Will the BoE hold as UK policy shifts?

Key data to move markets today

EU: German PPI and speeches by ECB Executive Board members Frank Elderson and Piero Cipollone and ECB Chief Economist Philip Lane

UK: Retail Sales and Retail Sales ex-Fuel

USA: US markets will be closed in observance of Juneteenth

Global Macro Updates

Burnham wins key UK by-election, setting the stage for a leadership challenge. Andy Burnham won the Makerfield by-election with 55% of the vote, strengthening his position for a possible challenge to UK Prime Minister Keir Starmer. In his victory speech, Burnham said the result represented the Labour Party’s final opportunity to change. Attention is now likely to turn to whether Starmer sets out a timetable for his departure and an orderly leadership transition.

Starmer has repeatedly said that he intends to contest any leadership challenge. The London Times reported that he has built a six-figure campaign fund, while advisers have made extensive preparations to present his case to Labour Party members. According to The Guardian, Starmer could face a formal challenge within the next week if he does not outline a departure plan. Burnham and former Health Secretary Wes Streeting are both expected to enter the contest.

Bloomberg news reported that Burnham has expanded his group of economic advisers ahead of a widely expected leadership bid. The team includes former BoE Chief Economist Andy Haldane, former Goldman Sachs Chief Economist Jim O’Neill, former IPPR Executive Director Carys Roberts and former OBR Chair Richard Hughes.

Investors remain cautious over the possibility that Burnham could support looser fiscal policy. The Telegraph noted that his positions on fiscal rules, bond markets, rejoining the EU and benefits for migrants have either shifted or softened, leaving some backers uncertain about his precise policy stance. Some Labour MPs are also concerned that he would face the same economic constraints as Starmer and could ultimately adopt a similar governing programme.

BoE leaves rates unchanged and keeps policy options open. The BoE left its key Bank Rate unchanged at 3.75% in a 7 - 2 vote, in line with expectations. The statement noted that global energy prices have declined since the previous meeting, but emphasised that the broader impact of the energy shock on the UK economy remains uncertain. Policymakers maintained their expectation that inflation will pick up later this year and highlighted the risk of material second-round effects in price and wage setting. The Committee reiterated that the required policy stance will depend on the scale and duration of the shock.

The minutes also showed that median expectations in the market participants survey point to unchanged policy over the year ahead. This represents a tightening of around 50 bps in the median rate path relative to expectations before the conflict, reinforcing the view that tighter financial conditions have done much of the work for the BoE. Some sell-side economists have also begun to flag the possibility that rates remain unchanged for the rest of the year.

The discussion also highlighted several macroeconomic considerations. Policymakers noted that weaker demand and a softer labour market should help limit the strength of second-round effects. Recent data provided greater reassurance that sustained disinflation had been underway before the conflict, while wage growth was described as close to levels consistent with the inflation target. However, forward-looking indicators suggest that the pace of wage moderation could stall. The MPC lowered its estimate of peak inflation to 3.25% in Q4, compared with its previous forecast of 3.6%.

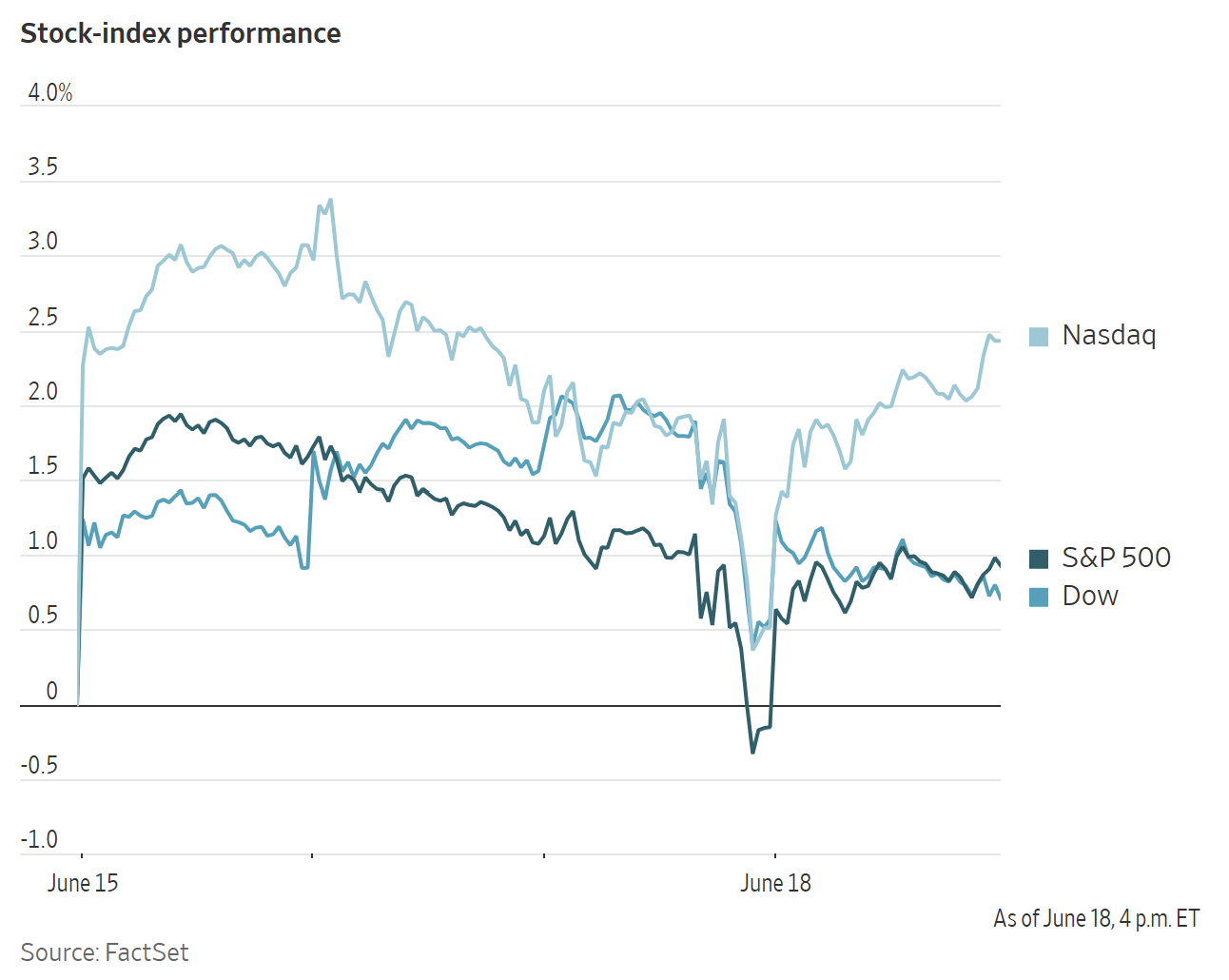

US Stock Indices

Dow Jones Industrial Average +0.14%

Nasdaq 100 +2.48%

S&P 500 +1.08%, with 5 of the 11 sectors of the S&P 500 up

In Thursday trading, the S&P 500 gained +1.08%. The Dow Jones Industrial Average added +0.14%, or 72.15 points. The Nasdaq Composite advanced +1.91%. All three indexes ended the week higher, led by the Nasdaq Composite, which was up +2.43%, followed by the S&P 500 advancing +0.93% and the Dow Jones Industrial Average at +0.71%. US markets will be closed today in observance of Juneteenth.

Thursday’s gains marked a sharp reversal from Wednesday’s selloff, which was triggered by the Fed’s stronger-than-expected pivot toward raising rates. In his first press conference as Fed Chair, Kevin Warsh emphasised that central bank officials are ‘unambiguously and unanimously’ committed to bringing inflation back to the Fed’s 2% target.

In company news, Intel surged after the US President said the chipmaker will work with Apple to design and produce semiconductors domestically.

Moody's Ratings assigned SpaceX a Baa1 rating late Thursday. The grade puts the space-exploration company comfortably in investment grade status, three notches above speculative grade, or ‘junk’, helping keep borrowing costs down if SpaceX wants to sell bonds on the public market. Moody's cited as strengths SpaceX's recurring revenue from satellite network Starlink and strategic importance as the primary launch provider for NASA and the Defense Department. Reuters reported that bankers for SpaceX are preparing to hold calls with investors as soon as next week to discuss a potential $20 billion bond offering, according to people with knowledge of the matter.

S&P 500 Best performing sector

Information Technology +2.68%, with Corning +11.13%, Intel +10.64% and Super Micro Computer +10.37%

S&P 500 Worst performing sector

Energy -1.73%, with SLB -4.45%, Halliburton -3.59% and ConocoPhillips -3.12%

Mega Caps

Alphabet +1.48%, Amazon +2.90%, Apple +0.70%, Meta Platforms +1.70%, Microsoft +0.13%, Nvidia +2.95% and Tesla +1.04%

Information Technology

Best performer: Corning +11.13%

Worst performer: Accenture -17.97%

Materials and Mining

Best performer: Martin Marietta Materials +3.05%

Worst performer: Steel Dynamics -7.49%

European Stock Indices

CAC 40 +0.44%

DAX +0.37%

FTSE 100 -1.04%

Commodities

Gold spot -1.15% to $4,208.59 an ounce

Silver spot -2.82% to $65.76 an ounce

West Texas Intermediate +1.20% to $76.56 a barrel

Brent crude +0.89% to $79.41 a barrel

Gold fell on Thursday. Spot gold was down -1.15% at $4,208.59 per ounce. Prices touched their lowest since November 2025 last week.

The US dollar climbed after the FOMC policy statement and touched a one-year high on Thursday, making greenback-priced bullion more expensive for overseas buyers.

Spot silver fell -2.82% to $65.76 per ounce.

Crude prices rose on Thursday, despite signs of improving market access through the Strait of Hormuz and ongoing concerns over global supply conditions.

Brent crude futures settled at $79.41 a barrel, up 70 cents, or +0.89%, while US WTI gained 91 cents, or +1.20%, to close at $76.56 a barrel.

The move followed a 14-point memorandum of understanding between the US and Iran, which established a 60-day negotiation period. Under the agreement, Iran will allow toll-free passage through the Strait of Hormuz, with traffic through the waterway expected to return to full capacity within 30 days.

Despite Thursday’s gains, crude benchmarks remained near their lowest levels since the first trading session after the war began. The US - Iran agreement has eased concerns over restricted shipping through the Strait of Hormuz while both sides continue to negotiate the details of a broader peace arrangement over the coming 60 days.

Market conditions appear to be loosening, with traffic through the strait improving, global jet-fuel prices declining, Gulf producers restarting output and regional crude premiums retreating to pre-war levels. However, many market participants expect it may take several weeks or months for shipping and production volumes to fully normalise, as shipowners will need to regain confidence that passage is safe.

Supply data also remained supportive. The DOE Weekly Petroleum Status Report showed another sizable draw in combined commercial crude and Strategic Petroleum Reserve inventories, while Cushing stockpiles moved closer to operationally critical levels. Combined commercial crude and SPR inventories are now at their lowest levels in more than 40 years.

Additional supply risks persisted as Ukrainian strikes on Russian refineries accelerated this week, building on an already elevated pace of attacks. Russian refinery utilisation is now estimated by some market observers to be firmly below 4.0 million bpd.

In Asia, China’s refinery throughput fell last month to a 45-month low. Official production, import and throughput data also suggest that China drew down stockpiles by around 500,000 bpd in May, marking the first inventory draw since the start of the war.

In the UAE, according to S&P Global, inventories at Fujairah declined 4.3% in the week ended 15 June to a record low of 5.145 million barrels, according to Fujairah Oil Industry Zone (FOIZ) data published on 17 June. Stocks of light distillates, including gasoline and naphtha, fell 33% to an all-time low of 1.376 million barrels. Inventories have now declined every week since the week ended February 16, according to FOIZ.

Signs of a production recovery are also emerging in the Gulf. Kuwait Petroleum Corp. (KPC) expects output to rise back above 2.0 million bpd within a week and to return to pre-war levels within a few weeks. Kuwait’s production averaged 573,000 bpd in May, according to the latest OPEC Monthly Oil Market Report. The updated timeline compares with KPC’s earlier guidance during the war that output would take about a month to recover to 2.0 million bpd.

Bloomberg news reported that oil production in southern Iraq has increased to around 1.5 million to 1.6 million bpd, from roughly 900,000 to 1.0 million bpd, as the resumption of cargo loadings frees up storage capacity. Separately, East Asian refiners are said to be increasing fuel exports after months of prioritising domestic sales, with spot offerings rising.

Middle Eastern crude premiums have also fallen back to pre-war levels. Reuters reported that tanker data showed that three fully laden Saudi VLCCs, along with three other tankers with active transponders, passed through the Strait of Hormuz on Wednesday, adding to the increase in volumes seen earlier in the week.

Longer term, China, the world’s second-largest oil consumer, is forecast to consume 753 million metric tons of oil in 2026, down 4.9% from 2025, as the country shifts further toward new energy sources and contends with elevated oil prices, according to a report from PetroChina’s research unit.

Note: As of 4 pm EDT 18 June 2026

Currencies

EUR -0.37% to $1.1461

GBP -0.58% to $1.3203

Bitcoin -2.01% to $62,895.64

Ethereum -1.77% to $1,706.49

The US dollar index rose to a one-year high on Thursday, as a hawkish shift from the Fed prompted traders to increase expectations for additional rate hikes this year. The move pressured the yen to its weakest level in two years and drew renewed warnings from Japanese officials.

A firmer US growth outlook has reinforced those expectations, with the past three payrolls reports showing monthly job gains well above economists’ forecasts.

Separate data released Thursday showed that initial jobless claims declined last week, indicating that layoffs remain limited.

Against that backdrop, the euro fell -0.37% to $1.1461, while sterling declined -0.58% to $1.3203. Both currencies touched their lowest levels in more than two months.

The dollar index advanced +0.40% to 100.79, its highest level since May 2025, after gaining +0.83% in the previous session, its largest one-day increase in more than three months.

The Japanese yen traded -0.46% lower to ¥161.28 on Thursday, after it weakened as far as ¥161.45 per dollar, its lowest level since July 2024 and erasing the gains made after Tokyo’s intervention on 30 April. A move beyond the pair’s 2024 high of ¥161.99 would leave the yen at its weakest level since 1986.

Fixed Income

US 10-year Bond -4.0 basis points to 4.460%

German 10-year Bund +0.1 basis points to 2.932%

UK 10-year Gilt +1.0 basis points to 4.768%

US Treasury yields declined on Thursday, reversing part of the prior session’s move after investors interpreted Fed Chair Kevin Warsh’s first policy meeting as hawkish, pushing short-term yields to their highest levels in 16 months.

The 2-year yield, which is most sensitive to expectations for Fed policy changes, fell -0.8 bps to 4.187% on Thursday after reaching 4.207% on Wednesday.

The 10-year yield declined -4.0 bps to 4.460%, while the 30-year yield fell -3.5 bps to 4.898% at the long end of the curve.

The move left the 2s10s curve flatter at 27.3 bps from Wednesday’s 30.5 bps, reflecting a bear-flattening bias.

A 5-year TIPS auction was well received, with the yield declining 3.3 bps to 1.910%.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 38.6 bps of rate hikes in 2026, lower than the 18.5 bps priced in a week ago. Fed funds futures traders are now pricing in a 39.6% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 8.3% last week.

Eurozone government bond yields were broadly steady on Thursday, as investors assessed a hawkish shift from the Fed during a busy week for global central banks.

Germany’s 10-year Bund yield was +0.1 bps higher at 2.932%, following five consecutive sessions of declines. This rally marked its longest downward run since mid-February.

Central-bank decisions remained a key focus. The SNB and the BoE both kept policy unchanged on Thursday, with the BoE holding the Bank Rate at 3.75% and the SNB leaving its policy rate at 0.0%. By contrast, the ECB raised rates last week to 2.25% from 2.00%, while the BoJ followed earlier this week by lifting its uncollateralised overnight call rate by 0.25 bps to 1.0%.

In the UK, the 2-year gilt yield rose +4.8 bps to 4.203%, while the 10-year yield increased +1.0 bps to 4.768%.

Speaking at an event hosted by Deutsche Bank on Thursday, ECB Chief Economist Philip Lane suggested that last week’s rate increase may not yet have begun to restrict growth. He also indicated that the eurozone economy may be able to tolerate slightly higher interest rates without losing momentum, with bond-market pricing implying that the upper end of the neutral range for the ECB’s deposit rate has risen to 2.50% from 2.25%.

‘Even when the price of oil is falling now, the price of food, we think, will go up and the price of goods and services,’ Lane said. ‘So the overall inflation dynamic, we do think, is going to be a prolonged period of above-target inflation.’

Money markets were last pricing in at least one additional ECB rate increase this year, with some probability assigned to a second move.

At the front end of the German curve, the 2-year yield, more sensitive to shifts in rate and inflation expectations, rose +2.1 bps to 2.616%. At the long end, the 30-year Bund yield declined -1.4 bps to 3.467%.

Italy’s 10-year BTP yield was unchanged at 3.629%, leaving the spread over comparable Bunds at 69.7 bps.

Note: As of 4 pm EDT 18 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.