Will Europe and Asia struggle for LNG?

Corporate Earnings News

Companies reporting on Tuesday, 3rd March: AutoZone, Best Buy, CrowdStrike Holdings, Target

Posted on Monday, 2nd March

Norwegian Cruise Line Holdings quarterly revenue +6.4% to $2.244 bn vs $2.343 bn estimate

EPS at $0.28 vs $0.26 estimate

John W. Chidsey, President and CEO, said, “The team delivered solid fourth quarter and full year 2025 results reflecting the strength of our award-winning brands, loyal guests and dedication of our team and crew members. As I step into this new role my initial assessment is that our strategy is sound, but execution and cross-functional alignment have fallen short. Our priority is to act urgently to address these gaps by improving coordination, reinforcing accountability, and strengthening financial discipline across the organization. The good news is that we have strong assets and have recently enhanced our leadership team with the right combination of new and tenured talent. Now, with a clear focus and necessary rigor, I am confident in our ability to create sustainable long-term value.” — see report.

Key data to move markets today

EU: Eurozone Harmonised Index of Consumer Prices, and Core Harmonized Index of Consumer Prices, Italian CPI, and speeches by French Central Bank Governor François de Villeroy de Galhau, Dutch Central Bank Governor Olaf Sleijpen, and Austrian Central Bank Governor Martin Kocher

US: Speeches by New York Fed President John Williams, Kansas City Fed President Jeff Schmid, and Minneapolis Fed President Neel Kashkari

JAPAN: A speech by BoJ Governor Kazuo Ueda

CHINA: NBS Manufacturing and Non-Manufacturing PMIs, RatingDog Manufacturing and Services PMIs

Global Macro Updates

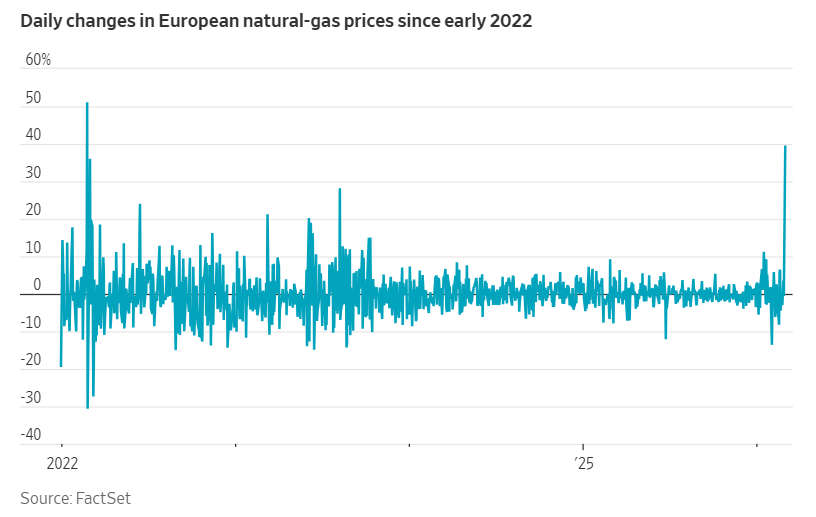

LNG market cut off by threats to the Strait of Hormuz. The global oil market has been disrupted by the US-Israel led war with Iran but liquefied natural gas (LNG) consumers are facing even greater threats. According to the Financial Times, 81mn tonnes (110bn cubic metres) of LNG, about a fifth of global supply, a greater share than that for oil exported through the same sea lane, was shipped through the Strait of Hormuz last year. In light of attacks on energy facilities by Iran, QatarEnergy, the state-owned petroleum company, announced the temporary closure of its LNG facilities.

The interruption in LNG flows has raised the alarm across both Europe and Asia given their dependency on these flows. The closure has tightened the global market and prompted renewed competition between these two major regional LNG markets for available cargoes. Although the majority of LNG cargoes passing through the Strait are destined for Asian markets such as Japan, China, South Korea, India and Taiwan, the consequences are being felt in Europe as well with European natural gas prices already surging. European storage levels are below seasonal average and roughly 10 percent lower than last year at the same time, with low January temperatures having driven the decline.

European gas buyers entered the year with cautious optimism, expecting additional LNG supply to exceed 35mn tonnes in 2026 and subdued Asian demand given the slowdown in China. Market conditions appeared balanced, with prices just under $11 per one million British thermal units (€31/MWh).

The closure of the Strait is expected to result in the loss of about 1.5mn tonnes (2.2 bcm) a week of LNG exports, forcing Asian and European markets to draw more heavily on existing storage and increasing the urgency of replenishing stocks over the summer. Even if the conflict is resolved swiftly, the market is likely to remain tight for some time after trade resumes. In response to the closure, as noted by the Financial Times, today foreign ministry spokesperson Mao Ning told reporters in Beijing that, “China urges all parties to immediately cease military operations, avoid escalating tensions and safeguard the safety of the Strait of Hormuz.” She added: “China will take necessary measures to safeguard its own energy security.”

Compounding demand pressures on an already tight market were the precautionary shutdowns of Israel’s Leviathan and Karish gasfields, which are crucial suppliers to Egypt. Egypt, which imported close to 10 bcm from Israel last year, will almost certainly need to increase LNG imports to compensate for lost volumes. Gas exports from Iran to Turkey could also be reduced, potentially prompting Turkish buyers to seek further LNG cargoes if the Iranian pipeline supply, more than 7 bcm in 2025, is restricted.

The duration of the conflict and the closure of the Strait of Hormuz will determine the immediate outcome for gas prices. Following QatarEnergy’s announcement, benchmark European TTF gas prices spiked over 20 per cent compared to the previous trading week, rising above $15 per one million British thermal units (€45/MWh).

While weak Chinese LNG demand may be restraining prices for now, a prolonged closure will intensify market pressures. The curtailment of Russian gas supplies to Europe four years ago offers a relevant “ceiling case" vs " base case” comparison, when prices surged to nearly $100/mmbtu in August 2022 and averaged $40/mmbtu that year. This time, the reaction is expected to be less extreme, provided the Strait’s closure is temporary.

On Monday, natural gas prices in Europe closed +39% higher, reaching €44.51 per megawatt-hour, the highest level observed in approximately a year. In the UK, natural gas prices were up by +45%, settling at 113.79 pence per therm.

By comparison, natural gas prices in the US recorded a far more modest increase, ending the day up just +3.5% per cent at $2.96 per million British thermal units.

US Stock Indices

Dow Jones Industrial Average -0.15%

Nasdaq 100 +0.13%

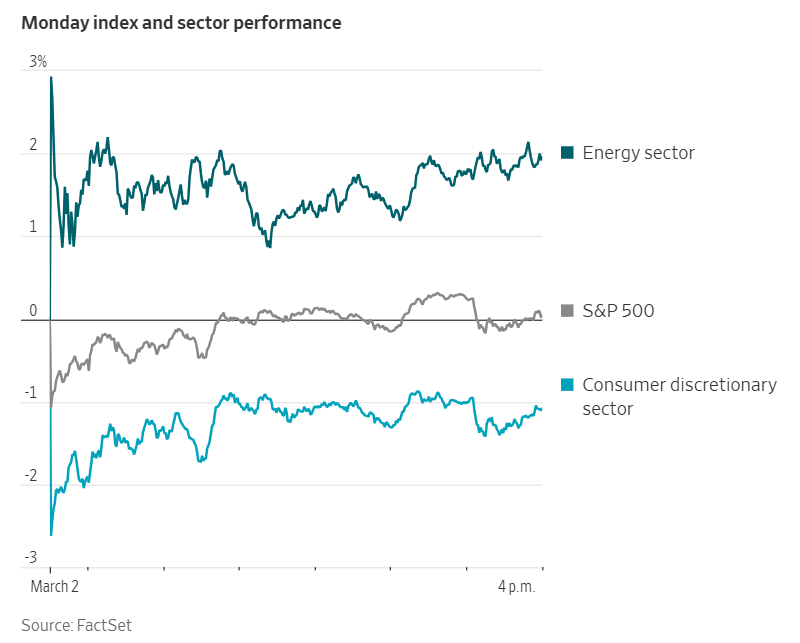

S&P 500 +0.04%, with 4 of the 11 sectors of the S&P 500 up

The ongoing conflict in the Middle East reverberated through global markets on Monday.

On the first trading day following the US-led strikes in the region, equity markets initially declined. Airline shares dropped as Defence stocks advanced. Nevertheless, a subsequent rally in the Energy and Technology sectors, perhaps driven by expectations that the conflict will be relatively short, enabled the S&P 500 to stage its biggest intraday recovery since November, rebounding from an early decline of -1.20% to close the day marginally higher, up +0.04%.

The Dow Jones Industrial Average ended the day down -0.15%, a decrease of 73.14 points, while the Nasdaq Composite advanced +0.36%.

In corporate news, Anthropic reported outages affecting its AI chatbot Claude and associated consumer applications on Monday. The company attributed the disruptions to unprecedented demand for its services.

Nvidia announced plans to invest $4 billion in two firms specialising in data centre optics, a technology integral to AI infrastructure.

BlackRock’s Global Infrastructure Partners and EQT reached an agreement to acquire AES for approximately $10.7 billion in cash, reflecting increasing interest in power plant developers capable of supporting electricity demands for AI data centres.

S&P 500 Best performing sector

Energy +1.95%, with Marathon Petroleum +5.86%, Valero Energy +5.02%, and APA +4.35%

S&P 500 Worst performing sector

Consumer Staples -1.35%, with Estee Lauder -8.48%, Dollar Tree -5.22%, and Monster Beverage -4.97%

Mega Caps

Alphabet -1.63%, Amazon -0.77%, Apple +0.20%, Meta Platforms +0.83%, Microsoft +1.48%, Nvidia +2.99%, and Tesla +0.20%

Information Technology

Best performer: Palantir Technologies +5.82%

Worst performer: TE Connectivity -7.89%

Materials and Mining

Best performer: CF Industries +4.78%

Worst performer: PPG Industries -3.30%

European Stock Indices

CAC 40 -2.17%

DAX -2.56%

FTSE 100 -1.20%

Commodities

Gold spot +0.47% to $5,321.60 an ounce

Silver spot -5.41% to $89.28 an ounce

West Texas Intermediate +5.54% to $71.02 a barrel

Brent crude +6.17% to $77.73 a barrel

Gold prices advanced for the fourth consecutive session on Monday, as heightened geopolitical tensions stemming from the intensifying US and Israeli air campaign against Iran and the widening of the conflict across GCC states prompted investors to seek refuge in safe-haven assets. The escalating conflict has fuelled concerns that it may develop into a prolonged regional war, thereby exacerbating uncertainty in global markets.

Spot gold gained +0.47% to reach $5,321.60 per ounce. In the previous session, the precious metal surged by +2.17%, marking its highest level in over four weeks.

In contrast, spot silver retreated-5.41% to $89.28 per ounce, following a rise to its highest point in more than four weeks during the previous session.

Oil prices advanced for a second consecutive session on Monday, driven by the escalating conflict and mounting threats to shipping routes through the Strait of Hormuz.

Brent crude futures ended the session up $4.52, or +6.17% to $77.73 per barrel. Earlier in the day, it had surged to $82.37, its highest level since January 2025.

US WTI crude also advanced, gaining $3.73, or +5.54%, to settle at $71.02 per barrel.

The US and Israeli air campaign against Iran intensified on Monday, with Israel extending its operations to Lebanon and Iran retaliating by striking energy infrastructure across Gulf nations and targeting tankers navigating the Strait of Hormuz.

On any given day, vessels transporting crude oil equivalent to approximately one-fifth of global demand traverse the Strait of Hormuz, alongside tankers carrying diesel, petrol, and other fuels to major Asian markets such as China and India.

Concerns over the security of passage through the Strait of Hormuz have intensified, with Iranian media reporting on Monday that a senior official of the Iranian Revolutionary Guards declared the strait closed and warned that Iran would fire upon any vessel attempting to transit.

Shipping data from Sunday indicated that at least 150 tankers, including both crude oil and liquefied natural gas vessels, were anchored in open Gulf waters beyond the Strait of Hormuz. In addition, a further 100 or more tankers, as well as dozens of cargo ships, were reported to be anchored outside the strait along the coasts of the United Arab Emirates and Oman and at designated anchorage points.

The Port of Kuwait has been closed as a direct consequence of these developments.

According to Rystad Energy, the effective closure of the Strait of Hormuz would result in a net loss of between 8 and 10 million bpd of crude oil supply, even after accounting for the redirection of some flows via Saudi Arabia’s East-West pipeline and Abu Dhabi’s pipeline infrastructure.

This crisis has also prompted Asian governments and refiners to review their strategic oil reserves and to explore alternative shipping routes and supply sources. During a webinar on Sunday, analysts at Kpler suggested that India may seek to increase imports of Russian oil to compensate for any potential shortfall in Middle Eastern supply.

In response to the heightened risks, Platts has initiated a review of the deliverability of crude oil from ports within the Persian Gulf as part of its Market on Close assessment process for Middle Eastern crude.

As reported by Bloomberg, there are limited alternatives to the Strait of Hormuz. Saudi Arabia is able to divert some shipments through a 746-mile pipeline with a capacity of 5 million barrels per day, which traverses the kingdom to a Red Sea terminal for onward export. The United Arab Emirates can also bypass the strait to a lesser extent, utilising the 1.5 million barrels per day Habshan-Fujairah pipeline, which connects inland oil fields to a terminal on the Gulf of Oman.

Note: As of 4 pm EST 2 March 2026

Currencies

EUR -1.08% to $1.1688

GBP -0.60% to $1.3404

Bitcoin +6.05% to $69,430.93

Ethereum +6.36% to $2,043.37

On Monday, both the euro and the yen declined, as the escalating conflict in the Middle East shifted focus toward the growth prospects of countries reliant on energy imports and how central banks may respond to inflation pressures.

The US dollar rose, primarily driven by increased safe-haven demand resulting from US and Israeli air strikes on Iran that have now extended into neighbouring regions. Suggestions that the Fed may now postpone rate cuts on concerns around elevated inflation resulting from higher oil prices also contributed to the dollar’s strength. Although the US is a net energy exporter, it does import some crude oil.

The dollar index was +0.92% to 98.55. The euro fell -1.08% to $1.1688 and sterling declined -0.60% to $1.3404, its lowest level since 17th December. The yen was -0.82% to ¥157.34 per dollar.

In addition, the Swiss National Bank signalled an increased willingness to intervene in foreign exchange markets, following the surge of the Swiss franc to its strongest position against the euro in over a decade as a result of the Middle East conflict.

Fixed Income

US 10-year Bond +8.8 basis points to 4.040%

German 10-year +5.5 basis points to 2.711%

UK 10-year gilt +7.7 basis points to 4.311%

US Treasury yields increased sharply on Monday on heightened concerns over escalating inflationary pressures resulting from the war against Iran.

The two-year US Treasury yield, which typically reflects market expectations for Fed fund rates, surged +9.4 bps to reach 3.481%, marking its largest daily increase since 6th June.

Yields continued to rise after the Institute for Supply Management (ISM) reported that its manufacturing PMI registered at 52.4 for the previous month, little changed from 52.6 in January. This marks the second consecutive month above the 50 threshold indicative of expansion, and surpasses economists’ forecast of 51.8.

Additionally, the ISM survey indicated that the measure of prices paid by manufacturers for inputs rose to its highest level in nearly three and a half years, intensifying market apprehension regarding inflation.

The yield on the US 10-year Treasury note advanced +8.8 bps to 4.040%, also representing its largest daily rise since 6th June. The 30-year bond yield climbed +5.9 bps to 4.677%.

The US Treasury yield curve, as measured by the spread between the two- and ten-year Treasury yields, stood at a positive 55.9 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 50.4 bps of cuts in 2026, lower than the 59.0 bps priced in the previous week. Fed funds futures traders are now pricing in a 2.5% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 5.5% a week ago.

Eurozone bonds experienced their most pronounced selloff in almost three months on Monday, as intensifying tensions in the Middle East reignited concerns regarding inflation given that Europe is an importer of crude oil as well as middle distillates, including diesel and jet fuel.

The yield on Germany's 10-year government bond climbed +5.5 bps to 2.711%, marking its largest single-day increase since December. The two-year bond yield, which is particularly responsive to shifts in interest rate expectations, rose +7.9 bps to 2.095%, its highest level since July. On the long-end of the curve, the 30-year yield advanced +4.0 bps to 3.359%.

Despite the prevailing risk-off sentiment, markets have not yet triggered the typical flight to the safety of Bunds, particularly following their robust performance earlier in the year. Bund yields recorded their largest monthly decline in February since April.

An uptick in inflation has the potential to prompt the ECB to reconsider its interest rate strategy. Money markets were most recently pricing in approximately an 8% likelihood of a rate cut by year-end, markedly lower than the 40% probability observed last Friday.

The yield curve between Germany's two- and ten-year bonds exhibited a bear flattening pattern, with short-term yields advancing more than long-term ones. The spread between these maturities narrowed by 2.4 bps to stand at roughly 61.6 bps, its lowest point since November.

Note: As of 5 pm EST 2 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.