A real rebound or a cost-driven illusion?

What to look out for today

Companies reporting on Friday, 24 April: Procter & Gamble, SLB

Key data to move markets today

EU: German IFO Business Climate, Current Assessment and Expectations Surveys

UK: GfK Consumer Confidence and Retail Sales

US: Michigan Consumer Expectations Index, Michigan Consumer Sentiment Index and UoM 1 and 5-year Consumer Inflation Expectations

JAPAN: National CPI

Global Macro Updates

April US S&P Global PMIs. The S&P Global Flash Composite PMI for April registered at 52.0, marking a three-month high and exceeding the consensus estimate of 50.6. The Manufacturing PMI advanced to 54.0, its highest level in 47 months and well above the consensus forecast of 52.9. The Services PMI also improved, reaching a two-month high of 51.3, slightly ahead of the expected 51.0.

The report highlighted a modest uptick in US business activity in April following near-stagnation in March, which was attributed to the conflict in the Middle East. Nevertheless, overall growth remained subdued, particularly in the services sector, where demand continued to weaken.

In contrast, manufacturing output surged to a four-year high, propelled by the strongest increase in new orders since May 2022. Employment remained flat overall, representing the weakest two-month period since late 2024. Manufacturing jobs declined, while hiring in services was only modest, reflecting cost pressures and tepid demand.

On the pricing front, the effects of conflict and tariffs caused supply chain delays to reach their longest duration since August 2022. This led to a spike in purchasing activity to near four-year highs and drove price increases at the fastest pace since July 2022, with input costs reaching an eleven-month peak.

These developments follow March’s flash PMIs, which indicated stagflationary pressures, as US business activity growth slowed to an eleven-month low and input costs surged to a ten-month high, resulting in the largest increase in selling prices in over three and a half years.

Eurozone Flash PMI. In April 2026, the Flash Eurozone Composite Output Index decreased to 48.6, underperforming consensus expectations of 50.1 and falling from March’s final reading of 50.7. This marks the first contraction in the region’s economic activity in 16 months.

The services sector experienced a pronounced decline, with activity slipping to a 62-month low of 47.4 and new business decreasing to 46.3, which represents the most substantial decline in demand since October 2023. While manufacturing output remained steady at 52.2, surpassing expectations of 50.9, this apparent resilience appears largely driven by factories accelerating input purchases in anticipation of further price increases and potential supply disruptions.

Input prices surged to their highest levels since late 2022 (with composite at 68.4 and manufacturing at 76.9), resulting in the sharpest rise in output prices in over three years. The latest figures suggest possible headwinds for Q2 GDP, highlight emerging stagflation risks, and present the ECB with a challenging policy dilemma amid rising inflation and weakening growth. For market participants, these results may reinforce downward pressure on services and cyclical equities while sustaining elevated short-term yields due to more hawkish monetary policy expectations.

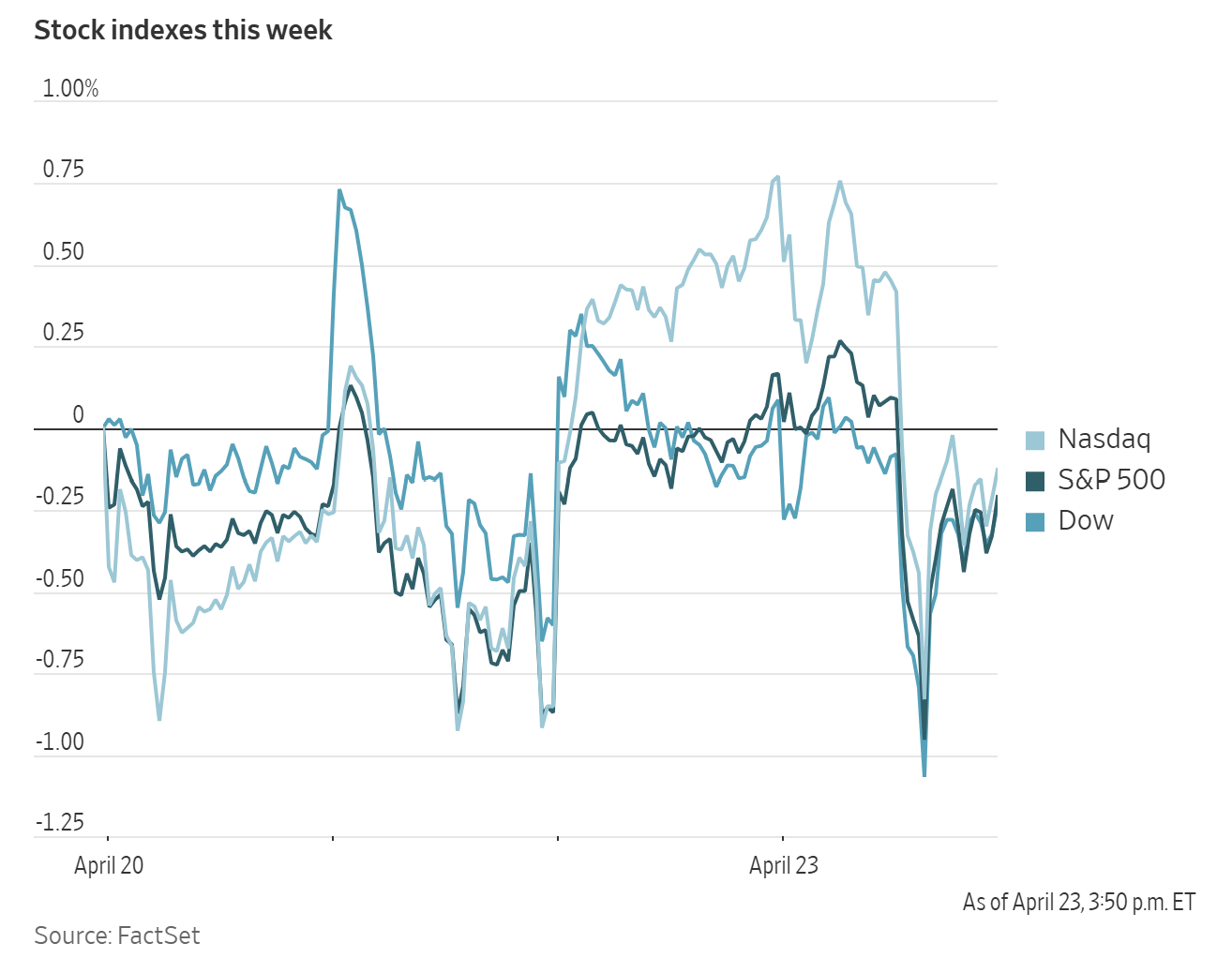

US Stock Indices

Dow Jones Industrial Average -0.36%

Nasdaq 100 -0.57%

S&P 500 -0.41%, with 6 of the 11 sectors of the S&P 500 down

On Thursday, equities declined as investors assessed the latest round of corporate earnings amid an increasingly tense geopolitical climate involving the US, Israel and Iran.

The Nasdaq Composite led the major indices lower, falling -0.89%, while the S&P 500 and Dow Jones Industrial Average declined -0.41% and -0.36%, respectively, with the Dow shedding 179.71 points.

In corporate news, shareholders of Warner Bros. Discovery overwhelmingly approved a merger with Paramount Skydance.

Spirit Aviation Holdings is reportedly in ‘very advanced discussions’ with the US government regarding the terms of a financing arrangement, according to its attorney, Marshall Huebner.

Shares of Super Micro Computer declined sharply after BlueFin Research reported that the server manufacturer had ‘lost a significant contract’ with Oracle.

S&P 500 Best performing sector

Utilities +2.80%, with NextEra Energy +6.94%, NRG Energy +3.30% and Entergy +3.12%

S&P 500 Worst performing sector

Information Technology -1.47%, with ServiceNow -17.75%, Workday -9.42% and Salesforce -8.69%

Mega Caps

Alphabet +0.01%, Amazon -0.11%, Apple +0.10%, Meta Platforms -2.31%, Microsoft -3.97%, Nvidia -1.41% and Tesla -3.56%

Information Technology

Best performer: Texas Instruments +19.43%

Worst performer: ServiceNow -17.75%

Materials and Mining

Best performer: Packaging of America +4.77%

Worst performer: Freeport-McMoRan -8.88%

Corporate Earnings Reports

Posted on Thursday, 23 April from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Intel reported Q1 2026 revenue of $13.6B (+7% Y/Y, beat $12.4B consensus), non-GAAP EPS $0.29 (beat $0.01 consensus). Q2 guidance: revenue $13.8B-$14.8B (beat $13.0B consensus), non-GAAP EPS $0.20 (beat $0.08 consensus), gross margin 39% (beat est). Data Centre & AI revenue $5.05B (beat est), double-digit Y/Y growth. Foundry revenue $5.42B (beat est), improvements ahead of schedule, 2026 capex lifted to match prior year. The CEO noted CPU demand surge from AI inference/agentic workloads.

Freeport-McMoRan reported Q1 adjusted EPS of $0.57 beating estimates of $0.45 and revenue of $6.23B topping $5.76B consensus, despite copper production of 662 million lbs down 24% year-over-year due to reduced capacity in Indonesia operations. The CEO noted growth in revenues, cash flow and earnings versus prior year. Chile committed to 30% faster permitting timelines including for FCX's $7.5B El Abra project with Codelco.

Lockheed Martin reported Q1 earnings that missed Wall Street consensus expectations of $6.72 per share on $18.24 billion revenue, with cash flow turning negative.

American Airlines reported Q1 adjusted EPS of -$0.40, beating estimates of -$0.46, and passenger revenue of $12.50B versus $12.49B consensus. The CEO highlighted record Q1 revenue and track for record Q2 but cut full-year 2026 earnings projections due to surging jet fuel costs. The CEO stated a merger with United Airlines would be bad for customers.

European Stock Indices

CAC 40 +0.87%

DAX -0.16%

FTSE 100 -0.19%

Commodities

Gold spot -0.95% to $4,692.69 an ounce

Silver spot -3.29% to $75.04 an ounce

West Texas Intermediate +4.45% to $97.00 a barrel

Brent crude +4.55% to $106.43 a barrel

Gold prices declined to their lowest level in over a week on Thursday.

Spot gold fell -0.95% to $4,692.69 per ounce, marking its lowest point since 13 April. Earlier in the session, bullion dropped over one percent, reaching an intraday low of $4,663.69 per ounce.

Meanwhile, spot silver decreased -3.29% to $75.04 per ounce, also touching its lowest level in more than a week earlier in the day.

Crude oil futures surged by more than four percent on Thursday following reports that air defences were responding to threats over Tehran, coupled with indications of a power struggle between Iran's hardline and moderate factions.

Brent crude futures closed at $106.43 per barrel, marking an increase of $4.63 or +4.55%, while WTI futures settled at $97.00 per barrel, up $4.13 or +4.45%.

Oil benchmarks briefly turned negative after RIA reported that ongoing talks in Pakistan could yield a breakthrough either tonight or tomorrow. The market subsequently rebounded when President Trump announced via social media that he had instructed the Navy to target any vessel, regardless of size, engaged in mine-laying activities in the Strait.

WTI and Brent prices momentarily spiked to $98.55 and $107.45, respectively, following reports that Iranian parliament Chairman Qalibaf resigned from the negotiating team after intervention by the Islamic Revolutionary Guard Corps (IRGC) and that air defences had been activated over Tehran. Both US and Israeli officials denied any military action directed at Iran, and updates regarding the Qalibaf story remained inconsistent.

In other developments, market participants reported strong demand for WTI Midland in Europe and Asia. Contracted volumes for May shipments to East Asia are more than 4x the 12-month average.

S&P Global Energy has reduced its forecast for global oil demand in 2026 by 700,000 barrels per day (bpd). Product inventories at the port of Singapore declined by 1.8 million barrels w/o/w to 50.139 million barrels.

According to Kpler, crude imports to Asia this month are tracking 22% lower y/o/y at 20.4 million barrels per day, representing an eight-year low. Refinery utilisation in Asia is expected to decrease to 28.4 million bpd this month, compared to 30.4 million bpd in March, based on data from Energy Aspects. Key concerns continue to centre on jet fuel supplies.

Note: As of 4 pm EDT 23 April 2026

Currencies

EUR -0.20% to $1.1685

GBP -0.26% to $1.3465

Bitcoin -1.09% to $77,929.84

Ethereum -3.19% to $2,326.67

The US dollar strengthened and was poised for a weekly advance on Thursday, as heightened tensions between Tehran and Washington intensified uncertainty in the Middle East and diminished prospects for a peace agreement.

The dollar index increased by +0.19% to 98.79.

The euro declined by -0.20% to $1.1685, having earlier reached its lowest level since 13 April. The single currency is set for its first weekly loss in four weeks. The British pound dropped -0.26% to $1.3465.

The Japanese yen weakened by -0.14% against the US dollar to ¥159.64 per dollar, approaching the ¥160 threshold that many market participants consider a trigger for official intervention. The BoJ is anticipated to maintain its current interest rates next week but has signalled a possible rate increase in June.

Fixed Income

US 10-year Bond +2.2 basis points to 4.329%

German 10-year Bund -0.3 basis points to 3.011%

UK 10-year gilt +4.2 basis points to 5.197%

US Treasury prices declined on Thursday during relatively stable trading, as investors remained cautious about making significant moves amid rising tensions and a fragile ceasefire between Washington and Tehran.

The yield on the 10-year Treasury note increased by +2.2 bps to 4.329%, while the 30-year yield rose by +1.1 bps to 4.904%.

At the shorter end of the yield curve, the two-year Treasury yield, sensitive to Fed fund rate expectations, advanced by +4.0 bps to 3.846%.

Analysts noted strong demand at the US Treasury’s auction of $26 billion in five-year Treasury Inflation-Protected Securities (TIPS). These securities were priced at 1.367%, marginally higher than the anticipated rate at the time of the auction, indicating that investors required a slight premium. The bid-to-cover ratio stood at 2.57x, surpassing the six-auction average of 2.41x.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 9.7 bps of rate cuts in 2026, lower than the 8.3 bps priced in a week ago. Fed funds futures traders are now pricing in a 1.0% probability of a 25 bps rate hike at the 29 April FOMC meeting, higher than last week’s 0.0% probability.

Short-term bond yields in the eurozone retreated following three consecutive daily increases, as lackluster economic data earlier in the session prompted the reversal.

Germany’s two-year yields, closely tied to ECB rate expectations, declined by -2.9 bps to 2.562%.

Germany’s 10-year government bond yield fell by -0.3 bps to 3.011%, while the 30-year yield at the longer end of the curve slipped by -0.4 bps.

On Wednesday, European Central Bank chief economist Philip Lane stated that the ECB cannot determine whether the economic shock from the Iran conflict will be temporary or more significant until the duration of the turmoil is clearer.

Money markets have priced in an ECB deposit facility rate of 2.61% by year-end, implying two 25 bps rate hikes and approximately a 45% probability of a third increase, compared to around 2.35% late last Friday.

Italy’s 10-year BTP underperformed, with yields rising +0.6 bps to 3.783%. The spread between BTPs and bunds stood at 77.2 bps.

Note: As of 4 pm EDT 23 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.