Trade fog, slower tides

What to look out for today

Companies reporting on Monday, 23rd February: Diamondback Energy, Dominion Energy, Domino’s Pizza, ONEOK

Key data to move markets today

Europe: German IFO Business Climate, Current Assessment and Expectations and Italian CPI

UK: A speech by BoE External Member Alan Taylor

USA: Factory Orders and a speech by Fed Governor Christopher Waller

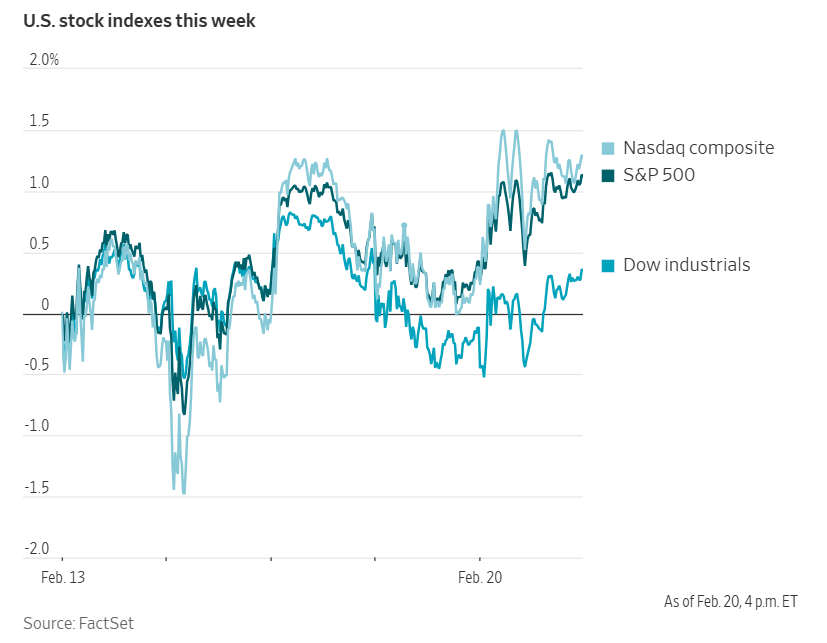

US Stock Indices

Dow Jones Industrial Average +0.47%

Nasdaq 100 +0.87%

S&P 500 +0.69%, with 9 of the 11 sectors of the S&P 500 up

The Dow Jones Industrial Average advanced by 230.77 points, or +0.47%, to 49,625.97, while the S&P 500 and Nasdaq Composite rose +0.69% and +0.87%, respectively. The S&P 500 marked its strongest weekly performance since 9th January.

For the week, all major US equity indices traded higher. The S&P 500 +1.07%, the Nasdaq Composite +1.51%, and the Dow Jones Industrial Average +0.25%.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q4 is projected to be +13.9%. This jumps to +14.3% when excluding the Energy sector. Of the 423 companies in the S&P 500 that have reported earnings to date for Q4 2025, 72.6% have reported earnings above analyst estimates, with 71.8% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 8.8% in Q4, increasing to 9.6% when excluding the Energy sector.

Information Technology at 92.6%, is the sector with most companies reporting above estimates. Additionally, with a surprise factor of 7.5%, it is the sector that has beaten earnings expectations by the highest surprise factor. Within Consumer Discretionary, 44.7% of companies have reported below estimates. Industrials is the sector with the lowest surprise factor, falling short of estimates by -0.3%. The S&P 500 surprise factor is 5.1%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.9x.

55 S&P 500 companies, and 3 Dow Jones constituents, are scheduled to release their Q4 earnings reports this week.

In corporate news, Paramount Skydance announced that there is ‘no statutory impediment’ in the US preventing the completion of its proposed $77.9 billion acquisition of Warner Bros. Discovery.

The Securities and Exchange Commission confirmed that its investigation into mobile advertising technology company AppLovin remains active and ongoing.

Lucid Group is reducing its workforce in response to the challenges faced by the EV manufacturer throughout 2025.

S&P 500 Best performing sector

Communication Services +2.65%, with Alphabet +3.74%, Match Group +3.71%, and Live Nation Entertainment +3.31%

S&P 500 Worst performing sector

Energy -0.71%, with Exxon Mobil -2.44%, Coterra Energy -1.36%, and SLB -1.34%

Mega Caps

Alphabet +3.74%, Amazon +2.56%, Apple +1.54%, Meta Platforms +1.69%, Microsoft -0.31%, Nvidia +1.02%, and Tesla +0.03%

Information Technology

Best performer: Corning +7.32%

Worst performer: Akamai Technologies -14.07%

Materials and Mining

Best performer: Freeport-McMoRan +2.83%

Worst performer: Dow -2.77%

Corporate Earnings Reports

Posted on Friday, 20th February

PPL quarterly revenue +2.9% to $2.274 bn vs $2.420 bn estimate

EPS at $0.74 vs $0.73 estimate

Vincent Sorgi, President and CEO, said, “As the energy landscape continues to transform at an unprecedented pace, PPL continues to evolve and adapt to meet challenges and embrace opportunities. In 2025, we achieved our targeted earnings per share and dividend growth, completed $4.4 billion in infrastructure investments to improve service to our customers and exceeded our targeted annual O&M savings to help keep energy affordable. Across PPL, we also continued to advance our strategy to create the utilities of the future – utilities that are stronger, smarter, cleaner and more efficient. In fact, despite significantly heightened storm activity in all of our service territories, our companies delivered top-quartile or near-top-quartile reliability in 2025. This performance is a direct result of investments we’re making in our electricity and gas networks and Kentucky power plants.” — see report.

European Stock Indices

CAC 40 +1.39%

DAX +0.87%

FTSE 100 +0.56%

Commodities

Gold spot +2.19% to $5,103.49 an ounce

Silver spot +7.67% to $84.57 an ounce

West Texas Intermediate -0.70% to $66.31 a barrel

Brent crude -0.42% to $71.64 a barrel

Spot gold rose +2.19% on Friday to reach $5,103.49 per ounce and a weekly gain of +1.22% after the US Supreme Court affirmed a lower court’s ruling that President Trump’s use of the 1977 law exceeded presidential authority. This raised concerns about the ability of the US to fund its debt.

Silver also advanced, with spot silver up +7.67% to $82.92 an ounce and a cumulative weekly increase of +9.26%.

In the oil markets, Brent crude prices reversed earlier losses due to late-day short-covering. Brent crude futures closed at $71.64 per barrel, reflecting a decline of 30 cents, or -0.42%. US WTI crude settled at $66.31 per barrel, down 47 cents, or -0.70%.

Despite the day’s declines, both major crude benchmarks posted gains for the week. Brent crude increased by +5.93% and WTI advanced +5.57%.

On the geopolitical front, Iran's foreign minister indicated on Friday that a draft counterproposal would be prepared within days following nuclear negotiations earlier in the week. Concurrently, the US President stated he was contemplating limited military strikes.

Note: As of 4 pm EST 20 February 2026

Currencies

EUR +0.07% to $1.1780

GBP +0.15% to $1.3482

Bitcoin +1.34% to $67,804.80

Ethereum +1.35% to $1,974.03

The US dollar experienced a modest decline in volatile trading on Friday, ending a four-session streak of gains. Early in the day, the dollar was initially stronger following the release of US economic data that revealed higher-than-expected inflation, although economic growth fell notably short of forecasts.

According to the Commerce Department, GDP expanded at an annualised rate of 1.4% in Q4, below the estimated 3% growth pace. Analysts attributed the lower figure in part to the effects of the government shutdown. The personal consumption expenditures (PCE) price index, excluding food and energy, rose by 0.4% in December, above the 0.3% estimate and following an unrevised 0.2% increase in November. Over the past 12 months, the index climbed 3.0%, outpacing the 2.8% rise seen in November.

The dollar index slipped by -0.05% to 97.79, while the euro gained +0.07% to $1.1780. Despite Friday's decline, the greenback was up +0.94% on the week, marking its strongest weekly performance since November. In contrast, the euro registered a weekly decrease of -0.73%.

The British pound advanced +0.15% to $1.3482, but recorded a weekly loss of -1.22%, its most significant decline since January 2025.

Against the Japanese yen, the dollar appreciated by +0.05% to ¥155.05 and rose +1.55% for the week, its largest weekly gain since October. Japanese data showed that the country's annual core consumer inflation reached 2.0% in January, marking the slowest increase in two years.

Fixed Income

US Bond +1.1 basis points to 4.091%

German 10-year -0.7 basis points to 2.740%

UK 10-year gilt -1.4 basis points to 4.356%

US Treasury yields advanced on Friday after the Supreme Court struck down President Donald Trump’s tariffs, which had been implemented under emergency law provisions. This decision introduced uncertainty regarding potential payments to trading partners and the outlook for future federal government revenues.

In response, the US President announced his intention to impose a 15% global tariff for 150 days as a temporary replacement for some of the emergency duties.

The Supreme Court, in a 6 - 3 decision authored by Chief Justice John Roberts, affirmed a lower court’s ruling that President Trump’s use of the 1977 law exceeded presidential authority.

Following the ruling, the yield on the US 10-year Treasury note rose by +1.1 bps to 4.091%, up from 4.080% on Thursday.

While the US administration has not provided tariff collection data since 14th December, economists at the Penn-Wharton Budget Model estimated on Friday that tariffs collected under the emergency economic powers act had collected $164.7 billion between January 2025 and January 2026.

Treasury market participants are closely watching whether the administration can match the current level of tariff revenues with alternative levies, as this will impact the US fiscal outlook.

US Treasury Secretary Scott Bessent indicated on Friday that the Treasury’s estimates suggest that shifting to alternative legal authorities for tariffs would result in ‘virtually unchanged’ tariff revenue for 2026.

The yield on the 2-year Treasury note, sensitive to Fed fund rate expectations, increased by +1.8 bps to 3.482%. The yield curve between the 2-year and 10-year notes narrowed by 2.5 bps over the week, standing at 60.9 bps compared to 63.4 bps the previous week.

Yields climbed further after economic data released earlier on Friday showed that underlying US inflation exceeded expectations in December, reinforcing the view that the Fed will likely keep interest rates unchanged for the coming months.

For the week, short-term yields rose more than long-term yields: the 2-year yield increased by +6.4 bps, the 10-year yield by +3.9 bps, and the 30-year yield by +3.0 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 55.5 bps of cuts in 2026, lower than the 63.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 4.0% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 9.2% a week ago.

Long-term eurozone government bond yields posted a second consecutive weekly decline on Friday, amid heightened speculation regarding the leadership of the ECB.

Eurozone bonds outperformed US Treasuries during Friday's session. German 10-year yields declined -1.9 bps over the past week, extending the prior week’s -8.4 bps decrease. This brings the total decline for February thus far to -10.7 bps, marking the largest monthly drop since April of the previous year.

The yield on the 10-year Bund fell -0.7 bps on the day to close at 2.740%, remaining above last week’s two-and-a-half-month low of 2.725%.

At the short end of the German curve, the 2-year yield edged down -0.1 bps on Friday but increased +1.8 bps over the week. In contrast, the 30-year yield declined -0.7 bps on the day, contributing to a weekly decrease of -3.1 bps.

ECB President Christine Lagarde addressed reports about her potential resignation, affirming to The Wall Street Journal on Thursday her intention to complete her eight-year term. Earlier in the week, the Financial Times had reported on the possibility of her stepping down, intensifying the competition to succeed her and introducing potential uncertainty for the ECB.

Yields on Italian BTPs and other eurozone bonds, including those of France and Spain, also hovered near multi-month lows, having outperformed Treasuries over the past week.

On Friday, the Italian 10-year yield declined -0.6 bps to 3.350%, after reaching 3.344%, its lowest level in four months. Over the week, Italian BTP 10-year yields fell -1.8 bps, while the spread versus Bunds widened slightly by +0.1 bps to 61.0 bps.

The French 10-year OAT yield dropped -1.0 bps to 3.311% on Friday, marking its lowest point in more than six months. For the week, the French 10-year OAT yield fell -3.8 bps, narrowing the spread with Bunds by 1.9 bps to 57.1 bps compared to the previous week.

Note: As of 5 pm EST 20 February 2026

Global Macro Updates

Supreme Court decision on Presidential tariff authority. The Supreme Court issued a 6 - 3 ruling against the Trump administration's invocation of emergency powers under the International Emergency Economic Powers Act (IEEPA) to impose tariffs. The majority opinion was opposed by Justices Thomas, Alito, and Kavanaugh, who dissented from the decision.

Chief Justice Roberts explained that the president's interpretation of the statute hinged on isolated references to ‘regulate’ and ‘importation’ within the law's text. He emphasised that these terms alone cannot justify such an expansive reading of presidential authority. The Court concluded that granting unlimited tariff powers to the executive branch would constitute a transformative expansion of presidential authority.

While the ruling did not resolve the question of potential refunds for tariffs previously collected under IEEPA, Justice Kavanaugh, in his dissent, warned that the process of determining refunds is likely to become complicated and contentious. Economists from the Penn-Wharton Budget Model estimated that possible refunds could reach as much as $165 billion if enacted.

Administration officials have noted that the president retains other statutory authorities to impose tariffs, such as Section 122 and Section 301, though each comes with its own set of limitations.

The decision is expected to have broader implications. The weakening of the long end of the Treasury yield curve reflects market anticipation that incoming tariff revenues could have mitigated future budget deficits and curtailed government bond issuance. Additionally, this ruling may carry political consequences in the lead-up to the midterm elections, particularly in light of the administration's recent focus on affordability concerns.

Q4 GDP softer than anticipated; December PCE slightly exceeds expectations. The initial estimate for Q4 GDP reflects a 1.4% annualised growth rate, falling short of the consensus forecast of 1.9% and lower than Q3’s 4.4% pace. On a full-year basis, GDP grew by 2.2%, slightly above the consensus expectation of 2.0% but just below the previous year's figure of 2.3%.

The increase in Q4 GDP was primarily driven by rises in consumer spending and business investment. These advances were partially offset by a significant decline in government spending and a reduction in exports, with federal government spending contracting at a 5.1% rate—the steepest drop since 2020.

The GDP chain price index increased by 3.6%, surpassing the consensus estimate of 3.0%, though slightly below the prior reading of 3.8%. Personal consumption advanced by 2.2%, compared to a 2.6% rise in Q3.

For December, the headline Personal Consumption Expenditures (PCE) price index rose 0.4% m/o/m, exceeding the consensus estimate of 0.3% and accelerating from November's 0.2%. Core PCE also climbed 0.4% m/o/m, matching expectations and doubling the previous month's pace.

On an annualiszed basis, the headline PCE price index rose 2.9%, edging above the consensus forecast of 2.8% and the prior month's rate of 2.8%. Core PCE increased to 3.0% y/o/y, in line with expectations and up from 2.8%, marking its highest level since March 2024.

Service prices remained the principal factor behind overall inflation, though goods prices also accelerated in December, with some analysts attributing this uptick to the impact of tariffs.

Personal spending in the US increased by 0.4% in December, consistent with both market expectations and the prior month's reading. Personal income advanced 0.3% m/o/m, in line with forecasts but slightly below November's 0.4% growth.

Softer GDP readout, coupled with hotter PCE, did little to change Fed rate cut expectations with market still pricing first cut in June.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.