Moving towards escalation?

Key data to move markets today

EU: Eurozone Consumer Confidence and speeches by Bank of Spain’s Governor José Luis Escrivá, ECB’s Board Member Piero Cipollone and Chief Economist Phillip Lane

JAPAN: National CPI and National Core CPI

Global Macro Updates

President Trump may consider occupying Kharg Island; reopening Hormuz remains a top priority. The principal Iran-related development on Friday was a report that the Trump administration is considering taking control of Iran’s Kharg Island crude-export facility to pressure Tehran to reopen the Strait of Hormuz, as reported by Axios. The report notes that such an operation could involve boots on the ground, an approach President Trump pushed back against on Thursday, and could require at least another month of further degrading Iran’s military capabilities.

Energy remains the central focus, given the ongoing closure of Hormuz and Iranian attacks on Middle Eastern oil infrastructure. Earlier today International Energy Agency Executive Director Faitih Birol said that more than 40 energy assets across nine countries in the Middle East have been “severely or very severely” damaged by the war, potentially prolonging disruptions to global supply chains after the conflict ends. Saudi Arabia said its base case anticipates crude rising above $180 per barrel if disruptions persist beyond late April. Reports on Friday also indicated that the US is deploying helicopters and low-flying jets as part of operations to help reopen the strait, while a team of UK military planners is meeting with US Central Command to evaluate options for the waterway. Late on Saturday, US President Trump gave Iran a two-day deadline to reopen the Strait of Hormuz or have its power plants bombed.

US and Israel’s strategies seem potentially divergent, following Israeli strikes on Iran’s energy infrastructure, although Israel’s Prime Minister Netanyahu said his government would honour President Trump’s request not to target Iranian energy sites.

Meanwhile, Iran continued strikes against regional targets. Bloomberg reported that Kuwait closed its Al Ahmadi refinery after multiple strikes, while the UAE and Saudi Arabia both intercepted missiles overnight. On Sunday Iran said it would respond to President Trump’s 48-hour warning by targeting vital infrastructure across the region, including energy facilities and water desalination plants.

Bowman and Waller still see a path to rate cuts this year. In the first Fed remarks following Wednesday’s FOMC decision, Fed Vice Chair for Supervision Michelle Bowman said in an interview with Fox Business that she still expects three rate cuts before year-end and continues to anticipate strong economic growth. She added that it is too early to assess the impacts of the Iran conflict, although she expects some supply-side policies to work their way through the economy.

Speaking to CNBC, Fed Governor Christopher Waller said he remains cautious given current economic conditions and uncertainty surrounding the war with Iran. However, he said he still believes rate cuts are possible later this year if the labour market continues to weaken and inflation remains under control.

Waller also noted that the labour market is not expanding, citing four negative payroll reports out of the past five. He added that he is monitoring inflation closely, particularly whether tariff-linked inflation fails to ease around mid-year, which could create a challenging policy environment for the Fed.

US Stock Indices

Dow Jones Industrial Average -0.96%

Nasdaq 100 -1.88%

S&P 500 -1.51%, with 9 of the 11 sectors of the S&P 500 down

US stocks and bonds fell on Friday after the Pentagon dispatched three additional warships and a new deployment of Marines to the region, heightening concerns that the conflict with Iran could become protracted and prolong what has been described as the largest disruption to oil supplies in history.

All three major indices declined for a fourth consecutive week, posting their steepest percentage losses since April’s tariff-driven volatility. The Dow Industrial Average ended Friday down -0.96%, or 443.93 points. The Nasdaq Composite fell -2.01% and is approaching correction territory, defined as a 10% decline from its recent peak. The S&P 500 declined -1.51% on Friday and is down nearly 7% from its all-time high.

In corporate news, Super Micro Computer placed two employees on leave and terminated a contractor after learning of their alleged involvement in a scheme to divert computer servers assembled in the US to China, in violation of export-control laws.

Nexstar Media said it has completed its $6.2 billion merger with rival Tegna after receiving federal clearance for the transaction.

Unilever is in discussions to separate its food business and combine it with spice maker McCormick, the Wall Street Journal reported.

Novartis reached a deal valued at up to $3 billion to acquire an experimental breast-cancer drug from Synnovation Therapeutics.

Scholastic said it will repurchase up to $200 million of its shares through a tender offer funded by the sale of its real-estate assets.

S&P 500 Best performing sector

Financials +0.19%, with Marsh & McLennan +3.26%, AON +2,73%, and Arthur Gallagher +2.45%

S&P 500 Worst performing sector

Utilities -4.11%, with Vistra -12.64%, Constellation Energy -10.90%, and NRG Energy -9.67%

Mega Caps

Alphabet -2.27%, Amazon -1.63%, Apple -0.39%, Meta Platforms -2.15%, Microsoft -1.85%, Nvidia -3.03%, and Tesla -3.24%

Information Technology

Best performer: Gen Digital +1.99%

Worst performer: Super Micro Computer -33.32%

Materials and Mining

Best performer: Vulcan Materials +0.54%

Worst performer: Mosaic -9.96%

European Stock Indices

CAC 40 -1.82%

DAX -2.01%

FTSE 100 -1.44%

Commodities

Gold spot -3.41% to $4,487.65 an ounce

Silver spot -6.68% to $67.76 an ounce

West Texas Intermediate +3.90% to $98.81 a barrel

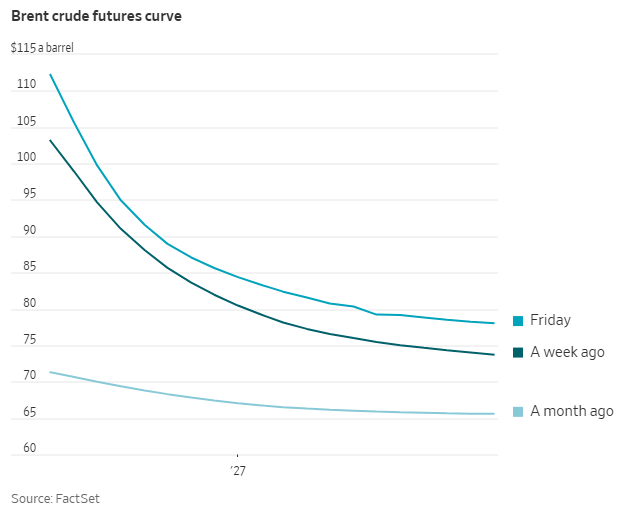

Brent crude +1.66% to $109.55 a barrel

Gold prices declined by more than three percent on Friday as the US dollar strengthened on expectations that inflation will keep interest rates higher and investors sought liquidity to cover margin calls. ETFs and futures have been selling off as these can be quickly liquidated, rather than physical gold, which is harder to move and sell.

Spot gold fell -3.41% to $4,487.64 per ounce, reversing an earlier gain of more than one percent. For the week, spot gold prices dropped -10.58%.

Spot silver also weakened, falling -6.68% to $67.76 per ounce, contributing to a -15.88% decline over the week.

Oil prices rose sharply on Friday, settling at their highest level in nearly four years after Iraq declared force majeure on all oilfields developed by foreign firms and the conflict involving Iran intensified, with the US preparing to deploy thousands of additional Marines and sailors to the Middle East.

Brent futures for May settled up $1.79, or +1.66%, at $109.55 a barrel, the highest since July 2022. US WTI crude futures for April, which expired on Friday, settled up $3.71, or +3.90%, at $98.81.

At the session high, Brent crude futures were up by more than $4.

The US-Israeli war on Iran showed no signs of easing, with attacks targeting key energy infrastructure in Iran and Iranian strikes against neighboring states, including Saudi Arabia, Qatar, and Kuwait.

Brent gained +5.45% for the week, while the front-month WTI contract settled down -0.50% versus last Friday’s close. WTI’s discount to Brent widened to its largest in 11 years on Wednesday.

Markets increasingly reflect expectations of more prolonged supply disruptions following recent attacks, as well as a delay of several weeks, at minimum, before the strategically important Strait of Hormuz is reopened.

Israel and Iran exchanged further attacks on Friday, following a strike on an oil refinery in Kuwait. On Thursday, President Trump said Israel would not carry out additional attacks on energy facilities.

On Friday, US Energy Secretary Chris Wright said that lifting oil sanctions on stranded, waterborne Iranian cargoes would allow supplies to reach Asia within three to four days. On Thursday, US Treasury Secretary Scott Bessent outlined those plans.

Bessent also said an additional release of crude from the US Strategic Petroleum Reserve was possible. Wright added that any reserve releases would occur over the coming months.

International Energy Agency Executive Director Fatih Birol warned in an interview with the Financial Times on Friday that restoring oil and gas flows from the Middle East Gulf could take up to six months.

The Trump administration is considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz, Axios reported on Friday, an outcome that could further tighten supply.

On Thursday, Brent surged above $119 a barrel, nearing a 9th March peak, after Iran responded to an Israeli attack on a major gas field by disabling 17% of Qatar’s LNG capacity. The damage is expected to take up to five years to repair.

Elsewhere, Ukraine’s state oil and gas company Naftogaz said on Friday that Russia attacked oil and gas facilities overnight in the Poltava and Sumy regions.

US energy companies increased the oil rig count by two to 414 this week, the highest level since mid-December, according to energy services firm Baker Hughes in its report on Friday.

Note: As of 4 pm EDT 20 March 2026

Currencies

EUR -0.38% to $1.1538

GBP -0.95% to $1.3300

Bitcoin +0.44% to $70,537.23

Ethereum -0.40% to $2,133.56

The dollar strengthened on Friday, though it posted a weekly decline against major currencies.

The euro, yen and sterling recorded weekly gains versus the dollar, as policymakers signalled a willingness to tolerate higher interest rates in response to the war in the Middle East, which has constrained oil and gas supplies.

The euro fell -0.38% to $1.1538, but gained +1.07% over the week.

The yen weakened -0.95% to ¥159.23 per dollar, while rising +0.30% on the week.

Sterling slipped -0.95% to $1.3300, yet advanced +0.59% against the dollar for the week.

The dollar index rose +0.29% to 99.50 on Friday, but ended the week down -0.99%, its largest weekly decline since late January.

As widely expected, the Fed held interest rates steady during its meeting last week, although Chair Jerome Powell said it was too soon to assess the scope and duration of the war’s economic impact.

The ECB also left rates unchanged last Thursday, while warning that energy prices could intensify inflationary pressures.

The BoE kept rates on hold as well, but triggered a sharp selloff in short-dated gilts after signalling it stood ready to act.

The BoJ left open the possibility of a rate increase as soon as April, catching off guard investors who had positioned themselves for a further weakening of the yen.

Fixed Income

US 10-year Bond +13.4 basis points to 4.387%

German 10-year +9.0 basis points to 3.053%

UK 10-year gilt +15.6 basis points to 4.940%

US Treasuries fell for a third consecutive session on Friday, mirroring the broader selloff in UK and European government bonds, as escalating Middle East tensions kept oil prices elevated and reinforced inflation concerns.

The 2-year yield, the most sensitive to shifts in interest-rate expectations, rose +10.6 bps to 3.913% on the day and increased +17.9 bps last week, extending a three-week run of gains.

The 10-year yield also moved higher, rising +13.4 bps to 4.387%, its largest one-day increase since early June 2025. The 10-year yield ended last week +10.5 bps above the prior Friday’s close. At the long end of the curve, the selloff was less pronounced: the 30-year yield rose +2.8 bps on Friday and finished last week +4.1 bps higher.

That shift in policy expectations flowed through to the curve, which flattened last week as the spread between 2- and 10-year yields narrowed to 47.4 bps from 54.8 bps the previous week.

The curve displayed a classic bear-flattening pattern, with short-dated yields rising faster than longer-term rates as investors priced in a greater risk of reaccelerating inflation.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in just 6.1 bps of rate hikes in 2026, in contrast with the 21.5 bps of rate cuts priced in the previous week. Fed funds futures traders are now pricing in a 12.4% probability of a 25 bps rate hike at the 29th April FOMC meeting, up from 0.0% a week ago.

The selloff in global bonds intensified on Friday after central bankers worldwide, including officials at the ECB, warned about rising inflation risks, prompting investors to rapidly price in interest-rate increases this year. Eurozone government bond yields climbed to their highest level in 15 years on Friday.

The 10-year German Bund yield rose +9.0 bps to 3.053%, its highest level since 2011, while the two-year Schatz, more sensitive to shifting expectations for rates and inflation, gained +9.8 bps to 2.679%. Over the week, the 10-year yield increased +10.5 bps and the two-year yield rose +17.9 bps. At the long end of the curve, the 30-year Bund yield added +7.4 bps on Friday but finished the week -0.4 bps lower at 3.531%.

The UK 10-year gilt yield rose +16.9 bps on Friday and has increased +58.4 bps since the start of the war, compared with a +39.7 bps rise in their German counterparts.

Money markets indicated that traders were assigning close to a 70% probability of a rate hike by both the ECB and the BoE as early as next month. Markets also expected the ECB to deliver at least one additional increase thereafter and the BoE to raise rates twice.

Within the eurozone, Italian yields have risen significantly faster than those in other markets, reflecting Italy’s greater reliance on imported oil and gas.

Italy’s 10-year BTP yield rose +18.5 bps to 3.961% on Friday, marking its largest one-day increase in a year. The 10-year BTP yield ended the week +17.5 bps higher.

The spread between Italian BTPs and German Bunds widened to 90.8 bps, its broadest level since last September and 10.8 bps wider than the prior week.

Note: As of 4 pm EDT 20 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

هذه المقالة متاحة لأغراض ملعوماتية فقط، ولا ينبغي اعتبارها عرضًا أو التماسًا لعرض شراء أو بيع أي استثمارات أو خدمات ذات صلة يمكن الإشارة إليها هنا. ينطوي التداول في الأدوات المالية على مخاطر كبيرة من الخسارة وقد لا يكون مناسبًا لجميع المستثمرين. الأداء السابق ليس مؤشرًا موثوقًا به للأداء المستقبلي.

أنشأ ذلك المتخصصون. للمحترفون.