Are European and UK risk premia justified?

What to look out for today

Companies reporting on Monday, 18 May: Baidu

Key data to move markets today

EU: German Bundesbank ‘Buba’ Monthly Report

UK: Speeches by BoE External members Megan Greene and Catherine Mann

JAPAN: GDP and GDP Product Deflator

CHINA: Industrial Production and Retail Sales

Global Macro Updates

Headwinds for UK and European assets in focus this week. Political uncertainty was the principal driver of UK market volatility last week, as an ongoing leadership crisis following the huge loss of councilors in recent local elections placed Prime Minister Starmer under pressure and pushed gilt yields to multi-decade highs. The 10-year gilt yield rose above 5.10%, the 30-year yield reached levels not seen since 1998 and sterling recorded its weakest weekly performance in more than a year. This reflected rising investor concerns over fiscal credibility in the event of a leadership transition toward a more left-leaning successor. Analysts have cautioned that the emergence of a more interventionist candidate could trigger a sharp and immediate repricing in the gilt market. By the end of last week, Manchester Mayor Andy Burnham had positioned himself to qualify for Labour party leadership by running for a position as member of parliament (MP) through a by-election in Makerfield, on the edges of greater Manchester. However, polling showed the right-wing populist and national-conservative party political group, Reform, leading Labour by 46% to 35% in a constituency held by Labour since 1983, further increasing political risk premia.

Against this challenging domestic backdrop, the BoE faced a more complex policy environment as markets repriced the outlook in response to energy-driven inflation risks. BoE Chief Economist Huw Pill signalled a preference for modest further tightening, while MPC member Catherine Mann warned that elevated volatility could feed through into broader financial conditions. By mid-week, rate markets were pricing approximately 68 bps of tightening by year-end, up from around 56 bps at the start of the week, largely reflecting higher energy costs. Simultaneously, domestic data has deteriorated further: retail sales have declined sharply, consumer confidence has fallen to multi-year lows and card spending has weakened as households curtail discretionary expenditure. Labour market conditions have softened, with weaker hiring activity and rising redundancies, while housing sentiment remained under pressure due to high mortgage rates. Although GDP and PMI releases indicated some areas of resilience, much of that strength was seen as front-loaded, and survey evidence continues to point to subdued demand and a rising risk of recession.

The conflict in Iran also continues to weigh on the eurozone outlook, reinforcing the ECB’s stagflation debate. Although official rhetoric remains measured, several policymakers have warned that oil-driven inflation could de-anchor inflation expectations and ultimately necessitate additional policy tightening. Incoming data also confirmed a loss of momentum. In Germany, sentiment remained fragile despite a temporary rebound in the ZEW survey. The economy ministry warned that higher energy costs and persistent uncertainty could materially weaken Q2 growth. In France, unemployment has risen to 8.1%, underscoring a deterioration in labour market conditions. Broader structural pressures have also intensified, with EU business investment falling to an 11-year low amid geopolitical and regulatory uncertainty. Meanwhile, energy-related strains remained evident, as reports point to greater dependence on US LNG, record levels of solar curtailment and ongoing debate over gas storage flexibility.

Beijing summit day two. The US President departed Beijing on Friday afternoon following his second meeting with President Xi. The overall tone of the summit remained cordial, with Xi stating that both sides had agreed to stabilise trade ties and had reached important areas of consensus. President Trump said the two countries had made ‘some fantastic trade deals.’

Iran was also a prominent topic in the discussions. President Trump said the two sides held broadly similar views on the need to end the war, agreed that Iran must not obtain a nuclear weapon and supported reopening the Strait of Hormuz. Even so, no clear framework or concrete next steps were presented for how such an outcome would be achieved.

On Sunday the White House said that, “President Trump and President Xi agreed that the United States and China should build a constructive relationship of strategic stability on the basis of fairness and reciprocity.” In a factsheet, Presidents Trump and Xi agreed in Beijing to establish a board of trade and a board of investment, in one of several measures to promote “strategic stability” in US - China relations. According to the White House, the trade board will allow the two sides to manage issues “across non-sensitive goods.” According to Bloomberg news, Treasury Secretary Scott Bessent has said one idea for the trade council was to remove tariffs on about $30 billion worth of commerce “for non-critical areas and areas that we’re not trying to reshore.” China has already agreed to buy at least $17 billion of agricultural products annually through 2028 in addition to the soybean-purchase commitments made last fall when China initially pledged to buy 12 million metric tons of soy after Trump’s meeting with Xi last year, and the US said at the time that Beijing would buy 25 million tons annually for three years. China has now also agreed to restore market access for American beef by lifting restrictions.

The US President had said on Thursday that China would purchase 200 Boeing aircraft. The announcement was notable, but it fell short of prior market expectations, as earlier reporting from Bloomberg news in March had indicated that Boeing had been nearing a substantially larger order that could be unveiled during the Beijing visit.

As noted by the Financial Times, the factsheet said China had agreed to address US concerns about supply chain shortages for rare earths and critical minerals, including yttrium, scandium, neodymium and indium, and that Beijing would also respond to issues the US had raised regarding bans or restrictions on the sale of rare earth production and processing equipment and technology.

Looking ahead, President Trump extended an invitation for Xi to visit the US in September, while the two leaders could also meet again at the APEC and G20 summits later this year. Chinese media highlighted Xi’s reference to ‘constructive strategic stability’ in describing bilateral relations, suggesting that Beijing is seeking a more stable framework for ties, at least through the remainder of President Trump’s current term.

US Stock Indices

Dow Jones Industrial Average -1.07%

Nasdaq 100 -1.54%

S&P 500 -1.24%, with 10 of the 11 sectors of the S&P 500 down

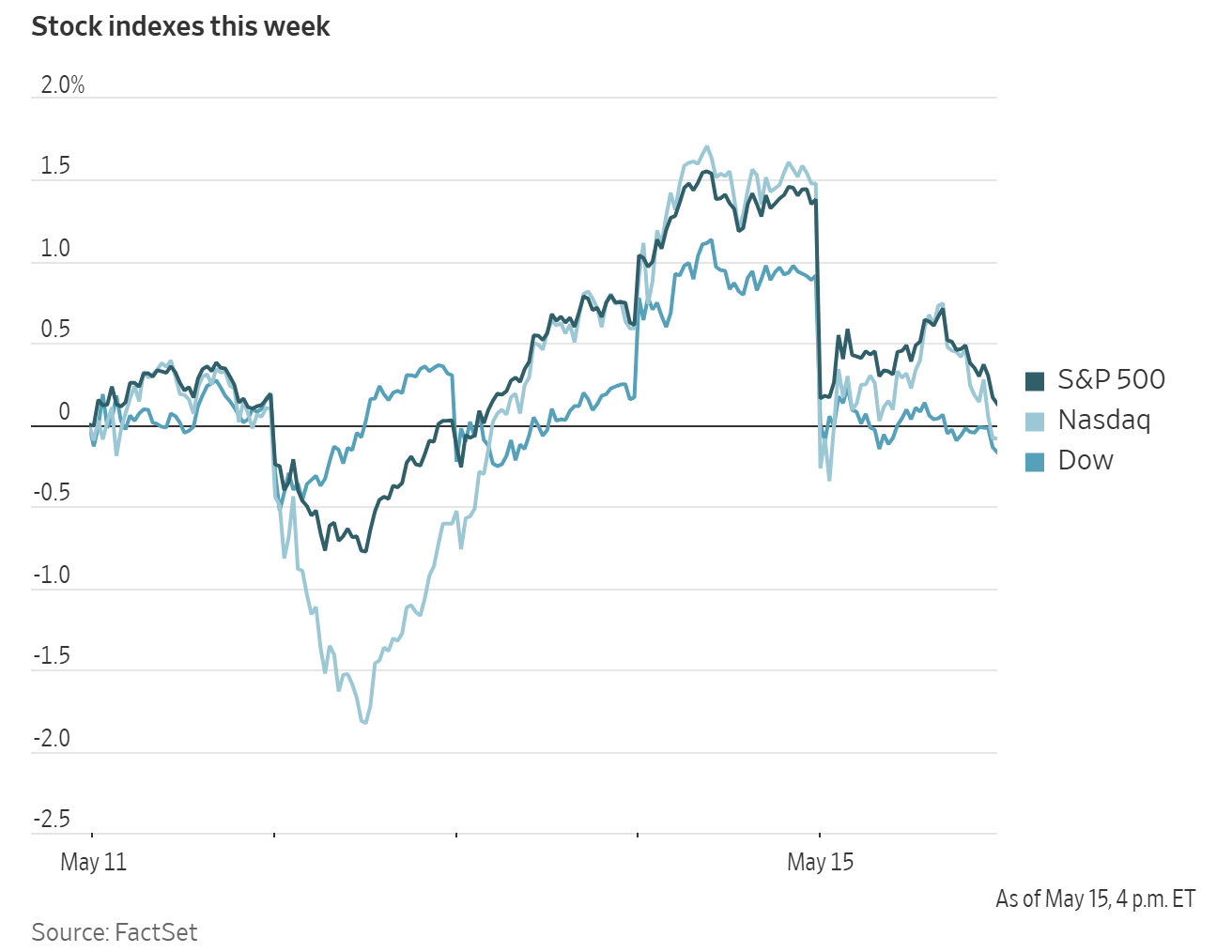

The Nasdaq Composite was -1.54%, or -410.08 points to 26,225.14 and the S&P 500 declined -1.24%, or -455.10 points to 7,408.50. The Dow Jones was -1.07%, or -537.29 points, to 49,526.17.

For the week, the S&P 500 advanced +0.13%, the Nasdaq Composite declined -0.62% and the Dow Jones Industrial Average increased +0.92%.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q1 2026 is projected to be +28.3%. This jumps to +29.6% when excluding the Energy sector. Of the 452 companies in the S&P 500 that have reported earnings to date for Q1, 83.0% have reported earnings above analyst estimates, with 78.6% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 11.1% in Q1, increasing to 11.6% when excluding the Energy sector.

Information Technology at 98.2%, is the sector with most companies reporting above estimates. Additionally, Energy with a surprise factor of 19.0%, is the sector that has beaten earnings expectations by the highest surprise factor. Within Communication Services, 36.8% of companies have reported below estimates. Alongside Real Estate, it is also the sector with the smallest surprise factor, exceeding estimates by 2.5%. The S&P 500 surprise factor is 8.2%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.6x.

19 S&P 500 companies are scheduled to release their Q1 earnings reports this week.

In corporate news, SpaceX is reportedly preparing to file publicly for its long-anticipated IPO as early as Wednesday, according to people familiar with the matter, as reported by Reuters.

Pershing Square has established a new stake in Microsoft, taking advantage of a decline in the company’s share price to invest in a business it believes is stronger and more resilient than the market currently recognises.

The US President said he discussed AI guardrails with Chinese President Xi Jinping and added that Nvidia’s H200 chips were also raised during the two-day summit in Beijing.

Boeing appears to have secured its long-awaited order from China during President Trump’s visit to the country, although the details of the agreement remain unclear, including the number of aircraft, the models involved and the expected timing.

Alphabet sold ¥576.5 billion ($3.6 billion) of bonds in the largest-ever yen-denominated deal by a non-Japanese issuer, as competition to fund data centres and AI infrastructure continues to intensify.

S&P 500 Best performing sector

Energy +2.32%, with APA +5.04%, Occidental Petroleum +4.89% and Devon Energy +4.76%

S&P 500 Worst performing sector

Materials -2.74%, with Newmont -6.25%, Albemarle -5.61% and Smurfit Westrock -5.28%

Mega Caps

Alphabet -0.97%, Amazon -1.15%, Apple +0.68%, Meta Platforms -0.68%, Microsoft +3.05%, Nvidia -4.42% and Tesla -4.77%

Information Technology

Best performer: Enphase Energy +10.16%

Worst performer: Corning -7.91%

Materials and Mining

Best performer: FMC +4.50%

Worst performer: Newmont -6.25%

European Stock Indices

CAC 40 -1.60%

DAX -2.07%

FTSE 100 -1.71%

Commodities

Gold spot -2.40% to $4,538.02 an ounce

Silver spot -9.02% to $75.95 an ounce

West Texas Intermediate +3.57% to $105.66 a barrel

Brent crude +2.44% to $109.21 a barrel

Gold fell to its lowest level in more than a week on Friday as US Treasury yields and the dollar strengthened, while rising inflation concerns stemming from the war in Iran reinforced expectations of higher interest rates.

Spot gold declined -2.40% to $4,538.02 per ounce after touching its lowest level since 4 May earlier in the session. For the week, prices fell -3.74%.

Spot silver dropped -9.02% to $75.95 per ounce, bringing its weekly decline to -5.44%.

Oil prices rose by more than two percent on Friday after remarks from the US President and Iran’s foreign minister further reduced hopes for an agreement to halt ship attacks and seizures around the Strait of Hormuz.

Brent crude futures settled at $109.21 per barrel, up $2.60, or +2.44%, while US WTI futures closed at $105.66 per barrel, up $3.64, or +3.57%.

Over the course of the week, Brent rose +8.69% and WTI advanced +11.60%, driven by uncertainty surrounding the fragile ceasefire in the Iran conflict.

Crude oil and refined products continued to trade higher as the ceasefire entered its fifth week, with Washington and Tehran still appearing no closer to an agreement. Additional support came after the US President stated that his patience with Iran was wearing thin, while expectations that China could help encourage Tehran toward an understanding also began to fade.

On Wednesday, WTI and Brent moved higher after sources close to the US President said he was leaning toward resuming military action against Iran. The President also stated that his decisions on Iran would not be influenced by the domestic financial impact, including gasoline prices. Some downward pressure emerged from reports that tanker traffic through the Strait had increased relative to prior weeks. Key concerns during the week included declining oil-on-water levels and the end of Strategic Petroleum Reserve releases just as summer demand begins to strengthen. Traders added that the physical market strengthened steadily throughout the week.

Shipping analytics firm Kpler reported on Thursday that 10 ships had passed through the strait over the previous 24 hours, compared with five to seven vessels per day in recent weeks.

In an effort to reduce reliance on the Strait of Hormuz, the UAE announced plans to expand pipeline capacity to the port of Fujairah by at least 1.5 million barrels per day (bpd). Most market participants expect other producers, including those using Saudi Arabia’s East-West pipeline, to make similar announcements.

Ukraine continued to target Russian energy infrastructure, striking at least two additional refineries during the week.

Note: As of 4 pm EDT 15 May 2026

Currencies

EUR -0.39% to $1.1623

GBP -0.62% to $1.3320

Bitcoin -3.02% to $78,927.48

Ethereum -3.31% to $2,220.96

The dollar strengthened for a fifth consecutive session on Friday and had its largest weekly percentage gain in two months.

The dollar index rose +0.41% to 99.27 after reaching 99.30 earlier in the session, while the euro declined -0.39% to $1.1623 after touching a five-week low of 1.1617.

The dollar’s five-day advance marks its longest run of gains since late March, lifting the index +1.46% over the week. By contrast, the euro fell -1.37% on a weekly basis, recording its sharpest decline in two months.

Against the Japanese yen, the dollar gained +0.27% to ¥158.76. Data released on Friday showed that Japan’s wholesale inflation accelerated in April at its fastest pace in three years, as the war in Iran pushed up oil and chemical goods prices, reinforcing the case for the BoJ to raise interest rates as early as June.

The yen weakened -1.35% over the week, moving back toward the ¥160 level that triggered intervention by Japanese authorities the prior week.

Sterling fell -0.62% to $1.3320 after touching a five-week low of $1.3313, as Prime Minister Keir Starmer faced mounting political pressure in his effort to remain in office. For the week, the pound declined -2.29%, its largest weekly drop since November 2024.

Fixed Income

US 10-year Bond +10.7 basis points to 4.596%

German 10-year Bund +12.7 basis points to 3.170%

UK 10-year gilt +18.8 basis points to 5.182%

US Treasury yields climbed to their highest levels in a year on Friday, as a surge in oil prices linked to ongoing energy disruptions in the Middle East, persistent inflation concerns and expectations of stronger economic growth prompted investors to reassess the likely path of interest rates.

The 2-year note yield, which is closely aligned with expectations for Fed policy, rose +4.5 bps to 4.075%, its highest level since March 2025.

The yield on the US 10-year note increased +10.7 bps to 4.596%, marking its highest level since May 2025.

The 30-year bond yield rose +8.8 bps to 5.120%, also its highest level since May 2025 and its largest one-day increase since the same month.

Over the week, the 2-year yield advanced +18.0 bps, the 10-year yield climbed +23.7 bps and the 30-year yield rose +18.0 bps.

The US Treasury yield curve, measured by the spread between the 2-year and 10-year notes, steepened over the week as the spread widened 5.7 bps to 52.1 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 15.1 bps of rate hikes in 2026, higher than the 1.0 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.8% probability of a 25 bps rate cut at June’s FOMC meeting, lower than last week’s 6.6% probability.

Bond markets are preparing for a degree of interest-rate pressure not seen in decades, as investors assess the economic costs of the war with Iran and how those burdens may be absorbed by the global economy.

Although the bond sell-off was global in scope, several of its drivers were at least partly domestic. UK gilt yields rose sharply again, reaching their highest levels in decades, as pressure intensified on Prime Minister Keir Starmer to resign following the Labour Party’s heavy losses in local elections and the emergence of new challengers. The UK 10-year yield rose +27.0 bps over the week after increasing +18.8 bps on Friday to 5.182%.

Yields across the eurozone moved higher, while Japanese government bond yields reached record levels following a stronger-than-expected wholesale inflation reading that reinforced expectations of further rate increases from the Bank of Japan. Over the week, Japan’s 10-year yield rose +22.9 bps from 2.476% to 2.705%.

Italian 10-year bonds were among the weakest performers in the euro zone, with yields rising +14.2 bps to around 3.930%, bringing the weekly increase to +19.8 bps. The 10-year German Bund yield rose +12.7 bps on Friday to 3.170%, taking its weekly rise to +16.3 bps. The spread between Italy’s 10-year BTPs and Bunds stood at 76.0 bps, up 3.5 bps from 72.5 bps the previous week.

The 2-year Shatz yield advanced +9.0 bps to 2.750%, contributing to a weekly rise of +15.2 bps. On the long-end of the maturity spectrum, the 30-year yield rose +13.3 bps last week, following an increase of +9.5 bps on Friday to 3.676%.

France’s 10-year OAT yields rose +13.2 bps on Friday, marking a weekly increase of +17.4 bps to 3.803%.

Note: As of 4 pm EDT 15 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.