Orders, Fed Interest Rate Decision, Fed Monetary Policy Statement and FOMC Press Conference

Global Macro Updates

FOMC Preview. The April FOMC meeting ends today, with the release of the policy statement at 2:00 pm EDT, followed by a press conference with Fed Chair Powell at 2:30 pm EDT. Market participants are currently assigning an almost certain probability to a decision to maintain rates, with the likelihood of a single dissenting vote, mirroring the outcome of the March meeting.

Analysts on the sell side anticipate that the decision to hold rates will be driven by persistent upward pressures on inflation, largely attributed to ongoing geopolitical conflicts and a robust macroeconomic environment, which includes positive labour market developments and sustained consumer spending.

Several previews suggest that the policy statement may be revised to acknowledge elevated inflation and stronger employment data. Economists at Bank of America noted that forward guidance regarding two-sided risks is expected to remain unchanged, although they suggested it is a close call. A potential modification from ‘any adjustments’ to simply ‘adjustments’ could signal that the next policy move is not necessarily a rate reduction. Jefferies anticipates no significant changes in communication, emphasising that the Fed's March language surrounding risks related to the Iranian conflict remains pertinent.

Jefferies economists expect Chair Powell's remarks to remain consistent, focusing on two-sided risks and the economy's resilience as justification for maintaining current policy. Bank of America also predicts that Powell will adopt a hawkish tone, reaffirming that monetary policy is appropriately positioned to address both labour market conditions and inflationary pressures.

This meeting is likely to be Powell's final appearance as Fed Chair, following the Department of Justice's announcement on Friday that it has closed its criminal investigation into cost overruns at the Fed headquarters. Senator Tillis, a Republican, stated on Sunday that he is now prepared to lift his blockade and support the confirmation of nominee Kevin Warsh as new Fed Chair.

OpenAI fails to meet internal targets, sparking concerns over AI CapEx. Recent media coverage indicates that OpenAI has fallen short of its internal objectives for both user growth and revenue, raising questions about the company’s ability to sustain its substantial investments in data centres. Specific missed targets include a goal of reaching one billion weekly active users by the end of 2025 and meeting revenue expectations, as subscriber attrition to competing AI platforms, such as Google’s Gemini, has eroded market share. Additionally, OpenAI’s monthly revenue targets for this year were not achieved, with Anthropic’s advancements in coding and enterprise solutions gaining traction among users.

According to reports, CFO Sarah Friar has cautioned that OpenAI may be unable to fulfill its computing contract obligations if revenue growth does not accelerate. Furthermore, the board has recently scrutinised the company’s data centre agreements and questioned CEO Sam Altman’s advocacy for increased capital spending in this area, especially given the current slowdown in business momentum.

In light of these developments, shares of companies within the OpenAI ecosystem experienced significant declines. SoftBank, having recently committed $30 billion to OpenAI’s $110 billion funding round in February, saw its stock drop, along with other infrastructure-linked partners such as Oracle, CoreWeave and AMD.

These events coincide with an updated partnership agreement between OpenAI and Microsoft announced the previous day, as reported by Axios. Despite the recent challenges, analysts have generally expressed optimism regarding these deal updates, particularly in view of a potential initial public offering. The revised agreement enables OpenAI to deliver stateful APIs across multiple cloud providers and focus more intently on enterprise licensing, positioning the company to compete more effectively with rivals such as Anthropic.

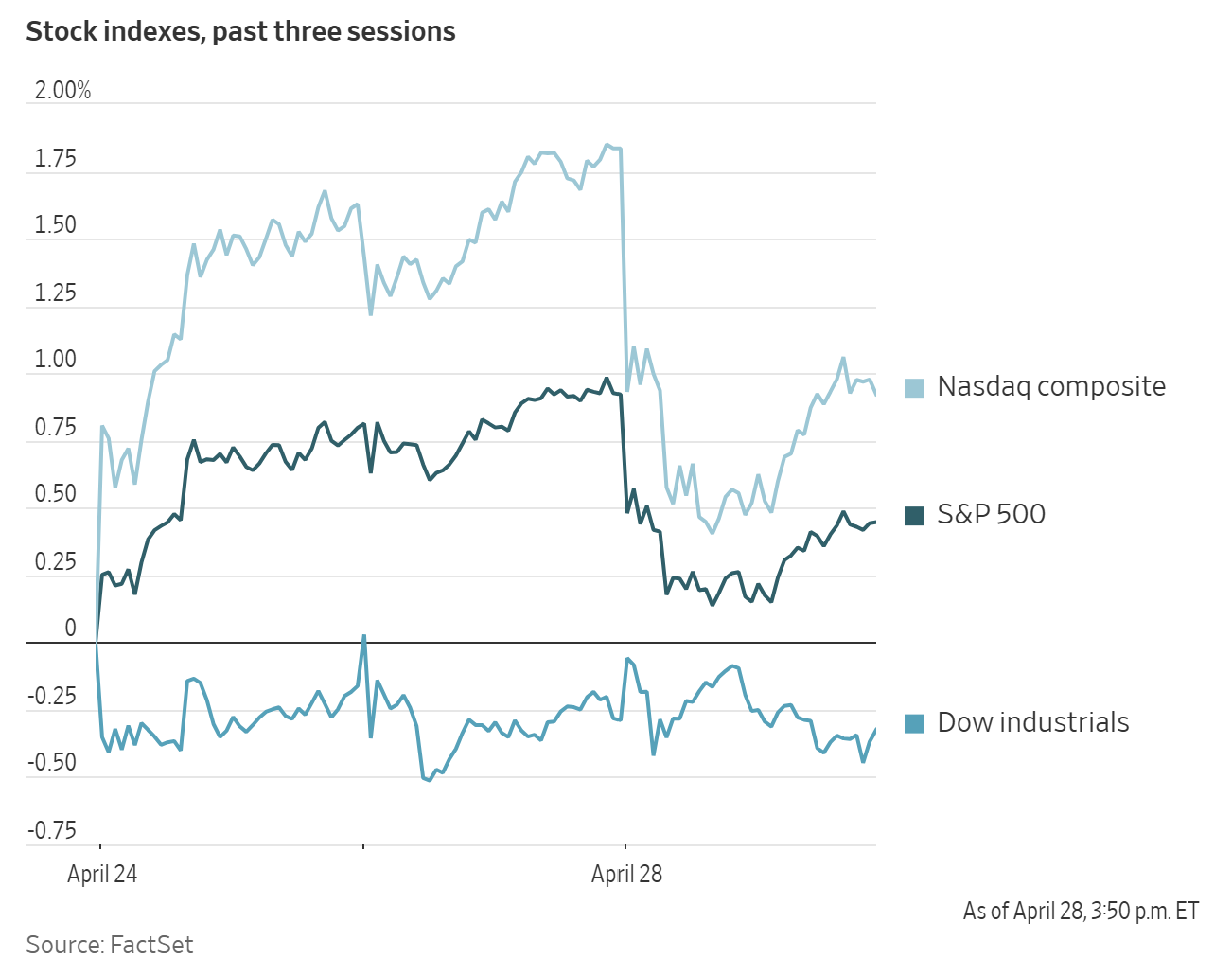

US Stock Indices

Dow Jones Industrial Average -0.05%

Nasdaq 100 -1.01%

S&P 500 -0.49%, with 5 of the 11 sectors of the S&P 500 down

Concerns regarding AI resurfaced on Tuesday on Wall Street. Shares of Oracle, CoreWeave, SoftBank and other companies affiliated with OpenAI experienced notable declines, with each falling at least four percent.

This downturn followed a report from The Wall Street Journal indicating that OpenAI, the developer of ChatGPT, had failed to meet its internal targets for revenue and user growth. These developments renewed investor apprehension about whether large-scale investments in AI by major technology firms will deliver the substantial profits that many anticipate.

The declines in these stocks weighed heavily on the Nasdaq Composite, pulling the index down -0.90% from its record high achieved in the previous session. Technology shares represented the largest losses within the S&P 500, which saw the sector decrease -1.29%. In contrast, the Dow Jones Industrial Average slipped by -0.05%, buoyed by a +3.86% surge in Coca-Cola shares after it reported earnings that surpassed expectations. It was Coca-Cola’s strongest single-day performance since October.

In corporate news, UPS maintained its guidance despite exceeding forecasts for Q1 sales and profits, signalling ongoing uncertainty surrounding the company’s plans to restructure its delivery network.

Coca-Cola’s emphasis on smaller packaging sizes continues to resonate with budget-conscious consumers, enabling the world’s largest beverage producer to achieve sales growth that outpaced expectations in Q1.

Centene reported Q1 net profit that surpassed projections and subsequently raised its annual outlook, marking a positive recovery trend for the US health insurance sector following a challenging year.

Spotify shares declined after the music streaming leader issued an operating income forecast for the second quarter that fell short of analyst estimates.

S&P 500 Best performing sector

Energy +1.65%, with Targa Resources +2.93%, Coterra Energy +2.85% and Kinder Morgan +2.71%

S&P 500 Worst performing sector

Information Technology -1.29%, with Corning -8.90%, Applied Materials -5.87% and Teradyne -5.44%

Mega Caps

Alphabet -0.29%, Amazon -0.52%, Apple +1.15%, Meta Platforms -1.07%, Microsoft +1.04%, Nvidia -1.59% and Tesla -0.67%

Information Technology

Best performer: Workday +2.84%

Worst performer: Corning -8.90%

Materials and Mining

Best performer: Packaging of America +4.73%

Worst performer: Albemarle -6.33%

Corporate Earnings Reports

Posted on Tuesday, 28 April from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Visa reported Q2 net revenue of $11.23 bn beating est $10.74 bn adjusted EPS $3.31 vs est $3.10 and total processed transactions $66.1 bn vs est $66.39 bn. CEO noted 17% net revenue growth highest since 2022 resilient con bn multi-year share buyback plan. Partnered with WeFi to enable self-custodied crypto spending on its network in Europe Asia Latin America.

Robinhood reported Q1 revenue $1.07 bn vs $1.14 bn estimate miss, EPS $0.38 vs $0.39 estimate miss, net income $346 mn vs $354 mn estimate. Total Platform Assets $307 bn +39% YoY, Gold Subscribers 4.3 mn +36% YoY, ARPU $157 +8% YoY. Record prediction contracts $8.8 bn. Expects $100 mn spend supporting Trump Accounts with $50 mn in Q2 on cost-plus basis revenue exceeding costs. CFO noted Q2 strong April volumes.

UPS reported Q1 2026 adjusted EPS $1.07 beating estimates of $1.02-$1.03, revenue $21.0-21.2 bn beating $20.99B estimate. Reaffirmed FY 2026 revenue ~$89.7 bn and CAPEX ~$3.0 bn. Expects return to revenue, operating profit growth and adjusted operating margin expansion in Q2. Posted lower Q1 profit amid scaling down Amazon deliveries. Previously announced 30,000 operational job cuts and begun filing for tariff refunds.

Coca-Cola reported Q1 adjusted EPS $0.86 vs est $0.81 beat, Revenue $12.5 bn vs est $12.25 bn beat, unit case volume +3% vs est +1.09%, price/mix +2%. Organic growth +10%. Raised FY organic revenue guidance to +4-5% vs est +4.68%, comparable EPS to +8-9%.

Corning reported Q1 2026 adjusted EPS $0.70 beating estimate $0.69 and revenue $4.35 bn beating estimate $4.30 bn ahead of market open. Company guides Q2 adjusted EPS $0.73 to $0.77 versus estimate $0.76.

Spotify reported Q1 revenue $5.30 bn beating est. $5.29 bn, EPS $4.03 vs. est. $3.45, MAUs 761 mn vs. est. 759 mn, ad-supported MAUs 483 mn up 14% YoY, operating income up 40% YoY. Q2 guidance revenue $5.61 bn vs. est. $5.58 bn, MAUs 778 mn vs. est. 774 mn, but operating income $737 mn vs. est. $788 ,mn and subscriber net adds 6 mn vs. est. 7 mn. Peloton announced global partnership to integrate 1,400 fitness classes for Premium subscribers.

General Motors reported Q1 2026 with adjusted EPS of $3.70 versus estimate $2.60, revenue $43.6 bn versus $43.4 bn estimate, North America adjusted EBIT $3.66 bn versus $2.43 bn estimate. Raised FY26 adjusted EPS guidance to $11.50-$13.50 from $11-$13, adjusted EBIT to $13.5 bn-$15.5 bn from $13 bn-$15 bn, amid $500 million tariff refund. Expects gross tariff costs of $2.5 bn-$3.5 bn in 2026. CEO noted no changes in consumer car shopping due to gas prices.

European Stock Indices

CAC 40 -0.46%

DAX -0.27%

FTSE 100 +0.11%

Commodities

Gold spot -1.87% to $4,594.51 an ounce

Silver spot -3.22% to $73.07 an ounce

West Texas Intermediate +2.35% to $99.62 a barrel

Brent crude +2.65% to $111.16 a barrel

Gold declined to a near four-week low on Tuesday, with spot gold falling -1.87% to $4,594.51 per ounce after reaching its lowest point since 2 April earlier in the session.

According to data released by the Hong Kong Census and Statistics Department on Tuesday, China, the world’s largest gold consumer, imported a net total of 47.866 metric tons of gold from Hong Kong in March, an increase from 46.249 tons in February.

Spot silver dropped -3.22% to $73.07 per ounce.

Oil prices closed more than two percent higher on Tuesday, as persistent concerns over supply disruptions from the closure of the Strait of Hormuz outweighed apprehensions regarding the United Arab Emirates’ (UAE) decision to withdraw from OPEC and the broader OPEC+ alliance.

Brent crude futures for June settled up $2.87, or +2.65%, at $111.16 per barrel, marking their seventh consecutive day of gains. Meanwhile, US WTI futures for June rose $2.29, or +2.35%, to $99.62 per barrel, briefly exceeding $100 earlier in the session for the first time since 13 April.

Iran is reportedly preparing a revised peace proposal after Washington rejected its latest offer. The US President stated that Iran contacted his administration, indicating the country is ‘in a state of collapse’ and expressing a desire to reopen the Strait as soon as possible. However, oil prices remained unaffected by these remarks.

The UAE announced its departure from OPEC/OPEC+ effective 1 May. In an official statement, the UAE explained that this decision follows a thorough review of its production policy and capacity, emphasising national interests and a commitment to addressing market needs. The current OPEC+ quota for the UAE in May stands at 3.447 million barrels per day (bpd), with nationwide production capacity projected to reach 5.0 million bpd by 2027.

Meanwhile, companies and countries, including Sweden, continue to prepare for potential jet fuel shortages.

According to AAA, the national average price for a gallon of regular gasoline reached a more than four-year high today.

Ukraine launched another overnight attack on Russia’s Tuapse refinery, resulting in a significant fire.

Ship-tracking data revealed considerable disruptions in the Strait of Hormuz region, with six Iranian oil tankers forced to return due to the US blockade, although some vessel traffic continues.

On Tuesday, the Idemitsu Maru, a Panama-flagged tanker carrying two million barrels of Saudi oil, and a liquefied natural gas (LNG) tanker operated by the UAE’s Abu Dhabi National Oil Company (ADNOC) successfully transited the Strait. The ADNOC vessel was the first loaded LNG tanker to cross since the onset of the Iran conflict on 28 February.

Vortexa data shows that as of 24 April, the volume of crude oil held on stationary tankers worldwide for at least seven days increased to 153.11 million barrels, the highest level since January and a 25% rise from 122.60 million barrels on 17 April.

Note: As of 4 pm EDT 28 April 2026

Currencies

EUR -0.07% to $1.1712

GBP -0.18% to $1.3510

Bitcoin -0.56% to $76,361.41

Ethereum +0.13% to $2,290.51

On Tuesday, the US dollar strengthened as risk-off sentiment stemming from the ongoing conflict with Iran outweighed a brief surge in the yen, which followed the BoJ's most divided policy decision to date under Governor Kazuo Ueda.

While the BoJ maintained its policy rate at 0.75%, an unusual 6 – 3 split, the widest margin since Governor Ueda assumed office, sparked speculation regarding a potential rate hike as early as June. The yen initially appreciated, but subsequently weakened after Governor Ueda's press conference, which tempered the growth outlook. As a result, the yen ended the session -0.11% lower at ¥159.54 per dollar.

The US dollar index broke a two-day losing streak, rising +0.15% to 98.63.

The euro declined -0.07% to $1.1712 and the British pound fell -0.18% to $1.3510. The BoE and the ECB are scheduled for key policy meetings this Thursday, presenting additional central bank risk events for the week.

Fixed Income

US 10-year Bond +0.8 basis points to 4.353%

German 10-year Bund +3.3 basis points to 3.074%

UK 10-year gilt +6.7 basis points to 5.040%

On Tuesday, US Treasury yields reached a three-week high.

The yield on the two-year note, which often reflects Fed fund rate expectations, increased +4.4 bps to 3.850%. The yield on the US 10-year note rose +0.8 bps to 4.353%. On the long-end, the 30-year yield declined -1.3 bps to 4.939%.

The yield curve between the two-year and 10-year notes flattened by 3.6 bps to 50.3 bps.

The Treasury reported solid demand for $44 billion in seven-year notes on Tuesday, concluding the week's issuance of $183 billion in short- and intermediate-term debt. The notes were sold at a high yield of 4.175%, which was 0.5 bps above the pre-auction level. The bid-to-cover ratio reached 2.51x, the highest since December.

Monday's $69 billion two-year note auction attracted average demand, while interest was comparatively subdued for the $70 billion five-year note sale.

Market participants are expecting the FOMC meeting to end with policymakers maintaining current rates as they weigh the risks posed by elevated inflation against signs of softness in the labour market.

This week's FOMC meeting marks the final session with Jerome Powell as Fed Chair. On Wednesday, the Senate Banking Committee is set to advance Kevin Warsh's nomination for Fed Chair to the full Senate, with a vote scheduled for 10 am EDT.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 4.7 bps of rate cuts in 2026, lower than the 8.4 bps priced in a week ago.

On Tuesday, eurozone bond yields reached multi-week highs following a survey indicating that consumers in the region anticipate higher inflation.

The ECB survey revealed that inflation expectations for one year ahead surged to 4.0% in March from 2.5% the previous month, while expectations for three years ahead rose to 3.0% from 2.5%. Both figures remain well above the ECB’s 2% target.

Investors now perceive a greater likelihood that the ECB will raise interest rates to prevent rising oil and gas prices from triggering broader price increases, despite the potential negative effects on economic growth.

Germany’s rate-sensitive two-year yield climbed to 2.667%, marking its highest level since 7 April, and settled +6.3 bps higher at 2.641%.

The yield on Germany’s 10-year note advanced to 3.086% during the session, a two-week peak, and was +3.3 bps higher on the day at 3.074%.

Markets are presently pricing in an approximately 85% probability that the ECB will increase rates by its June meeting and fully anticipate two 25 bps rate hikes by September. This expectation is marginally higher than prior to the release of the survey.

Other eurozone yields also rose in tandem with Germany’s. Italy’s 10-year yield increased +4.4 bps to 3.882%, expanding the spread over Bunds to 80.8 bps, which is 1.1 bps higher than the previous day.

Note: As of 4 pm EDT 28 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

هذه المقالة متاحة لأغراض معلوماتية فقط، ولا ينبغي اعتبارها عرضًا أو التماسًا لعرض شراء أو بيع أي استثمارات أو خدمات ذات صلة يمكن الإشارة إليها هنا. ينطوي التداول في الأدوات المالية على مخاطر كبيرة من الخسارة وقد لا يكون مناسبًا لجميع المستثمرين. الأداء السابق ليس مؤشرًا موثوقًا به للأداء المستقبلي.

أنشأها المتخصصون. للمحترفين.