Will the cease-fire really calm the waters?

Global Macro Updates

Strait of Hormuz reopens on fragile terms. Ahead of Tuesday's 8:00 pm ET deadline, the US President announced that Washington and Tehran had agreed to a two-week ceasefire, with the reopening of the Strait of Hormuz as a central condition. Iran consented to allow ‘safe passage’ through the waterway, though only in coordination with its navy and, notably, ‘with due consideration of technical limitations.’ Analysts have interpreted this language as preserving Tehran's effective discretion to accelerate or restrict vessel movement at will, contingent on the trajectory of peace negotiations with the US and Israel.

The operational reality on the water reflects that ambiguity. Only four ships transited the strait on Wednesday, the lowest daily figure recorded in April and a sharp decline from more than 100 per day prior to the conflict, according to S&P Global Market Intelligence. Iran has informed mediators it will cap crossings at roughly a dozen vessels per day, and the Islamic Revolutionary Guard Corps Navy has warned ships anchored near the strait that they must obtain Tehran's authorisation before attempting transit or risk destruction. Iran has also indicated its intention to charge vessels upward of $1 million per crossing going forward.

The bottleneck remains considerable: more than 425 oil and fuel tankers and nearly 20 LNG carriers are awaiting passage. Brokers expect dozens of vessels to move through in the coming days — if the ceasefire holds. Complicating Iran's jurisdictional claims, however, is a basic geographic reality: Iran controls only one shore of the strait. Oman's Musandam exclave occupies the opposite bank, and maritime legal experts have noted there is no recognised basis under international law for Iran to regulate commercial shipping on Oman's side of the maritime boundary.

Diplomatically, a follow-on meeting between US and Iranian delegations, with Vice President JD Vance leading the American side, is scheduled for Saturday in Islamabad. Pakistan, Egypt and Turkey have served as mediators. President Trump has indicated that a 10-point Iranian framework will form the basis for discussions, though he has also asserted that Tehran has already accepted many elements of a separate 15-point US proposal calling for sweeping concessions. Iran's publicised demands, including retention of Hormuz control, uranium enrichment rights, sanctions relief and full US military withdrawal from the region, have been characterised as nonstarters by Washington and Jerusalem. Iran, in turn, has rejected the US plan's requirements to abandon enrichment and accept constraints on its missile programme.

Even in a best-case scenario, market normalisation will lag. The EIA's Short-Term Energy Outlook, published Tuesday ahead of the ceasefire announcement, estimated that Middle Eastern supply disruptions have already removed approximately 7.5 million barrels per day (bpd) from global markets, with outages projected to rise above 9.1 million bpd through April. Should the conflict conclude this month, the EIA projects shut-ins could decline to 6.7 million bpd in May, with output approaching pre-conflict levels by late 2026. Refined products, particularly jet fuel, are expected to normalise more slowly, with supply constraints persisting for several months even if the strait fully reopens.

The geopolitical consequences of a Tehran-controlled chokepoint extend well beyond energy logistics. For US allies in the region, including Saudi Arabia, the UAE and Kuwait, Iran's de facto gatekeeping authority over the strait represents a structural vulnerability: the continued flow of their hydrocarbon exports now rests, in part, on Tehran's goodwill. That leverage is unlikely to dissipate even under a formal peace settlement, and will almost certainly inform the posture of Gulf states throughout the negotiation period.

China, despite reportedly playing a constructive role in nudging Tehran toward the negotiating table, finds itself in an increasingly uncomfortable position. Hours after the ceasefire announcement, President Trump declared that any country supplying military weapons to Iran would face immediate 50% tariffs on all goods sold to the US, with no exemptions. Though no nations were named explicitly, the measure is widely understood as directed at Beijing and Moscow, both of which have supplied Iran with missile systems, air-defense technology and dual-use components. Analysts noted the threat carries particular tension ahead of Trump's planned summit with President Xi in Beijing next month.

Adding a further layer of complexity, the temporary OFAC general licences authorising the sale and delivery of sanctioned Russian and Iranian crude oil, issued in March to stabilise energy markets, are approaching expiration: the Russian oil waiver (GL 134A) expires 11 April, and its Iranian counterpart (GL U) on 19 April. Whether these are renewed, allowed to lapse, or leveraged as diplomatic instruments will be a key signal of Washington's intentions as the two-week ceasefire clock runs down.

Corporate Earnings Calendar

Monday: Goldman Sachs

Tuesday: BlackRock, Citigroup, Johnson & Johnson, JPMorgan Chase, Wells Fargo

Wednesday: Bank of America, Morgan Stanley

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +4.90% MTD and -1.37% YTD

Dow Jones Industrial Average +0.52% MTD and -3.08% YTD

NYSE +3.21% MTD and +3.61% YTD

S&P 500 +3.90% MTD and -0.92% YTD

The S&P 500 is +3.04% over the past seven days, with 10 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +2.52% over this past week and +3.35% YTD.

The S&P 500 Communication Services is the leading sector so far this month, +6.71% MTD and -0.87% YTD, while Energy is the weakest sector at -5.53% MTD and +29.65% YTD.

Over the past seven days, Communication Services outperformed within the S&P 500 at +5.12%, followed by Industrials and Information Technology at +4.05% and +3.63%, respectively. Conversely, Energy underperformed at -2.16%, followed by Utilities and Consumer Staples at +0.85% and +1.04%, respectively.

The equal-weight version of the S&P 500 was +2.36% on Wednesday, underperforming its cap-weighted counterpart by 0.15 percentage points.

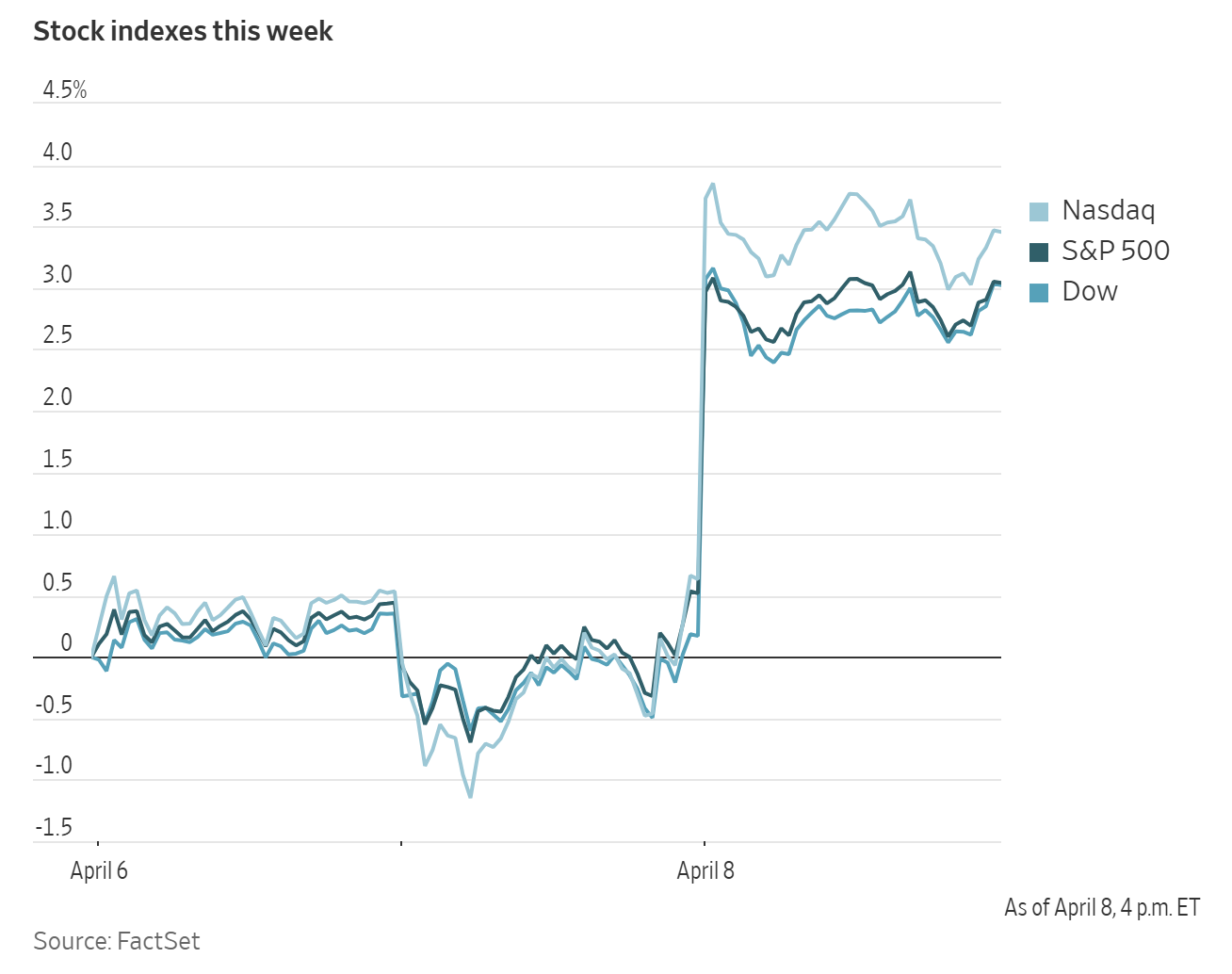

On Wednesday, the Dow Jones Industrial Average advanced +2.85% to close at 47,909.92, 1,325.46 points higher than Tuesday’s close. The S&P 500 rose by +2.51%, while the Nasdaq Composite posted a gain of +2.80%. Over the past seven days, the S&P 500 is +3.16%, the Dow Jones +0.04%, and the Nasdaq Composite +3.64%.

In corporate news, Levi Strauss announced that its turnaround strategy is yielding positive results and accordingly raised its guidance.

Moody’s downgraded the outlook for Blue Owl Credit Income, one of Blue Owl’s largest private credit funds, following substantial investor redemption requests amounting to 22% of assets at the close of the first quarter. Despite this, the fund limited withdrawals to 5%. The outlook revision does not immediately impact the fund’s Baa2 investment-grade rating, but it moves Blue Owl closer to the lowest tier before non-investment grade, Baa3.

Shell issued a warning regarding decreased natural gas production due to disruptions stemming from the conflict in the Middle East, although it anticipates benefitting from elevated oil prices. The company's shares declined alongside the broader energy sector after the announcement of a cease-fire prompted a sharp drop in oil prices.

Delta Air Lines forecasted that higher fuel costs resulting from the Iran conflict will exceed $2 billion through June, leading the airline to maintain its previously issued full-year profit guidance and proceed with caution.

Mega caps: The Magnificent Seven had a mostly positive performance over the past week. Over the last seven days, Alphabet +6.70%, Meta Platforms +5.73%, Amazon +5.07%, Nvidia +3.60%, Microsoft +1.34% and Apple +1.28%, while Tesla -9.97%.

Energy stocks had a mostly negative performance this week. The Energy sector itself was -1.71%. WTI and Brent prices are -2.44% and -4.12%, respectively, over the past week. Over the last seven days, Baker Hughes +4.67% and Energy Fuels +1.92%, while Halliburton -0.53%, Shell -1.23%, Chevron -2.29%, BP -2.31%, ConocoPhillips -2.46%, Marathon Petroleum -2.59%, ExxonMobil -2.84%, Occidental Petroleum -3.95%, Phillips 66 -4.35% and APA -6.29%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector itself +2.74%. Over the past seven days, Freeport-McMoRan +6.37%, Nucor +4.86%, Newmont Corporation +3.83%, Sibanye Stillwater +1.69%, Celanese Corporation +0.31% and Mosaic +0.30%, while Albemarle -0.58%, CF Industries -1.42% and Yara International -4.28%.

European Stock Indices Price Performance

Stoxx 600 +5.21% MTD and +3.60% YTD

DAX +6.18% MTD and -1.67% YTD

CAC 40 +5.72% MTD and +1.40% YTD

IBEX 35 +6.35% MTD and +4.76% YTD

FTSE MIB +6.28% MTD and +4.78% YTD

FTSE 100 +4.25% MTD and +6.82% YTD

This week, the pan-European Stoxx Europe 600 index is +2.65%. It was +3.88% on Wednesday, closing at 613.50.

So far this month in the STOXX Europe 600, Banks is the leading sector +9.04% MTD and +1.29% YTD, while Oil & Gas is the weakest at -2.33% MTD and +32.74% YTD.

Over the past seven days, Travel & Leisure outperformed within the STOXX Europe 600, at +5.07%, followed by Banks and Industrial Goods at +4.33% and +4.20%, respectively. Conversely, Oil & Gas underperformed at +0.13%, followed by Health Care and Utilities at +0.30% and +1.64%, respectively.

Germany's DAX index was +5.06% Wednesday, closing at 24,080.63. It was +3.36% over the past seven days. France's CAC 40 index was +4.49% Wednesday, closing at 8,263.87. It was +3.54% over the past week.

The UK's FTSE 100 index was +2.36% over the past seven days to 10,608.88. It was +2.51% on Wednesday.

The Travel & Leisure outperformed on Wednesday, with airline stocks surging as a significant drop in fuel costs, following the session’s crude price slump after the US-Iran ceasefire agreement, was expected to materially enhance near-term profit margins, according to analysts. The sector, which had been heavily de-rated during the recent oil price spike, benefitted from improved positioning and short covering, amplifying the rebound. The Technology sector also advanced, particularly among semis, with analysts citing lower energy costs and stabilising macroeconomic conditions as factors improving sentiment toward CapEx and demand visibility.

Banks and Financials broadly benefitted from reduced market volatility and improved growth outlooks, while rate hike expectations provided additional support. Commerzbank shares climbed after the bank rejected UniCredit's takeover proposal, underscoring ongoing M&A activity and robust capital positions within the sector. Close Brothers Group shares also traded higher, following its clarification of financial provisions for its motor finance scheme. Construction & Materials and Basic Resources both advanced due to anticipated cost relief as commodity prices increased in response to the announcement of the US-Iran ceasefire.

Conversely, Oil & Gas was the clear underperformer, as the sharp decline in crude prices reversed outperformance of the past week. Leading majors were among the notable decliners, with Shell's reduction in gas output, attributed to the conflict in the Middle East, further weighing on investor sentiment despite expectations of trading gains. Defensive sectors, including Utilities, Telecom, Insurance and Health Care, lagged relative to the broader market rally, as investors shifted from defensive holdings to more pro-cyclical sectors.

Other Global Stock Indices Price Performance

MSCI World Index +4.07% MTD and +0.63% YTD

Hang Seng +4.46% MTD and +1.02% YTD

Over the past seven days, the MSCI World Index and Hang Seng Index are +3.16% and +2.37%, respectively.

Currencies

EUR +0.95% MTD and -0.68% YTD to $1.1665

GBP +1.35% MTD and -0.54% YTD to $1.3400

On Wednesday, the US dollar declined to its lowest point in a month against major currencies, following an agreement between the US and Iran for a two-week ceasefire. This development fostered optimism among investors and boosted risk assets globally.

However, the ceasefire appeared precarious. The dollar recovered from its earlier losses as Iran targeted oil facilities in neighbouring Gulf countries and Israel launched its most significant attacks to date on Lebanon.

The euro appreciated +0.60% on Wednesday to $1.1665, reaching its highest level since early March. Over the past seven days, the dollar retreated -0.67% against the euro.

Broadly, the US dollar posted declines across the board. The dollar index fell -0.52% to 99.00 on Wednesday, marking a weekly decrease of -0.57%. MTD the index is down -0.87%, although it remains up +0.74% YTD.

The Japanese yen strengthened by +0.63% against the US dollar on Wednesday to ¥158.50, contributing to a +0.13% gain over the past week. MTD, the yen is up +0.11%, though it is down -1.18% YTD.

The British pound rose +0.77% to $1.3400 on Wednesday. Over the past week, sterling has appreciated by +0.73% against the US dollar.

Among global currencies, the US dollar has been the principal beneficiary of the ongoing conflict with Iran, partly due to the US being a net energy exporter and the terms of trade of most commodities. This status provides a strategic advantage, as the US is less vulnerable to the economic challenges faced by oil-importing nations such as Japan and many European countries.

The five-week conflict significantly undermined investor confidence, resulting in an unprecedented disruption to global oil and gas supplies. The fragile détente has granted Iran greater influence over shipping through the crucial strait than it possessed prior to the conflict, according to analysts. This shift occurred after the US President refrained from escalating attacks on Iran’s civilian infrastructure.

Note: As of 5:00 pm EDT 8 April 2026

Cryptocurrencies

Bitcoin +4.88% MTD and -18.41% YTD to $71,551.24

Ethereum +5.42% MTD and -25.65% YTD to $2,214.67

Bitcoin was +4.61% over the last seven days and Ethereum was +2.68%. On Wednesday, global markets turned more optimistic after a ceasefire deal between the US and Iran. Bitcoin climbed as much as 5% to $72,841, its highest level since 18 March, before paring some of the gain to end the trading day +2.35% to $71,551.24. Bitcoin has been stuck in a range between roughly $60,000 and $75,000 since the war with Iran started on 28 February. It remains down more than 40% from its October record above $126,000. Ethereum, which had risen as much as +7.5% to $2,273 during the day, ended Wednesday’s session +3.26% to $2,214.67.

As noted by Bloomberg news, spot activity remains soft, according to a report from blockchain data firm Glassnode, which added that “until spot demand picks up, rallies are likely to feel fragile, with limited follow-through.” However, demand by institutional investors is still relatively solid with listed Spot Bitcoin funds bringing in about $471 million in net inflows on Monday, the strongest single-day total in roughly six weeks, according to The Block's data.

In addition, Morgan Stanley launched the Morgan Stanley Bitcoin Trust on Wednesday. The launch is one of the first entries by a major US commercial bank into issuing a Bitcoin-linked exchange traded product. It saw about $34 million in trading volume in its first day of trading. Bitcoin ETFs currently hold over $100 billion in cumulative assets under management as of Tuesday, according to data from CoinShares. The largest Bitcoin ETF belongs to BlackRock, which has over $53 billion in net assets in its IBIT fund. However, flows into Spot ETFs remain in recovery mode. Nearly $5 billion has exited since November, only partially offset by $1.32 billion in March inflows and another roughly $150 million so far in April.

Note: As of 5:00 pm EDT 8 April 2026

Fixed Income

US 10-year yield -1.7 bps MTD and +6.3 bps YTD to 4.301%

German 10-year yield -5.5 bps MTD and +10.4 bps YTD to 2.951%

UK 10-year yield -20.5 bps MTD and +12.1 bps YTD to 4.651%

US Treasury yields remained largely stable on Wednesday. The yield on the 10-year US Treasury note edged +0.1 bps higher to 4.301%, while the yield on the 30-year bond increased +1.4 bps to 4.888%. The two-year US Treasury yield, which often moves in tandem with Fed fund rate expectations, rose +0.2 bps to 3.800%. The yield curve, as measured by the spread between the two- and 10-year Treasury notes, stood at 50.1 bps, slightly lower than the previous week’s 50.7 bps.

Over the past week, US yields declined across the curve. At the front-end, the 2-year yield declined by -1.5 bps, the 10-year yield ended the week -2.1 bps lower, and at the longer end, the 30-year yield fell by -1.4 bps.

Following a robust $58 billion auction of 3-year notes on Tuesday, analysts characterised the $39 billion auction in 10-year notes as decent, with a bid-to-cover ratio of 2.43x, slightly below the average.

This week’s auction schedule will end today with the issuance of $22 billion in 30-year bonds.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 0.5% probability of a 25 bps rate hike at April’s FOMC meeting, from 1.0% last week. Fed funds futures traders are pricing in 6.4 bps of rate cuts in 2026, lower than the 7.0 bps of rate cuts priced in a week ago.

March FOMC minutes note worries that inflation may persist due to the oil shock. The March FOMC minutes indicate that committee members expressed concern that inflation may persist at elevated levels for an extended period, largely as a result of the recent oil price shock. The meeting itself produced no major surprises, as rates were kept unchanged in line with expectations. Governor Miran dissented, advocating for a 25 bps reduction. The overall takeaways leaned in a hawkish direction, with fewer members forecasting more than one rate cut in 2026. Chairman Powell emphasised that additional rate cuts are unlikely without further evidence of progress on underlying inflation.

Regarding inflation and oil prices, many participants highlighted the risks associated with prolonged high inflation. Some noted that there had been little progress in reducing inflation in recent months, while several participants observed that near-term inflation expectations have increased, driven by the oil shock.

On the labour market front, most committee members believed that recent data pointed to a broadly balanced labour market. However, the vast majority judged that employment risks are tilted to the downside. Some members raised concerns about potential shocks to the labour market and suggested that firms may delay or scale back hiring in anticipation of the adoption of AI technologies.

With respect to the outlook for economic growth, participants reported continued solid activity and noted that consumer spending has remained resilient. Most expect the trajectory of growth to be sustained by investments related to AI, favourable financial conditions and supportive fiscal policy measures.

In terms of monetary policy, many participants agreed that it would likely become appropriate to reduce interest rates over time. Nonetheless, a few committee members have postponed their assumptions regarding the timing of such adjustments further into the future.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt declined -18.8 bps to 4.651%. Over the past seven days, it is -12.4 bps lower.

Following the agreement for a two week ceasefire in the Iran conflict, traders reduced expectations for future ECB rate hikes. Nevertheless, two tightening actions were still anticipated by year-end, reflecting ongoing uncertainty regarding the prospect of a permanent resolution.

Money markets reflected a roughly 30% probability of an ECB rate hike in April, down from 60% the previous day, and forecasted a deposit facility rate near 2.50% by year-end, rather than 2.75%. Traders fully priced in one increase by June and two by September. The current deposit rate stands at 2.0%.

Germany’s 10-year government bond yield declined -13.5 bps to 2.951%. The 2-year yield, more responsive to policy rate expectations, fell -21.9 bps to 2.503%. At the longer end, the 30-year yield decreased -7.1 bps to 3.467%.

Italy’s 10-year BTP yield dropped -27.9 bps on Wednesday to 3.709%, with the spread over safe-haven Bunds narrowing to 75.8 bps from 87.5 bps the previous week. The Italian 10-year yield declined -15.4 bps throughout the week.

During the past week, yields across the German government bond curve decreased, with the most pronounced decline observed at the short end. The yield on the 10-year German bond fell -3.7 bps, while the two-year Schatz yield was -10.2 bps. At the longer end of the spectrum, the 30-year German yield experienced a modest increase of +0.8 bps.

The yield spread between German Bunds and 10-year UK gilts reached 170.0 bps on Wednesday, a decline of 8.7 bps over the past seven days.

The spread between US 10-year Treasuries and German Bunds is now 135.0 bps, an increase of 1.6 bps from last week’s 133.4 bps.

Over the course of the week, France’s 10-year OAT yield has decreased -11.5 bps. The spread between the French OAT 10-year yield and German Bund 10-year yield stood at 62.6 bps, 7.8 bps lower than last week’s 70.4 bps.

Commodities

Gold spot +0.97% MTD and +9.99% YTD to $4,745.00 per ounce

Silver spot -1.31% MTD and +1.63% YTD to $74.12 per ounce

West Texas Intermediate crude -4.98% MTD and +68.09% YTD to $96.50 a barrel

Brent crude -18.71% MTD and +57.91% YTD to $96.18 a barrel

On Wednesday, gold reached its highest level in nearly three weeks, supported by declines in both the US dollar and oil prices following the agreement between Washington and Tehran to enact a two-week truce in their ongoing conflict.

Spot gold increased +0.25% to $4,745.00 per ounce, with bullion earlier rising more than three percent to its strongest level since 19 March. Despite this, gold prices have decreased -0.26% over the past seven days.

The depreciation of the US dollar against major currencies made dollar-denominated bullion more accessible to holders of other currencies, thereby supporting gold prices.

Spot silver advanced +1.63% to $74.12 per ounce. Over the past week, however, silver has declined -1.33%.

On Wednesday, oil prices experienced a sharp decline, falling below $100 per barrel amid optimism about the potential reopening of the Strait of Hormuz. This sentiment was fuelled by the US President's agreement to a two-week ceasefire with Iran.

Brent crude futures closed $9.26, or -8.78%, lower at $96.18 per barrel, while US WTI crude dropped $13.84, or -12.54%, to $96.50 per barrel. Over the past week, WTI is down -2.44% and Brent has declined by -4.12%.

The initial drop in prices reflected market anticipation of the Strait's reopening and the release of built-up energy supplies through this critical shipping route. However, oil clawed back some losses as Iranian strikes on regional energy infrastructure persisted. Despite the ceasefire agreement, tanker traffic through the Strait of Hormuz remains virtually halted. Iran has indicated to mediators that it will only participate in planned talks in Islamabad if the ceasefire is extended to include ongoing Israeli military actions against Lebanon. The resumption of tanker movement is further delayed by shipowners seeking clarity on Iran's requirements, verification of insurance coverage and official statements from Tehran throughout the day.

Shortly before the close of trading, Iran's parliament speaker stated that negotiations are unreasonable given the current situation in Lebanon. In response, the White House Press Secretary clarified that Lebanon is not included in the ceasefire agreement with Iran. Israeli Prime Minister Netanyahu also affirmed that the ceasefire does not apply to Hezbollah and Israeli operations against them will continue.

The region remains extremely volatile, with Iranian drones targeting a pumping station on Saudi Arabia's East-West pipeline. Additionally, Qatar, Bahrain, the United Arab Emirates and Kuwait all faced missile and drone attacks throughout the day.

Additionally, Russian oil exports from Ust-Luga have been offline since 1 April due to repeated drone strikes by Ukraine.

EIA report. The latest US Energy Information Agency (EIA) report, released on Wednesday showed that US crude oil inventories reached their highest level in nearly three years last week, while fuel inventories declined as international demand increased.

Crude inventories rose by 3.1 million barrels to a total of 464.7 million barrels for the week ending 3 April. Stocks in the Strategic Petroleum Reserve decreased by 1.7 million barrels, bringing the reserve down to 413.3 million barrels.

In March, the US announced plans to release 172 million barrels of oil from its reserve over a 120-day period in an effort to mitigate surging oil prices caused by the US-Israeli conflict with Iran.

Crude stocks at the Cushing, Oklahoma delivery hub increased by 24,000 barrels during the week, marking their highest level since July 2024. On the US Gulf Coast, crude inventories were at their highest point since March 2023.

Distillate stockpiles, including diesel and heating oil, declined by 3.1 million barrels to 114.7 million barrels for the week, according to EIA data. Distillate exports rose last week by 170,000 barrels per day (bpd), reaching 1.58 million bpd compared to 1.23 million bpd a year earlier.

Net US crude imports decreased by 758,000 bpd last week, while exports increased by 628,000 bpd, totalling 4.15 million bpd, as per EIA figures.

Refinery crude runs fell by 129,000 bpd, and utilisation rates decreased slightly by 0.1 percentage point to 92% for the week.

US gasoline inventories dropped by 1.6 million barrels, bringing the total to 239.3 million barrels for the week. Total product supplied, a proxy for overall demand, declined by 283,000 bpd to 20.64 million bpd.

Note: As of 5:00 pm EDT 8 April 2026

Key data to move markets

EUROPE

Thursday: German Industrial Production, German Trade Balance and a speech by Dutch central bank Governor Olaf Sleijpen

Friday: German Harmonised Index of Consumer Prices and a speech by ECB Vice President Luis de Guindos

Tuesday: Spanish Harmonised Index of Consumer Prices

Wednesday: French CPI and Eurozone Industrial Production

UK

Tuesday: BRC Like-for-Like Retail Sales and speeches by BoE Governor Andrew Bailey and BoE External Member Megan Greene

Wednesday: A speech by BoE Governor Andrew Bailey

USA

Thursday: Initial and Continuing Jobless Claims, GDP, Personal Consumption Expenditures Price Index, Core Personal Consumption Expenditures Price Index, Personal Income and Personal Spending

Friday: CPI, Factory Orders, Michigan Consumer Expectations Index, Michigan Consumer Sentiment Index and UoM 1-year and 5-year Consumer Inflation Expectations

Monday: Existing Home Sales Change

Tuesday: ADP Employment Change 4-week Average, PPI and a speech by Chicago Fed President Austan Goolsbee

Wednesday: NY Empire State Manufacturing Index and Fed’s Beige Book

CHINA

Friday: CPI and PPI

Tuesday: Exports, Imports and Trade Balance

GLOBAL: Monday to Saturday IMF and World Bank Spring Meeting

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.