Peace for two weeks as negotiations continue

Key data to move markets today

EU: German Factory Orders, Eurozone PPI and Eurozone Retail Sales

US: FOMC Minutes and speeches by San Francisco Fed President Mary Daly and Fed Governor Christopher Waller

Global Macro Updates

Ceasefire at the Strait: a fragile path to peace and oil recovery. On Truth Social, the US President announced that he had accepted Pakistan’s proposal to suspend US military action against Iran for two weeks, contingent upon Iran’s immediate reopening of the Strait of Hormuz. President Trump emphasised that US military objectives had already been achieved and reaffirmed that negotiations for a long-term peace plan were ‘very far along’. He also acknowledged Iran’s 10-point proposal as a viable foundation for future discussions.

Press reports indicate that both Iran and Israel have agreed to participate in negotiations, with Iranian media confirming that the first round of talks is scheduled to begin on Friday in Islamabad.

Iran’s Foreign Minister Araghchi confirmed Iran’s acceptance of the arrangement and stated that safe passage through the Strait of Hormuz would be permitted for two weeks, coordinated by Iran’s armed forces.

The Supreme National Security Council of Iran claimed that major concessions had been secured from the US, including a principled agreement to lift all primary and secondary sanctions, acceptance of Iran’s nuclear enrichment activities and continued Iranian control over the Strait of Hormuz. However, BBC coverage clarified that nuclear enrichment was not explicitly included in the 10-point plan. The plan did call for the lifting of sanctions and addressed US concerns by committing to reopening the Strait and pledging not to seek possession of nuclear weapons.

Axios reported that the process of restoring oil shipments through the Strait of Hormuz is expected to be lengthy and complex, leading to persistently high prices and supply shortages for importing nations. The key factor will be whether the US-Iran ceasefire provides sufficient certainty for tanker operators to resume shipments.

The restoration of insurance for tankers remains uncertain and it is unclear what specific conditions Iran may impose. Restarting oil facilities and shut-in fields could take weeks to months, while repairing damaged infrastructure may require up to six months to return to pre-war production rates; in the case of Qatar’s LNG exports, full recovery could take years.

Prior to the ceasefire, the US Energy Information Administration (EIA) warned that fuel prices could continue to rise for months after the Strait’s reopening and revised its Brent spot price forecast upward to an average of $96 per barrel for this year, from $78.84. Retail gasoline and diesel prices are also expected to climb. The EIA predicts that full restoration of oil flows through the Strait will take several months post-conflict.

Reuters has revealed that refiners in Europe and Asia are paying nearly $150 per barrel for certain types of crude oil, which is much higher than prices seen in the futures market. Previously, Reuters reported that spot premiums for WTI compared to other crude benchmarks hit record levels because of the fierce competition between Asian and European refiners. Furthermore, WTI crude futures entered an extreme backwardation phase, indicating a substantial premium for immediate delivery.

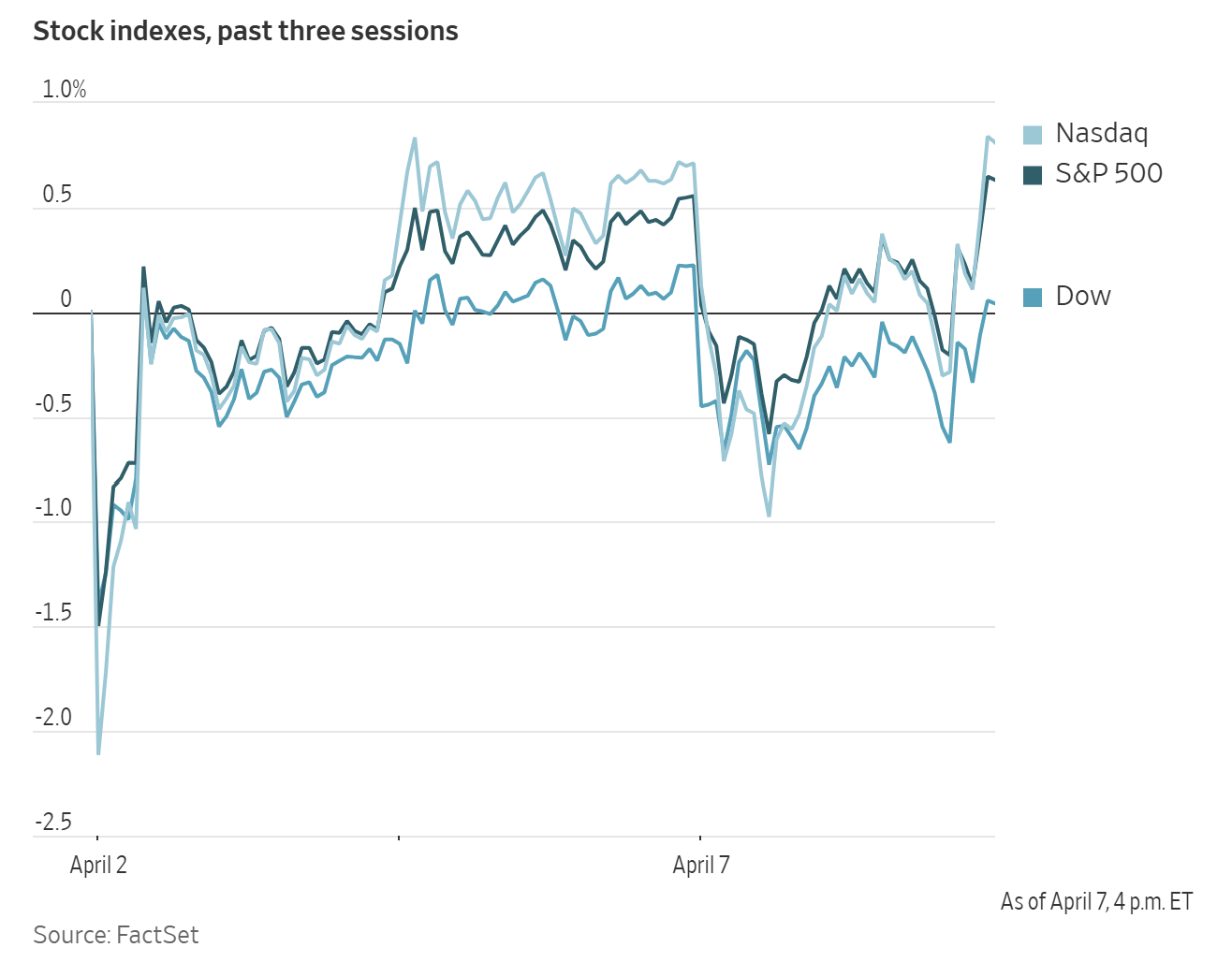

US Stock Indices

Dow Jones Industrial Average -0.18%

Nasdaq 100 +0.04%

S&P 500 +0.08%, with 6 of the 11 sectors of the S&P 500 up

Late in a volatile session, Wall Street found some relief as Pakistan asked the US to extend Tehran's Strait of Hormuz reopening deadline by two weeks. The S&P 500 edged up +0.08%, the Nasdaq Composite gained +0.10% and the Dow Jones Industrial Average dropped -0.18%.

In corporate news, Intel has announced its participation in Elon Musk’s ambitious initiative to design semiconductors for Tesla, SpaceX and xAI, signifying an unexpected turn in the chipmaker’s ongoing efforts to regain market leadership.

Pacific Investment Management is reportedly in discussions with Bank of America to facilitate approximately $14 billion in debt financing for the construction of a significant Oracle data centre in Michigan, according to sources familiar with the negotiations.

Anthropic PBC disclosed that its revenue run rate has surpassed $30 billion, a substantial increase from $9 billion at the close of 2025, and confirmed plans to collaborate with Broadcom and Google to support its expanding operations.

Pershing Square, led by Bill Ackman, has submitted an offer to acquire Universal Music Group, valuing the world’s largest music company at approximately $60 billion.

Shares of leading insurance companies rose after the US Medicare programme announced a 2.48% payment increase to private insurers for 2027, representing a notable improvement over the initial rates proposed earlier this year.

S&P 500 Best performing sector

Communication Services +1.04%, with Paramount Skydance +10.66%, Alphabet +2.11% and Charter Communications +1.74%

S&P 500 Worst performing sector

Consumer Staples -1.76%, with Campbell’s -5.18%, Dollar Tree -4.20% and Kimberly-Clark -4.06%

Mega Caps

Alphabet +2.11%, Amazon +0.46%, Apple -2.07%, Meta Platforms +0.35%, Microsoft -0.16%, Nvidia +0.26% and Tesla -1.75%

Information Technology

Best performer: Broadcom +6.21%

Worst performer: Enphase Energy -4.76%

Materials and Mining

Best performer: FMC +2.50%

Worst performer: International Flavors & Fragrance -2.58%

European Stock Indices

CAC 40 -0.67%

DAX -1.06%

FTSE 100 -0.84%

Commodities

Gold spot +1.84% to $4,733.00 an ounce

Silver spot +0.19% to $72.93 an ounce

West Texas Intermediate -2.02% to $110.34 a barrel

Brent crude -3.87% to $105.44 a barrel

Gold prices recovered on Tuesday as market participants remained focussed on the impending 8:00 PM Eastern deadline set by President Trump, which required Iran to reach an agreement or face extensive attacks targeting its bridges and power infrastructure.

Spot gold advanced +1.84% to $4,733.00 per ounce, recovering from a -0.60% decline on Monday.

Despite a strong start earlier in the year, gold has declined by -10.64% since the onset of the Iran war on 28 February.

Spot silver increased +0.19%, reaching $72.93 per ounce.

WTI and Brent crude prices declined -2.02% and -3.87%, respectively, in anticipation of President Trump’s 8:00 PM Eastern deadline regarding the reopening of the Strait of Hormuz. Early session reports indicated that Iran had suspended negotiations with the US, although subsequent updates suggested that discussions remained ongoing.

Both benchmark contracts retreated from their session highs following President Trump’s interview on Fox News, during which he stated that, given progress in the negotiations, he may consider extending the deadline before escalating attacks on Iranian infrastructure. In response to heightened tensions, Kuwait advised residents to remain indoors from midnight until 6:00 AM local time as a precaution.

China and Russia vetoed a UN Security Council resolution aimed at protecting shipping in the Strait of Hormuz. Shortly after 2:00 PM Eastern, media outlets reported that Iran had informed mediators it retains approximately 15,000 missiles and 45,000 drones.

Following the close, Tasnim News cited military sources who warned that Iran may target Aramco oil facilities, the Yanbu export terminal and the Fujairah pipeline should President Trump proceed with his threat. Additionally, Pakistan requested a two-week extension of the deadline and urged Iran to reopen the Strait of Hormuz during that period as a goodwill gesture.

Overnight, Ukraine launched another attack on Russia’s Ust-Luga oil export terminal, striking three reservoir tanks. Bloomberg news reported that Russian Urals crude traded at a 13-year high above $116 per barrel last week, while spot prices for Dated Brent reached a record $144.50 per barrel today.

The EIA Short Term Energy Outlook reduced its forecast for global crude and liquids production in 2026 by 2.7 million barrels per day (bpd) m/o/m, and raised its price projections for WTI and Brent this year by 18.7% and 21.8%, respectively. The agency estimated that over 9.3 million bpd of global supply were offline in March, compared to 2.42 million bpd in February, and also lowered its US crude production estimate for 2026 by 100,000 bpd.

Oil shipments through the CPC remain stable, according to Kazakhstan’s energy ministry as of Tuesday, following allegations by Russia’s military that Ukrainian attacks damaged loading facilities in the Black Sea. Historically, Kazakhstan has delayed acknowledging production impacts resulting from such incidents.

Note: As of 4 pm EDT 7 April 2026

Currencies

EUR +0.46% to $1.1596

GBP +0.48% to $1.3298

Bitcoin +0.57% to $69,909.56

Ethereum +0.26% to $2,144.70

The US dollar edged lower as market participants closely monitored the impending US deadline for Iran to reopen the Strait of Hormuz to maritime traffic or face potential strikes on its infrastructure. The US dollar index declined -0.46% to 99.52.

The Japanese yen experienced a modest appreciation, strengthening +0.06% against the dollar to ¥159.50 per dollar. The euro advanced +0.46% to $1.1596, and the British pound rose +0.48% to $1.3298. Additionally, the pound gained +0.10% against the euro, reaching 87.14 pence on Tuesday.

Fixed Income

US 10-year Bond -4.4 basis points to 4.300%

German 10-year Bund +9.1 basis points to 3.086%

UK 10-year gilt +6.1 basis points to 4.839%

US Treasury yields remained relatively steady amid volatile trading conditions on Tuesday, as the deadline imposed by the US President for Iran to reopen the Strait of Hormuz approached, with little indication that an agreement would be reached.

The yield on the US 10-year Treasury decreased -4.4 bps to 4.300%, after previously reaching an intraday high of 4.380%. Similarly, the yield on the 30-year Treasury bond declined -1.6 bps, settling at 4.874%. The two-year US Treasury yield, responsive to the Fed fund rate expectations, fell -6.6 bps to 3.798%, after rising as high as 3.877% earlier in the session.

The US Treasury yield curve, which tracks the spread between the two-year and 10-year notes, stood at 50.2 bps.

Yields moved lower following a well-received auction of $58 billion in three-year notes, with analysts noting a bid-to-cover ratio of 2.68x, which was above average.

This week, the market will see further supply with $39 billion in 10-year notes scheduled for auction on Wednesday, followed by $22 billion in 30-year bonds on Thursday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 7.8 bps of rate cuts in 2026, in contrast with the 6.1 bps of rate hikes priced in a week ago. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 1.0% probability.

Eurozone bond yields climbed on Tuesday, driven by ongoing uncertainty regarding the Iran conflict and the impending US-imposed deadline for reaching an agreement.

The yield on the German 10-year Bund was up +9.1 bps at 3.086%.

Belgian central bank president Pierre Wunsch told The Wall Street Journal on Tuesday that the ECB may need to increase interest rates if the conflict continues, and a rate hike as soon as 30 April remains a possibility.

In late afternoon trading on Tuesday, markets were pricing in 76.5 bps of ECB interest rate hikes by year-end, consistent with pre-long weekend expectations. There is a 66.0% probability priced in for a 25 bps increase to 2.25% at the 29 April meeting.

The German 2-year yield, sensitive to changes in rate expectations, was +10.6 bps at 2.722% on Tuesday. On the longer end of the curve, the 30-year yield rose +6.4 bps to 3.538%.

The yield on Italian 10-year BTP increased +11.3 bps to 3.988%, resulting in a premium of 90.2 bps over Bunds.

Note: As of 4 pm EDT 7 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.