Can headline fatigue become a risk premium?

What to look out for today

Companies reporting on Friday, 8 May: Enbridge, Sony

Key data to move markets today

JAPAN: Labour Cash Earnings

EU: German Industrial Production, German Trade Balance and speeches by ECB President Christine Lagarde, ECB Vice President Luis de Guindos, ECB Executive Board members Piero Cipollone and Isabel Schnabel and German Bundesbank President Joachim Nagel.

USA: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, Unemployment Rate, U6 Underemployment Rate, Michigan Consumer Sentiment index and Consumer Expectations Index, UoM 1 and 5-year Inflation Expectations and a speech by Fed Governor Lisa Cook

Global Macro Updates

Markets look past the strait, but the risk lies in what they choose not to see. Equity markets are entering a peculiar phase of cognitive dissonance. With corporate earnings delivering one of the strongest seasonal performances in recent memory, investor attention has pivoted decisively toward balance sheets and forward guidance, effectively tuning out the escalating exchange of fire between US and Iranian forces in the Strait of Hormuz. This is not complacency in the traditional sense, it can be perilous: headline fatigue that mistakes tactical de-escalation for strategic resolution.

The facts on the ground tell a more complicated story. US Central Command confirmed strikes against Iranian missile and drone sites, as well as command and control positions, after Navy guided-missile destroyers came under attack while transiting the Strait. The US President characterised the engagement as a ‘love tap’ and no US vessels were damaged. This was language clearly calibrated to contain market volatility. Yet, the underlying architecture of the conflict remains unresolved. Iran has yet to respond formally to the US’ 14-point framework and Iranian officials have signalled that nuclear issues will be excluded from any near-term negotiations: a red line that directly contradicts core US demands. Markets appear to be pricing in an agreement that does not yet exist.

The macroeconomic transmission mechanism may already be operating beneath the surface. The New York Fed's April Survey of Consumer Expectations showed year-ahead inflation expectations edging up to 3.6% from 3.4% in March. Median year-ahead gas price growth expectations, while declining sharply m/o/m, remain elevated at 5.1%, still carrying the residual imprint of energy disruptions tied to earlier phases of the Iran conflict. Labour market perceptions, while broadly stable, showed a slight deterioration in unemployment expectations, now at their highest level since April 2025.

The risk is not an immediate shock. It is the slow erosion of confidence through protracted uncertainty. A prolonged impasse over the Strait of Hormuz, even without outright closure, is sufficient to sustain insurance premium pressures on shipping, keep energy volatility elevated and gradually tighten financial conditions at the margin. Markets focussed on earnings beats today may find themselves repricing geopolitical risk premiums tomorrow, not because the conflict escalated, but because it never ended.

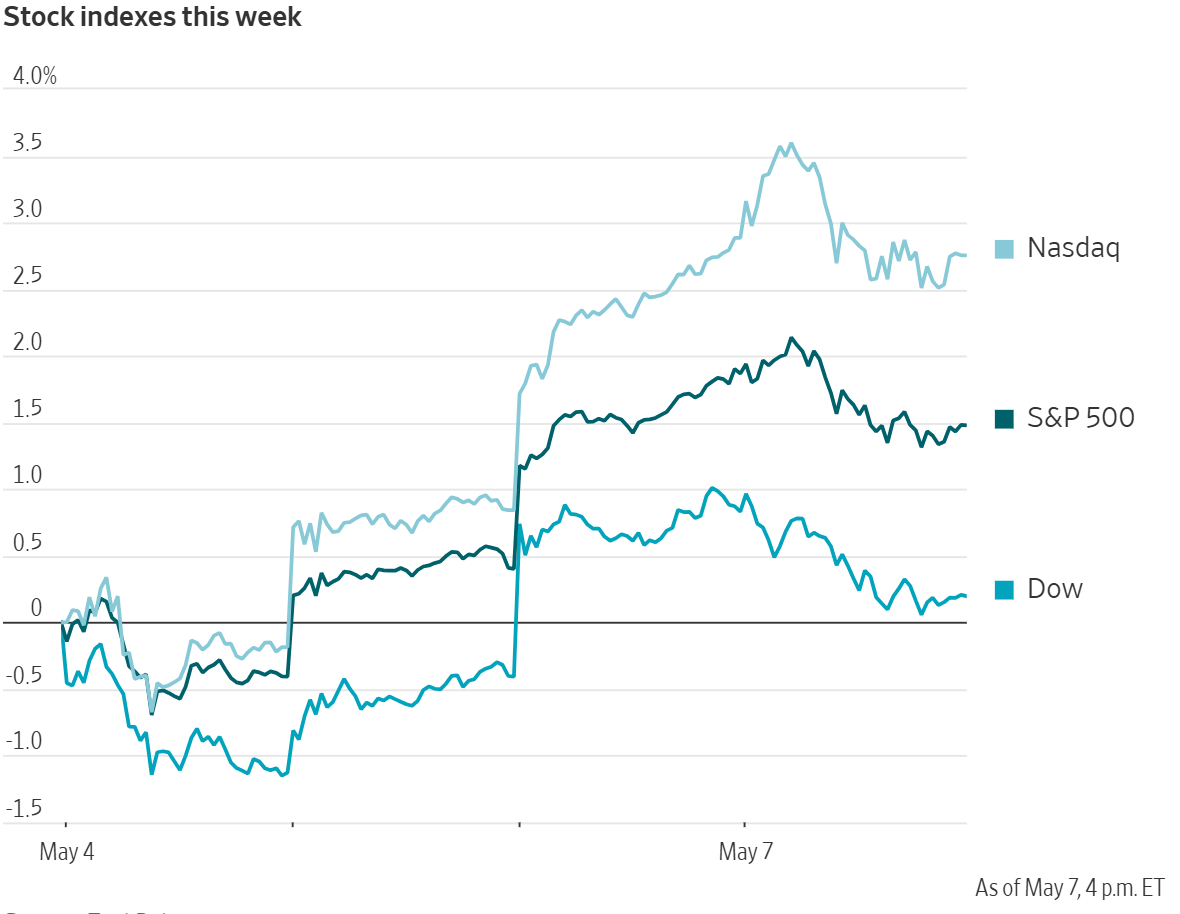

US Stock Indices

Dow Jones Industrial Average -0.63%

Nasdaq 100 -0.12%

S&P 500 -0.38%, with 9 sectors of 11 the S&P 500 down

After the S&P 500 and Nasdaq Composite eased slightly from the record highs reached on Wednesday, earnings-related headlines drove several outsized moves.

Despite strong results from software and cybersecurity companies, the Nasdaq Composite closed -0.13% lower. The S&P 500 fell -0.38%, while the Dow Jones Industrial Average declined -0.63%, or 313.62 points.

In corporate news, Arm Holdings fell after weakness in the smartphone market weighed on royalty revenue, offsetting growth tied to AI data-centre demand.

Datadog advanced after the software company raised its full-year outlook for revenue and earnings, well above Wall Street expectations.

Peloton Interactive increased its full-year guidance, signalling that its turnaround, supported by new commercial offerings and upgraded equipment, remains on track.

At its investor day, Citigroup said it is targeting a medium-term return on tangible equity (RoTE) of 14% to 15%, in line with expectations.

Shares of national-security satellite company HawkEye 360 rose in their public-market debut on Thursday, underscoring investor demand for defence-related companies.

S&P 500 Best performing sector

Information Technology +0.08%, with Fortinet +20.03%, CrowdStrike Holdings +8.04% and PTC +7.96%

S&P 500 Worst performing sector

Materials -1.83%, with FMC -7.51%, Celanese -5.99% and International Flavors & Fragrances -5.63%

Mega Caps

Alphabet +0.06%, Amazon -1.38%, Apple -0.01%, Meta Platforms +0.64%, Microsoft +1.67%, Nvidia +1.85% and Tesla +3.33%

Information Technology

Best performer: Fortinet +20.03%

Worst performer: Teradyne -7.42%

Materials and Mining

Best performer: Albemarle +2.98%

Worst performer: FMC -7.51%

Corporate Earnings Reports

Posted on Thursday, 7 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Datadog reported Q1 revenue of $1.01 vs $958 mn estimate with 32% y/o/y growth and EPS of $0.60 vs $0.52 expected. FCF reached $289 mn vs $153 mn estimate and operating cash flow $335 mn. $100K+ ARR customers hit 5K, up 21% y/o/y, with NRR at 121%. Q2 guidance: revenue $1.1 bn vs $995 mn estimated, EPS $0.58 vs $0.52 estimated. FY26 guidance raised to revenue $4.3 bn vs $4.1 bn estimated, EPS $2.40 vs $2.23 estimated. Datadog CEO stated "Datadog executed to a strong quarter, with 32% year-over-year revenue growth, $335 million in operating cash flow, and $289 million in FCF."

McDonald's reported Q1 earnings with adjusted EPS of $2.83 beating estimates of $2.75 and revenue of $6.52 bn topping consensus of $6.48 bn. Global comparable sales rose 3.8% missing expectations of 3.92%, US comp sales increased 3.9% below 4.11% estimate, international developmental 3.4% versus 3.71%, and international operated markets 3.9% above 3.89%. Systemwide sales grew over 6%. The company expects 2026 capital expenditures between $3.7 bn and $3.9 bn and operating margin in the mid-to-high 40% range. McDonald's is on pace for approximately 50,000 global restaurants by end 2027 and plans to expand in China. It will remove self-serve soda fountains nationwide by 2032. CEO Chris Kempczinski noted a challenging environment that may be worsening but expressed confidence in the balance of the year.

CoreWeave reported Q1 earnings with revenue of $2.08 bn, beating estimates of $1.97 bn, adjusted EBITDA of $1.16 bn, beating estimates of $1.14 bn at a 56% margin vs 57.4% expected, but net loss of $740 mn, missing estimates of $628.2 mn and EPS loss of $1.40, missing estimates of $0.92 to $1.20. Backlog stands at $99.4 bn, total contracted power at ~3.5 GW, and active power surpassed 1 GW.

Applied Optoelectronics reported Q1 revenue of $151 mn vs $155 mn estimated and EPS of ($0.07) vs estimates of ($0.05). The company completed its first shipment of 800G products. Q2 guidance calls for revenue of $189 mn vs $193 mn estimated and EPS of $0.01 vs $0.07 estimated.

Coinbase reported Q1 total revenue of $1.40 bn, missing Wall Street consensus of $1.49 bn, transaction revenue $756 mn vs $785.9 mn expected, subscription & services revenue $584 mn vs $625.3 mn, and EPS -$1.49 vs. $0.04. It guided Q2 subscription & services revenue to $565 mn -$645 mn, Q2 restructuring expenses ~$50 mn - $60 mn, and FY adjusted expenses flat year-over-year.

Affirm reported quarterly EPS of $0.3, beating Wall Street consensus of $0.17, and revenue of $1.03 bn, surpassing estimates of $995 mn.

Mercado Libre reported Q1 FY26 earnings with revenue of $8.85 bn vs $8.37 bn consensus estimate, a $0.48 bn beat and 49% y/o/y growth. EPS was $8.23, beating estimates by $0.03. Net income was $417 mn, missing $426 mn estimate. GMV rose 42% y/o/y to $19 bn, beating $18 bn estimate, TPV increased 50% y/o/y to $87 bn, beating $80 bn estimate. Commerce revenue grew 47% y/o/y to $4.9 bn, fintech 51% y/o/y to $4.0 bn. Free shipping and credit expansion boosted revenue but squeezed margins. CEO highlighted another exceptional quarter with net revenue and financial income up 49% y/o/y, the fastest pace in almost four years.

Rocket Lab reported Q1 revenue of $200 mn, beating $189 mn estimate and EPS ($0.07) vs est. ($0.08). Backlog grew to $2.2 bn, up 20% q/o/q, with 31 new Electron and HASTE contracts signed plus 5 Neutron launches. Q2 guidance includes revenue $235 mn vs $205 mn estimated and gross margins 39% vs 41% estimated. Rocket Lab won a $30 mn HASTE contract from Anduril for 3 hypersonic test launches out of Virginia, supporting Mach 5+ defence tech, with HASTE now nearly 1/3 of backlog. Company stated it surpassed all guidance metrics for the quarter.

European Stock Indices

CAC 40 -1.17%

DAX -1.02%

FTSE 100 -1.55%

Commodities

Gold spot -0.08% to $4,685.09 an ounce

Silver spot +1.48% to $78.48 an ounce

West Texas Intermediate +1.51% to $97.66 a barrel

Brent crude +1.04% to $103.07 a barrel

Gold prices eased modestly on Thursday.

Spot gold was -0.08% lower at $4,685.09 per ounce, after touching a two-week high earlier in the session.

Data showed that China’s central bank added to its gold reserves for an 18th consecutive month in April.

Spot silver gained +1.48% to $78.48 per ounce, after reaching its highest level since 17 April.

US crude futures advanced on Thursday in volatile trading. WTI rose $1.45, or +1.51%, to $97.66 a barrel, while Brent added $1.06, or +1.04%, to $103.07.

WTI and Brent fell to session lows of $89.80 and $96.05, respectively, following additional reports that the United States and Iran were nearing a limited, temporary agreement to halt the war, reopen the Strait and pursue a nuclear framework. Prices rebounded after reports that Iran had established a new agency to screen and tax vessels seeking to transit the Strait, an approach the US has repeatedly said is unacceptable. Iranian state television also reported that Iran would seek reparations for war-related damage before reopening the Strait, a demand the US has said it would not accept.

Additionally, Caixin reported that a Chinese-owned product tanker was attacked off the coast of the UAE on 4 May, triggering a fire on deck. Estimates suggest roughly 1,600 ships are backed up just outside the Strait. Reports also indicated an oil slick in and around the area of Kharg Island. Iran’s state broadcaster, citing an unnamed military official, said Iranian missile fire forced ‘enemy units’ in the Strait of Hormuz to retreat following a US military attack on an Iranian oil tanker.

IEA Executive Director Fatih Birol warned at a Toronto conference that energy markets are entering ‘troubled waters,’ as the Iran war continues to take millions of barrels offline. He noted Brent’s recent $96 – $102 range on mixed reports of a short-term deal to reopen the Strait of Hormuz, described volatility as the dominant theme, urged Canada to pursue new export destinations and said the IEA stands ready to release additional SPR barrels.

Reuters cited Kpler data showing Asian product exports last month were down nearly 3.0 million bpd versus the average of the three months prior to the war. Jet fuel exports averaged 596,000 bpd last month, compared with 1.54 million bpd before the war.

Oil product stockpiles at the port of Singapore fell 1.071 million barrels last week to 44.828 million barrels.

In addition, Ukraine continued to target Russian energy infrastructure, with two drone strikes reported on Thursday, one on the Perm oil pumping station and another on the Perm refinery. The pumping station has been targeted multiple times in the last two weeks.

Note: As of 4 pm EDT 7 May 2026

Currencies

EUR -0.19% to $1.1724

GBP -0.31% to $1.3545

Bitcoin -2.20% to $79,733.02

Ethereum -2.74% to $2,288.87

The dollar pared early losses to trade with a firmer tone against most major currencies on Thursday, as investors weighed prospects for a de-escalation in the Iran war.

The euro was down -0.19% on the day at $1.1724, after rising +0.48% on Wednesday, while sterling slipped -0.31% to $1.3545 after rallying +0.39% the previous session.

The Japanese yen weakened -0.36% versus the dollar to ¥156.82, a day after strengthening sharply amid speculation that Japanese authorities had again intervened to support the currency.

BoJ data released on Thursday suggested Japan may have spent as much as ¥5.01 trillion, or approximately $32.06 billion, in its latest effort to shore up the currency, pointing to repeated bouts of market intervention.

Japan’s top currency diplomat, Atsushi Mimura, said separately on Thursday that the country faced no constraints on intervening in currency markets.

US Treasury Secretary Scott Bessent is scheduled to meet Japanese Prime Minister Sanae Takaichi next week, and Nikkei reported that discussions will include measures to curb speculative yen selling.

Fixed Income

US 10-year Bond +4.4 basis points to 4.395%

German 10-year Bund +0.4 basis points to 3.009%

UK 10-year Gilt +1.1 basis points to 4.959%

US Treasury yields rose across the curve in volatile trading on Thursday, reversing earlier declines.

The yield on the US 10-year Treasury note rose +4.4 bps to 4.395%, after falling to 4.314% earlier in the day, its lowest level since 27 April.

The 30-year yield added +3.3 bps to 4.971%, after dipping to 4.911% earlier in the session, its lowest since 24 April. At the front end, the 2-year yield increased +4.3 bps to 3.913%, after sliding to 3.824% earlier, its lowest since 28 April.

The US Treasury yield curve, measured as the spread between 2-year and 10-year notes, was at 48.2 bps, from 48.1 bps on Wednesday.

On Fedspeak, Cleveland Fed President Beth Hammack said it would be wrong to assume the Fed’s next move will be a cut, and noted that elevated prices are weighing on consumer spending. San Francisco Fed President Mary Daly said she sees no signs of rising long-term inflation expectations. New York Fed President John Williams said the economy has remained resilient and has performed better than many expected, though uncertainty persists.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 3.2 bps of rate hikes in 2026, compared to 2.4 bps of rate cuts priced in a week ago. Fed funds futures traders are now pricing in a 3.7% probability of a 25 bps rate cut at the June FOMC meeting, from 5.6% a week ago.

Eurozone government bonds were mixed in a narrow trading range on Thursday, after posting their largest rally in a month the previous day.

The two-year Schatz yield fell -11.2 bps on Wednesday, the biggest decline since 8 April, and was +0.4 bps higher on Thursday at 2.583%. The 10-year Bund yield edged up +0.4 bps to 3.009%. At the long end, the 30-year yield rose +0.2 bps to 3.545%.

Money markets indicate traders are pricing in roughly a 75% probability of a June hike by the ECB, down from about 88% at the end of last week.

Market participants are awaiting the outcome of the UK local elections, which could raise questions over Prime Minister Keir Starmer’s position and potentially revive concerns about fiscal slippage.

UK 10-year yields rose +1.1 bps to 4.959% on Thursday, after reaching 5.107% on Monday, their highest level in 18 years.

Italian 10-year yields eased -0.7 bps to 3.732%, leaving the spread over Bunds at 72.3 bps.

Note: As of 4 pm EDT 7 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

هذه المقالة متاحة لأغراض معلوماتية فقط، ولا ينبغي اعتبارها عرضًا أو التماسًا لعرض شراء أو بيع أي استثمارات أو خدمات ذات صلة يمكن الإشارة إليها هنا. ينطوي التداول في الأدوات المالية على مخاطر كبيرة من الخسارة وقد لا يكون مناسبًا لجميع المستثمرين. الأداء السابق ليس مؤشرًا موثوقًا به للأداء المستقبلي.

مقالات ذات صلة

Fixed Income Briefing April 2026نشرة الدخل الثابت8 مايو 2026

Fixed Income Briefing April 2026نشرة الدخل الثابت8 مايو 2026 April Review - Forged under pressure: AI and structural tailwindsمراجعة الأسهم الشهرية7 مايو 2026

April Review - Forged under pressure: AI and structural tailwindsمراجعة الأسهم الشهرية7 مايو 2026 Will Trump be the winning dealmaker?أسبوعياً7 مايو 2026

Will Trump be the winning dealmaker?أسبوعياً7 مايو 2026 Earnings Scoreboard - Is the Iran premium priced into US refining?لوحة نتائج الأرباح6 مايو 2026

Earnings Scoreboard - Is the Iran premium priced into US refining?لوحة نتائج الأرباح6 مايو 2026

أنشأها المتخصصون. للمحترفين.