How long can the AI boom boost growth?

What to look out for today

Companies reporting on Friday, 1 May: Anglogold Ashanti, Chevron, Colgate-Palmolive, Church & Dwight, Dominion Energy, ExxonMobil

Key data to move markets today

JAPAN: Tokyo CPI

EU: European Markets closed for Labour Day Holiday

UK: S&P Global Manufacturing PMI and a speech by BoE Chief Economist Huw Pill

USA: ISM Manufacturing Employment Index, New Orders Index, Manufacturing PMI and Manufacturing Prices Paid

Global Macro Updates

US GDP grows as labour markets continue to show strength. US GDP picked up in Q1 at a 2% annualised rate as it rebounded on government spending following last year’s government shutdown. The AI spending boom and the building of data centres helped to lift business spending on equipment, which increased at a 17.2% rate after rising at a 4.3% pace in the fourth quarter. However, this GDP growth may prove to be only temporary as inflation expectations rise. The personal consumption expenditures price index increased at a 4.5% pace last quarter, the fastest since the Q3 2022. PCE inflation rose 3.5% y/o/y in March, the biggest rise since May 2023, a separate report from the Bureau for Economic Analysis (BEA) showed on Wednesday.

Meanwhile, jobless claims plunged to the lowest level since 1969 in a sign that job-cut announcements have not yet meaningfully translated into layoffs. Initial claims fell by 26,000 to 189,000 in the week ended 25 April, according to Labor Department data released Thursday. Continuing claims, a proxy for the number of people receiving benefits, dropped to 1.79 million in the previous week, the lowest in two years. However, wages and salaries, adjusted for inflation, rose only 0.1% in the 12 months through March, after increasing 0.7% year-on-year in December, another report from the Labor Department showed. As noted by Reuters, consumers have relied on savings or have been saving less to maintain their spending. The savings rate dropped to 3.6% in March, the lowest level since October 2022, the BEA reported.

ECB and BoE leave rates unchanged on inflation fears. The ECB left interest rates unchanged, as expected, with the benchmark rate at 2%, but extensively debated a hike to combat soaring inflation, which rose to 3% in April, well above the ECB's 2%. ECB President Christine Lagarde said the decision to hold rates was unanimous, but that a hike was discussed. She signalled the ECB will consider a possible interest-rate hike in June given that inflation developments were moving away from the ECB's 'baseline' projection, which already embeds market projections for two hikes. In its statement the ECB warned that “the upside risks to inflation and the downside risks to growth have intensified.” ECB policymakers also noted that “the longer the war continues and the longer energy prices remain high, the stronger is the likely impact on broader inflation and the economy.”

After an 8-1 vote, with only BoE Chief Economist Huw Pill dissenting in favour of a 25 bps rise, the BoE kept the benchmark rate at 3.75%. BoE Governor, Andrew Bailey, said holding rates was a “reasonable place” to be, given the softness in the UK economy. However, he suggested they may need to rise in the event of continued substantial disruption to energy supplies. “Where we go from here will depend on the size and duration of the shock to energy prices,” he said. The BoE now expects Q3 inflation to be 1.4% higher than it forecast in February’s outlook report, prior to the Iran war.

Instead of providing a central inflation projection, the Bank outlined three scenarios, with the worst-case scenario being one in which the price of oil rose above $130 a barrel and remained elevated for a prolonged period. It predicted that if this happened, inflation would probably peak at 6% by the start of 2027, unemployment would rise to 5.6% and interest rates would have to rise to 5.25% to combat this.

Governor Bailey also noted during the press conference that traders had gotten ahead of themselves after the BoE’s March meeting, at one stage pricing in as many as four or five rate increases. He said that the market is now no longer “in the wrong place.” After the meeting, money markets trimmed wagers on the extent of BoE hikes this year, pricing around two hikes and more than a 50-50 chance of a third.

The Bank of Japan, the US Federal Reserve and the Bank of Canada all also left rates unchanged this week, even while expressing concerns over inflation.

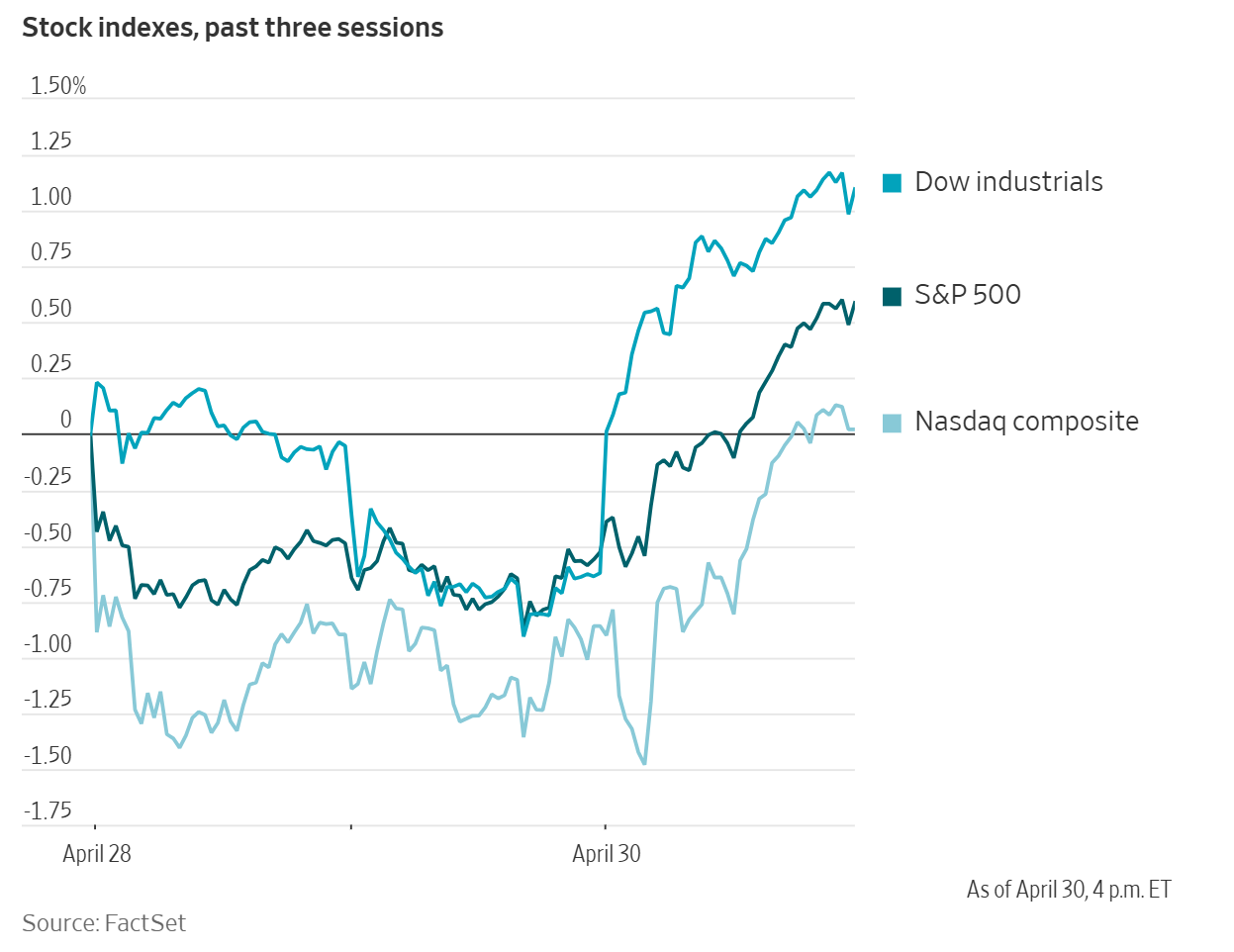

US Stock Indices

Dow Jones Industrial Average +1.62%

Nasdaq 100 +0.98%

S&P 500 +1.02%, with 10 of the 11 sectors of the S&P 500 down

The Nasdaq composite and the S&P 500 ended April at fresh highs as strong US growth data fuelled investor optimism about the outlook for corporate earnings. The Nasdaq composite ended April with a +15.29% gain, its best month since early 2020. The S&P 500 also closed its best month since 2020 and was +10.42% for the month.

The Dow Jones Industrial Average rose 790.33 points, or +1.62% to 49,652.14 points on Thursday. The S&P 500 was up 73.05 points, or +1.02%, to 7,209.00 and the Nasdaq Composite climbed 219.07 points, or +0.89%, to 24,892.31.

In corporate news, Eli Lilly & Co. raised its annual sales and profit forecast due to the increasing demand for obesity medications with its new weight-loss pill seeing huge interest before advertising for the drug had even started.

Apple reported results on Thursday that beat estimates due to continued demand for the new MacBook model driven by incoming CEO John Ternus, while supply constraints hindered iPhone sales. Apple said sales and profits were $111.18 billion and $2.01 per share for the fiscal second quarter ended 28 March. Sales of the iPhone were $56.99 billion, slightly less than estimates of $57.21 billion, according to LSEG data.

Mastercard warned that overseas spending growth on the firm’s cards had weakened in recent weeks.

Ford Motor warned of pressure from an unexpected rise in commodity costs, spooking investors even as the automaker raised its full-year profit outlook on demand for high-margin pickups and SUVs.

S&P 500 Best performing sector

Communication Services +3.98%, with Alphabet +9.96%, Charter Communications +4.11% and Verizon +3.05%

S&P 500 Worst performing sector

Information Technology -0.63%, with Meta Platforms -8.55%, Nvidia -4.63% and Tyler Technologies -4.18%

Mega Caps

Alphabet +9.96%, Amazon +0.77%, Apple +0.44%, Meta Platforms -8.55%, Microsoft -3.93%, Nvidia -4.63% and Tesla +2.37%

Information Technology

Best performer: Qualcomm +15.12%

Worst performer: Meta Platforms -8.55%

Materials and Mining

Best performer: CRH +4.39%

Worst performer: International Paper -9.41%

Corporate Earnings Reports

Posted on Thursday, 30 April from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Apple Q2 FY26 revenue $111.2 bn beating $109.6 bn consensus. EPS $2.01 beating $1.96. iPhone revenue $56.99 bn, up 21.7% y/o/y for second straight quarter over 20% growth; Services $30.98 bn, up 16.3% y/o/y Products $80.2 bn, up 17% y/o/y. Greater China revenue $20.5 bn, beating $18.91 bn est. Company boosted quarterly dividend to $0.27/share from $0.26 and authorised additional $100 bn share buyback. CEO Tim Cook stated it was Apple's best March quarter ever with double-digit growth across segments fueled by extraordinary iPhone 17 demand.

SanDisk Q3 earnings after close with revenue of $5.95 bn vs estimates of $4.73 bn and EPS of $23.41 versus $14.66, alongside operating income of $4.2 bn vs $2.7 bn expected. Q4 guidance raised to revenue of $8.1 bn vs $6.6 bn estimates and EPS of $31.50 versus $23.44. SanDisk CEO stated 'This quarter marks a fundamental inflection point for Sandisk.'

Western Digital Q3 revenue of $3.34 bn beating estimates of $3.25 bn and adjusted EPS of $2.72 vs $2.39 expected. It guided Q4 revenue to $3.65 bn above $3.46 bn consensus and operating expenses to $385 mn - $395 mn. The company also plans to boost its quarterly dividend by 20%.

Reddit Q1 revenue of $663 mn beating $610 mn consensus. EPS of $1.01 missing $1.09 estimate, EBITDA of $266 mn, topping $226 mn forecast. DAUs of 126.8 mn exceeding 121.1 mn est and ARPU of $5.23, up 44% y/o/y. Q2 guidance includes revenue of $720 mn above $716 mn est and EBITDA of $290 mn over $283 mn est. Reddit CEO stated 'Reddit is a one-of-one business powered by deeply engaged communities and authentic human conversation. That foundation is driving a rare combination of growth, profitability & efficiency, and giving Reddit a unique advantage in the age of AI.'

Amgen Q1 revenue of $8.62 bn vs Wall Street consensus of $8.57 bn and adjusted EPS of $5.15 versus $4.75. The company raised FY adjusted EPS guidance to $21.70-$23.10 from $21.60-$23.00 and FY revenue guidance to $37.1 bn - $38.5 bn from $37 bn - $38.4 bn.

Bristol-Myers Squibb Q1 revenue of $11.49 bn, beating estimates of $10.91 bn, and adjusted EPS of $1.58 versus $1.42 expected. Worldwide Eliquis revenue was $4.14 bn, up 16% y/o/y. The company reaffirmed its 2026 financial guidance. Bank of America maintained a Buy rating and Guggenheim maintained a Buy rating. Bristol-Myers announced its alliance with Pfizer is partnering with Mark Cuban Cost Plus Drug Company to offer Eliquis.

Merck Q1 sales of $16.29 bn versus Wall Street consensus of $15.83 bn and adjusted loss per share of $1.28 vs expected loss of $1.51. Keytruda revenue reached $8.03 bn, up 12% y/o/y, while Gardasil revenue was $1.07 bn vs estimates of $1.04 bn. The company adjusted FY adjusted EPS guidance to $5.04-$5.16 from prior $5.00-$5.15 and FY sales guidance to $65.8 bn -$67 bn from $65.5 bn - $67.8 bn.

Mastercard Q1 adjusted EPS of $4.60, beating estimates of $4.40, and net revenue of $8.40 bn versus $8.25 bn expected. Net revenue grew 16% y/o/y, with payment network revenue up 12% driven by 7% gross dollar volume increase to $2.7 trn, 13% cross-border volume growth, and 9% rise in switched transactions. Value-added services revenue surged 22%. The company announced plans to acquire BVNK to expand stablecoin solutions and repurchased $4 bn in stock during the quarter plus $1.7 bn through April 27, with $11.7 bn remaining in authorisation. CEO Michael Miebach stated, "Mastercard is 'diversified, future-ready, and delivering,' highlighting growth beyond traditional card payment.”

Eli Lilly Q1 earnings: adjusted EPS of $8.55 beating consensus estimates of $6.66-$6.97, revenue of $19.8 bn vs. $17.6 bn-$17.8 bn expected, driven by Mounjaro revenue of $8.66 bn (est. $7.21 bn) and Zepbound $4.16 bn (est. $4.03 bn), up from $3.34 adj. EPS y/o/y. Company raised FY2026 revenue guidance to $82-85 bn from $80-83 bn and adj. EPS to $35.50-37 from $33.50-35. CEO stated 2026 started strong with 56% Q1 revenue growth and highlighted FDA approval of Foundayo GLP-1 pill with over 20,000 users. FDA proposed excluding Lilly weight-loss drugs from bulk compounding list.

Valero Energy Q1 earnings: revenue of $32.381 bn beating Wall Street consensus of $30.729 bn and adjusted EPS of $4.22 versus estimates of $3.16.

Caterpillar Q1 revenue of $17.42 bn, beating estimates of $16.24 bn, and adjusted EPS of $5.54, surpassing $4.63 consensus. Adjusted operating income reached $3.13 bn vs $2.74 bn expected, with financial revenues at $942 mn against $895.8 mn forecast. The company guided for low double-digit fiscal year sales and revenues growth and higher Q2 sales and revenues vs Q2 2025. CEO stated the team delivered a strong start to the year with solid sales and revenues growth, robust order activity, and a record backlog providing a strong foundation for continued positive momentum.

ConocoPhillips Q1 adjusted EPS of $1.89 beating Wall Street consensus of $1.72, adjusted net income of $2.3 bn vs $2.07 bn expected, total revenue and other income of $16.05 bn against $15.38 bn forecast, while cash flow from operations was $4.30 bn, missing $5.06 bn estimate. Production averaged 2,309 mboed. Company guided FY production at 2.295-2.325 mmboed, Q2 production at 2.185-2.215 mmboed, and FY capex at $12B-$12.58B

European Stock Indices

CAC 40 +0.53%

DAX +1.41%

FTSE 100 +1.62%

Commodities

Gold spot +1.53% to $4614.70 an ounce

Silver spot +2.90% to $74.18 an ounce

West Texas Intermediate -1.69% to $105.07 a barrel

Brent crude -3.41%, to $114.01 a barrel

Gold rose on Thursday due to a softer US dollar and easing oil prices, but saw its second straight monthly decline due to increasing inflation fears from the ongoing war with Iran and the “higher for longer“ rate environment.

Spot gold was +1.53% to $4,614.70 per ounce. However, it was -0.71% for the month.

Spot silver was also up on Thursday, +2.90% to $74.18 per ounce.

Oil trading was volatile on Thursday, with Brent futures hitting a four-year high of $126.41 a barrel, the highest since 9 March 2022, before settling down $4.02, or -3.41%, to $114.01 after rising for eight consecutive sessions. WTI crude futures closed down $1.81, or -1.69%, at $105.07. The contract reached $110.93 earlier in the trading session, the highest since 7 April. The extreme volatility was attributed to the monthly expiry of Brent futures on Thursday and President Trump telling oil executives that the blockade on the Strait of Hormuz could last for months. Axios reported President Trump was set to be briefed on new military options including a “short and powerful” wave of strikes on Iran aimed at breaking the deadlock in peace talks.

Iran said it would respond with "long and painful strikes" on US positions if Washington renewed attacks. It also reasserted its control over the Strait of Hormuz.

Note: As of 4 pm EDT 30 April 2026

Currencies

EUR +0.51% to $1.1733

GBP +0.98% to $1.3608

Bitcoin +0.9% to $76,366.62

Ethereum +0.9% to $2,260.51

On Thursday, the US dollar fell sharply against the Japanese yen and other major currencies with the US dollar index falling -0.88% to 98.09.

The euro rose +0.51% against the dollar to $1.1733 after the ECB kept rates on hold despite eurozone inflation surging to an estimated 3% in April, well above the ECB 2% target.

In an 8-1 vote, with only BoE Chief Economist Huw Pill voting for a 25 bps rise, the MPC of the Bank of England also kept the benchmark interest rate on hold at 3.75% and set out scenarios for the economic impact of the Iran war. Sterling was +0.98% to $1.3608.

Japanese Finance Minister Satsuki Katayama said earlier on Thursday the time to take"decisive" action in the market was nearing; her strongest signal yet of potential market intervention to prop up the sagging yen.

Japan intervened to prop up the yen against the US dollar on Thursday, its first official currency action in nearly two years after the dollar hit ¥160.725, its highest level against the yen since July 2024. After the intervention it rose as much as 3% against the dollar before ending the trading day +2.4% at ¥156.56 per dollar

Fixed Income

US 10-year Bond -2.4 basis points to 4.389%

German 10-year Bund -5.4 basis points to 3.032%

UK 10-year gilt -4.4 basis points to 5.033%

On Thursday US Treasury yields fell on the shorter end after Q1 GDP expanded by less than expectations. The Commerce Department reported Thursday that Q1 GDP came in at a 2% seasonally adjusted annualised pace in the first quarter, up from 0.5% in the fourth quarter of 2025, but lower than a consensus estimate of 2.2% growth. The yield on the two-year note, which often reflects Fed fund rate expectations, fell -4.6 bps to 3.885%. The yield on the US 10-year note was -2.4 bps to 4.389%. On the long-end, the 30-year yield edged up +0.3 bps to 4.990%.

The yield curve between the two-year and 10-year notes widened by 2.2 bps to 50.4 bps from Wednesday’s 48.2 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in bps of rate cuts in 2026, lower than the bps priced in a week ago.

Across the pond, in the UK, gilts rallied with the 10-year gilt declining -4.4 bps to 5.033%, the 30-year falling -2.4 bps to 5.672%, and the 2-year yield also down, -5.6 bps to 4.445%.

On Thursday, eurozone bond yields fell as oil prices cooled from four-year highs following a sharp surge earlier in the day and the ECB kept rates at 2% for a third straight meeting. Inflation rose to 3% from March’s 2.6% due to a significant leap in energy prices and growth slowed in Q1. Eurostat stated that the eurozone grew by a mere 0.1% in the first quarter, down from 0.2% in the final months of 2025.

The ECB warned that the war in the Middle East has intensified upside risks to inflation and downside risks to growth. After the ECB meeting, money markets priced in around 75 basis points of ECB hikes over the next year, with the first step fully priced in by July and the second by September.

The yield on Germany’s 10-year note fell -5.4 bps to 3.032%, while at the long end, the 30-year yield was -3.7 bps to 3.540%. The 2-year Schatz, considered more sensitive to ECB policy moves, declined -6.0 bps to 2.636%.

Other eurozone yields also fell. Italy’s 10-year yield declined -6.6 bps to 3.857%. The spread over Bunds narrowed to 82.5bps, which was 1.2 bps lower than the previous day.

Note: As of 4 pm EDT 30 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

هذه المقالة متاحة لأغراض معلوماتية فقط، ولا ينبغي اعتبارها عرضًا أو التماسًا لعرض شراء أو بيع أي استثمارات أو خدمات ذات صلة يمكن الإشارة إليها هنا. ينطوي التداول في الأدوات المالية على مخاطر كبيرة من الخسارة وقد لا يكون مناسبًا لجميع المستثمرين. الأداء السابق ليس مؤشرًا موثوقًا به للأداء المستقبلي.

أنشأها المتخصصون. للمحترفين.