What will it take to get both sides to the table?

Key data to move markets today

US: NY Empire State Manufacturing Index and Industrial Production

CHINA: Industrial Production, Retail Sales and Monthly Budget Statement

Global Macro Updates

Attention shifts to strategy and barriers to a swift resolution. As reported by The Wall Street Journal, according to Arab diplomats, Iranian leaders have become increasingly confident in their capacity to disrupt global oil shipments and have established stringent preconditions for any resumption of diplomatic negotiations. These conditions include an immediate cessation of airstrikes and robust assurances against future attacks. However, Iranian Foreign Minister Abbas Araghchi denied seeking talks or a ceasefire with the US.

Diplomatic efforts have reportedly been focused on persuading all parties, namely the US, Israel, and Iran, to agree to a ‘period of calm’, which could serve as a foundation for progressing towards an actual ceasefire.

This intensified diplomatic activity coincides with Iran escalating its retaliatory actions in the Strait of Hormuz, including attacks on tankers, the deployment of naval mines, attacks on neighbouring Arab states, and other actions. Military strategists contend that a diplomatic approach may represent the only sustainable solution for ensuring the Strait remains open, as military measures alone may prove insufficient to deter Iranian aggression.

Within the White House, advisers are deliberating on the timing and manner in which President Trump might proclaim victory, even as the conflict expands. Internal divisions among White House staff and the Republican Party are influencing the President’s messaging and strategic choices regarding the war. The economic team has cautioned against the risks of an oil shock, while political advisers advocate for a restrained military approach. In contrast, more hawkish figures, such as Senators Lindsey Graham and Tom Cotton, are urging President Trump to maintain robust military pressure, as reported by Reuters. Over the weekend President Trump, for the first time, called on world powers, including France, the UK, Japan and China, to help the US reopen the waterway by sending warships to provide escorts to commercial vessels. None of the countries have so far said they’re yet willing to do that. As noted by Bloomberg news, Japan, which rarely wants to appear out of lockstep with the US, said that efforts to escort ships through Hormuz face “high hurdles”, while Australia ruled out sending warships.

January annualised core PCE up; Q4 GDP revised down; January durable orders missed forecasts. In January, headline Personal Consumption Expenditures (PCE) increased by 0.3%, in line with market expectations, following a 0.4% rise in December. Core PCE also rose by 0.4% m/o/m, matching consensus estimates and December’s growth rate. On an annualised basis, headline PCE stood at 2.8%, slightly below the consensus estimate of 2.9% and December’s figure of 2.9%. Conversely, annualised core PCE registered at 3.1%, surpassing the consensus of 2.9% and December’s 3.0%.

US personal spending advanced by 0.4% m/o/m, exceeding the anticipated 0.3% increase and equalling the previous month’s growth. Meanwhile, personal income rose by 0.4% m/o/m, falling short of the consensus estimate of 0.5%, but improving upon December’s 0.3% rise.

The second estimate for Q4 GDP revealed growth of 0.7%, below both the consensus and prior reading of 1.4%. This downward revision was attributed to declines in exports, consumer spending, government expenditure, and investment. The GDP Chain Price Index was recorded at 3.8%, marginally above the consensus of 3.7% and the previous reading of 3.6%. Personal consumption was revised down by 0.4 percentage points to 2.0%.

Durable goods orders for January remained unchanged m/o/m, contrasting with expectations for a 1.2% increase and December’s revised 0.9% decrease. Core orders, excluding defence and aircraft, were also flat, missing the projected 0.5% increase and following December’s unrevised 0.6% growth. Orders excluding transportation rose by 0.4% m/o/m, just below the anticipated 0.5% increase, and December’s revised 1.3% rise. In essence, the data indicates that the US economy was already slowing before the outbreak of the war with Iran. Fed officials are widely expected to hold rates steady this week, with investors focusing on any potential change in the central bank’s outlook amid the war and its expected impact on inflation and the ongoing disruptions in the labour market.

US Stock Indices

Dow Jones Industrial Average -0.26%

Nasdaq 100 -0.62%

S&P 500 -0.61%, with 6 of the 11 sectors of the S&P 500 down

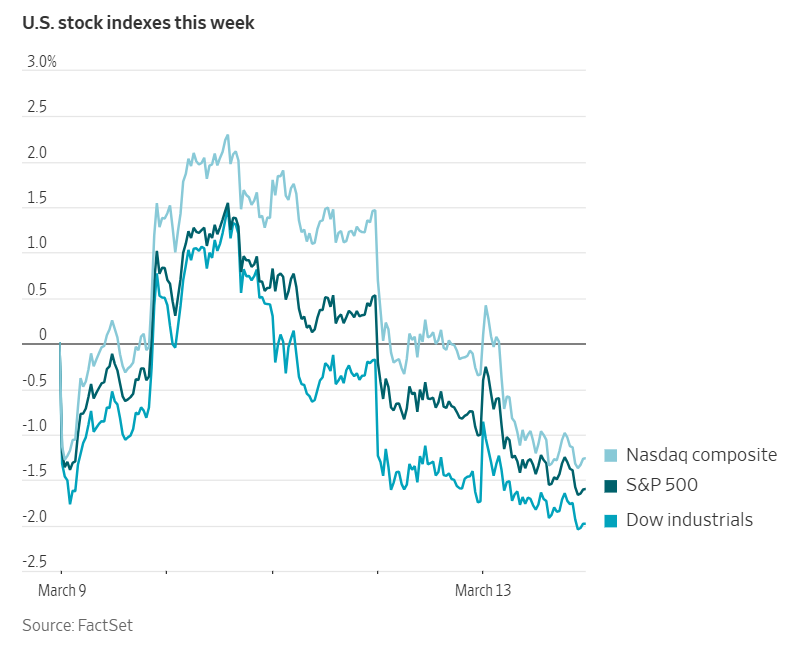

On Friday, US equity markets were down again. The S&P 500 was -0.61% or -40.43 to 6,632.19, the Nasdaq Composite was -0.93% or -206.62 to 22,105.26 and the Dow Jones was -0.26% or 119.38 to 46,558.47 points.

US equity markets declined for a third consecutive week last week, as investors continued to assess the potential ramifications of an extended conflict in the Middle East on global energy prices and overall economic stability. Over last week, the S&P 500 fell -1.60%, the Dow Jones Industrial Average was -1.99%, while the Nasdaq Composite declined -1.26%.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q4 is projected to be +14.1%. This jumps to +14.6% when excluding the Energy sector. Of the 495 companies in the S&P 500 that have reported earnings to date for Q4 2025, 72.5% have reported earnings above analyst estimates, with 72.4% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 9.2% in Q4, increasing to 10.0% when excluding the Energy sector.

Information Technology at 91.5%, is the sector with most companies reporting above estimates. Additionally, Energy and Information Technology, both with a surprise factor of 7.0%, are the sectors that have beaten earnings expectations by the highest surprise factor. Within Materials, 46.2% of companies have reported below estimates. Utilities is the only sector with a negative surprise factor, falling short of estimates by 2.9%. The S&P 500 surprise factor is 4.8%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.1x.

10 S&P 500 companies are scheduled to release their Q4 earnings reports this week.

In corporate news, Apple has announced a reduction in the commission fees levied on app developers in China. This concession in a highly lucrative market comes as the company faces the prospect of antitrust action from domestic regulatory authorities.

Adobe shares declined following the announcement that CEO Shantanu Narayen will step down. The decision comes amid persistent concerns regarding the company's prospects in the rapidly evolving artificial intelligence sector.

Carvana's board has approved a 5-for-1 stock split, a measure designed to make the automotive retailer's shares more accessible to investors after a remarkable multi-year rally since the COVID pandemic's onset.

S&P 500 Best performing sector

Utilities +0.94%, with Xcel Energy +2.10%, Sempra +2.06%, and WEC Energy +2.00%

S&P 500 Worst performing sector

Information Technology -1.29%, with Adobe -7.58%, Broadcom -4.11%, and Salesforce -3.24%

Mega Caps

Alphabet -0.58%, Amazon -0.89%, Apple -2.21%, Meta Platforms -3.83%, Microsoft -1.58%, Nvidia -1.59%, and Tesla -0.96%

Information Technology

Best performer: Micron Technology +5.13%

Worst performer: Adobe -7.58%

Materials and Mining

Best performer: International Paper Company +4.49%

Worst performer: Mosaic -6.54%

European Stock Indices

CAC 40 -0.91%

DAX -0.60%

FTSE 100 -0.43%

Commodities

Gold spot -1.19% to $5,018.43 an ounce

Silver spot -3.53% to $80.55 an ounce

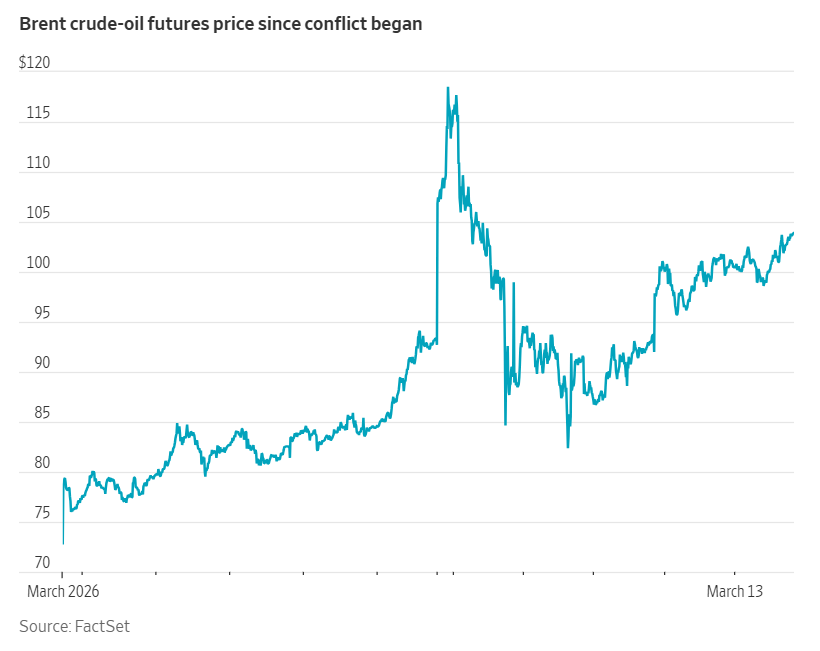

West Texas Intermediate +3.03% to $99.31 a barrel

Brent crude +2.10% to $103.89 a barrel

Gold prices declined on Friday, marking a second consecutive week of losses, primarily due to the strengthening US dollar.

Spot gold dropped -1.19% to $5,018.43 per ounce and registered a weekly decrease of -2.93%.

Although the long-term outlook for gold remains supportive, bullion continues to trend towards its lowest levels since the onset of the Iran conflict, as the dollar hovers near four-month highs.

Spot silver fell -3.53% to $80.55 per ounce, accumulating a weekly loss of -4.48%.

Crude oil futures advanced on Friday, driven by the continued closure of the Strait of Hormuz. Early session losses, prompted by an erroneous report that an Indian-flagged tanker had navigated the strait, which has remained closed since the onset of the conflict, were quickly reversed. Once it became clear that the vessel had departed from Oman without passing through the strait, prices recovered, turning positive before midday.

Brent crude for May delivery settled at $103.89 per barrel, up $2.14, or +2.10%. US WTI crude for April closed at $99.31 per barrel, up $2.92, or +3.03%. Brent was +11.82% from the previous week, while WTI was up +8.81%.

Since the outbreak of the war with Iran, Brent prices have climbed by +41.91%, with WTI advancing +47.59% over the same period.

In response to surging fuel costs and with an eye on the upcoming election, the US has issued a 30-day licence permitting countries to purchase Russian oil and petroleum products currently stranded at sea. Treasury Secretary Scott Bessent described this move as an attempt to stabilise global energy markets destabilised by the US-Israeli-led war with Iran. According to Russia's presidential envoy, Kirill Dmitriev, this measure will impact approximately 100 million barrels of Russian crude, equivalent to nearly a day's global output.

This initiative follows the US Energy Department's announcement of a release of 172 million barrels from the Strategic Petroleum Reserve, intended to mitigate soaring oil prices. This plan is coordinated with the International Energy Agency, which has agreed to release a record 400 million barrels from strategic stockpiles, including the US contribution. However, any brief respite provided by these measures was quickly overshadowed by renewed tensions in the Middle East.

Iran’s new Supreme Leader, Ayatollah Mojtaba Khamenei, has asserted that Iran will persist in its resistance and keep the Strait of Hormuz closed as leverage against the US and Israel. The situation further deteriorated when two fuel tankers in Iraqi waters were reportedly attacked by Iranian boats equipped with explosives, prompting Iraqi officials to confirm a complete halt in operations at the nation's oil ports.

Note: As of 4 pm EDT 13 March 2026

Currencies

EUR -0.83% to $1.1416

GBP -0.94% to $1.3222

Bitcoin +1.12% to $71,114.98

Ethereum +1.96% to $2,103.42

The US dollar appreciated across the board on Friday, positioning itself for a second consecutive week of gains.

The euro depreciated by -0.83% against the dollar, settling at $1.1416, which contributed to a weekly decline of -1.75%. The dollar index advanced by +0.75% on Friday to reach 100.50, bringing its weekly gain to +1.66%.

Market participants are now turning their attention to the upcoming ECB policy meeting scheduled for Thursday, with some traders speculating that the recent surge in oil prices could prompt the central bank to consider raising interest rates later this year.

Against the Japanese yen, the US dollar strengthened to its highest level since July 2024, appreciating +0.24% on Friday to ¥159.71. Over the course of the week, the yen declined -1.22% versus the US dollar.

Japan's Finance Minister, Satsuki Katayama, stated on Friday that the government stands prepared to take appropriate action in response to yen fluctuations that affect citizens' livelihoods, emphasising ongoing close communication with US authorities regarding foreign exchange matters.

The British pound fell -0.94% on Friday, closing at $1.322 and resulting in a cumulative weekly depreciation of -1.41%.

Fixed Income

US 10-year Bond +1.3 basis points to 4.282%

German 10-year +2.5 basis points to 2.986%

UK 10-year gilt +5.8 basis points to 4.771%

On Friday, yields on US Treasury securities diverged, with short-term yields declining while those on the long end of the curve advanced. This movement followed the release of data indicating that the Fed's preferred measure of inflation aligned with economists' expectations for January. Nevertheless, ongoing apprehension regarding elevated oil prices continued to unsettle investors.

The Personal Consumption Expenditures (PCE) price index registered a 0.3% increase in January, following a 0.4% rise in December. When excluding the more volatile food and energy categories, the core PCE price index climbed by 0.4%, mirroring the gain recorded in the preceding month.

The yield on the two-year Treasury note, closely linked to Fed fund rates expectations, declined -1.1 bps to 3.734%. Conversely, the yield on ten-year notes rose +1.3 bps to 4.283%, while the thirty-year yield advanced +1.8 bps to 4.903%.

Over the past week, the 2- and 10-year yields both increased by +15.7 and +14.9 bps, respectively, and the 30-year yield rose +14.2 bps. Since the onset of the conflict, the 2-year yield has climbed +34.7 bps, the 10-year +33.0 bps, and the 30-year +28.5 bps.

During the preceding week, the yield curve, calculated as the differential between the two- and ten-year notes, flattened slightly, narrowing by 0.8 bps to 54.8 bps from 55.6 bps in the prior week.

Mounting concerns over the recent escalation in oil prices have largely overshadowed the release of a weaker-than-anticipated employment report for February.

Additional economic data published on Friday revealed that US economic growth decelerated more sharply in Q4 than previously estimated. Simultaneously, job openings increased in January, though overall hiring remained subdued.

It is widely anticipated that the Fed will maintain its current policy rate at the conclusion of its two-day meeting on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 21.4 bps of cuts in 2026, lower than the 42.3 bps priced in the previous week. Fed funds futures traders are now pricing in a 1.9% probability of a 25 bps rate cut at the FOMC meeting this week, down from 3.5% a week ago.

On Friday, eurozone government bonds experienced their second consecutive weekly decline, as persistent concerns regarding the inflationary effects of the conflict in the Middle East continued to drive yields higher.

France and Italy have initiated discussions with Iran in an effort to secure agreements ensuring the safe passage of their vessels through the Strait, according to a report by the Financial Times. However, Italy has publicly denied the existence of such negotiations.

Money market participants are now assigning a probability greater than 60% to the prospect of an ECB rate hike by June. Prior to the onset of the conflict, expectations indicated only a marginal likelihood of a rate cut within the year.

Germany’s 10-year government bond yield increased +2.5 bps on Friday, reaching 2.986%. This marked a weekly rise of +12.5 bps, following a previous week’s increase of +20.5 bps. The yield on Germany’s two-year Schatz rose +3.1 bps on Friday, amounting to a cumulative rise of +44.0 bps since the commencement of hostilities with Tehran. At the longer end, the increase in yields has been less pronounced; Germany’s 30-year yield advanced +1.7 bps on Friday, contributing to a weekly gain of +11.4 bps and a total increase of +21.6 bps since the conflict began.

Italian government bonds have borne the brunt of the decline in European bond prices. The yield on Italy’s 10-year BTP climbed +3.5 bps to 3.786%. Over the week, it rose +14.8 bps and is now +43.6 bps higher since the start of the conflict. The spread between the 10-year German Bund and Italy’s 10-year BTP widened by 2.3 bps last week to 80.0 bps, after expanding by 10.6 bps since the conflict began.

The French 10-year yield rose +3.5 bps on Friday, contributing to a weekly increase of +13.4 bps and culminating in a total rise of +35.6 bps since the conflict began. Last week, the spread between the 10-year French OAT and German Bund widened marginally, by 0.9 bps to 68.1 bps, marking an increase of 2.6 bps since the conflict began.

Note: As of 4 pm EDT 13 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

هذه المقالة متاحة لأغراض ملعوماتية فقط، ولا ينبغي اعتبارها عرضًا أو التماسًا لعرض شراء أو بيع أي استثمارات أو خدمات ذات صلة يمكن الإشارة إليها هنا. ينطوي التداول في الأدوات المالية على مخاطر كبيرة من الخسارة وقد لا يكون مناسبًا لجميع المستثمرين. الأداء السابق ليس مؤشرًا موثوقًا به للأداء المستقبلي.

Created by professionals. For professionals.