Will financials kick-off earnings on a positive note?

What to look out for today

Companies reporting on Monday, 13 April: Goldman Sachs

Key data to move markets today

EU: A speech by ECB Vice President Luis de Guindos

US: Existing Home Sales Change and a speech by Fed Governor Stephen Miran

GLOBAL: IMF and World Bank Spring Meeting

Global Macro Updates

March inflation, consumer sentiment and factory orders. In March, the core Consumer Price Index (CPI) registered a m/o/m increase of 0.2%, slightly below the consensus expectation of 0.3% and matching February's rise. On an annualised basis, core inflation reached 2.6%, falling short of the anticipated 2.7% and up from February's 2.5%. Headline CPI, which includes all items, rose 0.9% m/o/m, aligning with consensus forecasts and exceeding February's 0.3% increase. The annualised headline rate stood at 3.3%, just below the consensus of 3.4% and up from 2.4% in February.

Energy prices experienced a notable surge, climbing 10.9% in March. Gasoline prices soared by 21.2%, a jump anticipated due to the ongoing conflict with Iran. This was the largest monthly increase recorded since tracking began in 1967. However, preliminary reports suggested that March figures might not fully capture the broader spillover effects from the geopolitical conflict.

Core goods prices increased 0.1%. Notable gains were observed in apparel (1.0%) and new vehicles (0.1%), which offset declines in used vehicles (-0.4%) and medical care commodities (-1.0%). Appliances decreased by 1.3%, following a sharp 3.1% rise in the previous month attributed to tariff impacts. Used car prices, previously expected to contribute to inflationary pressures, did not rise as anticipated.

Core services rose by 0.2%, down from February's 0.3%. Airline fares increased by 2.7%, building on a 1.4% gain in February. Medical care services remained flat after a 0.6% rise the prior month. The Shelter Index advanced 0.3% m/o/m, with rent up 0.2% and owners’ equivalent rent (OER) up 0.3%.

The preliminary April reading from the University of Michigan (UMich) Consumer Sentiment Index dropped to 47.6, well below the consensus of 52.0 and March’s 53.3. This marked the lowest level on record, with sentiment declining broadly across age, income and political affiliations amid heightened concerns regarding the Iran conflict.

Year-ahead inflation expectations surged from 3.8% in March to 4.8% in April, representing the largest one-month increase since April 2025. Long-run inflation expectations also rose, moving from 3.2% to 3.4%, the highest reading since November 2025.

The Current Economic Conditions Index fell to 50.1 from 55.8, while the Index of Consumer Expectations declined to 46.1 from 51.7. The report highlighted a sharp deterioration in sentiment, with expectations for business conditions dropping by approximately 20% and views on personal finances falling by around 11%, largely due to inflation concerns. Buying conditions for major items worsened, and many consumers cited the Iran conflict as a principal factor behind increased economic pessimism.

February factory orders were unchanged, missing the consensus estimate of a 0.2% increase and mirroring January’s flat reading. This followed the preliminary February durable goods orders released earlier in the week, which also came in below expectations and marked the third consecutive monthly decline.

US Stock Indices

Dow Jones Industrial Average -0.56%

Nasdaq 100 +0.14%

S&P 500 -0.11%, with 7 of the 11 sectors of the S&P 500 down

US indices were mixed on Friday as investors awaited US - Iran talks scheduled for the weekend and US inflation data rose due to the jump in energy prices.

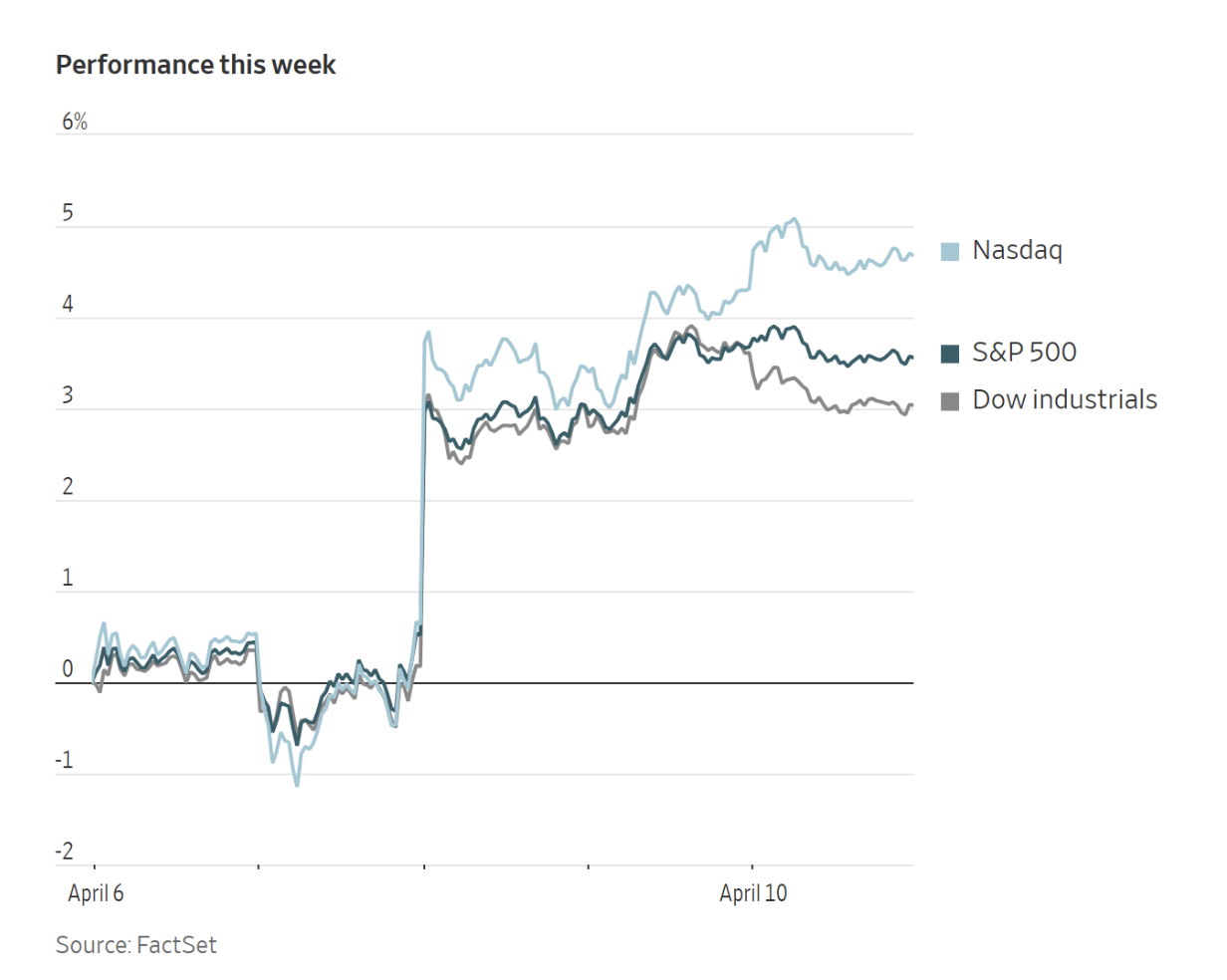

The Dow Jones Industrial Average fell -0.56% to 47,916.57, while the S&P 500 lost its seven days of steam and was -0.11% on Friday. The Nasdaq Composite Index rose +0.35% to 22,902,89. However, for the week, the S&P 500 rose +3.10%, the Dow gained +2.67% and the Nasdaq rose +4.12%, with all three logging their biggest weekly percent gains since November.

In corporate news, cloud infrastructure firm CoreWeave said it struck a deal with Anthropic to supply it with cloud computing capacity. As a result, CoreWeave’s shares rose more than thirteen percent on Friday. The multi-year agreement, whose financial terms were not disclosed, will bring computing capacity for Anthropic online later this year and help it run workloads for its Claude family of AI models.

This came as Treasury Secretary Scott Bessent and Fed Chair Jerome Powell summoned Wall Street leaders to an urgent meeting on concerns that the latest artificial intelligence model from Anthropic PBC will expose greater cyber risk.

US regulators denied Replimune Group’s skin cancer treatment for a second time.

S&P 500 Best performing sector

Information Technology +0.76%, with Super Micro Computer +8.79%, Broadcom +4.69% and Advanced Micro Devices +3.55%

S&P 500 Worst performing sector

Consumer Staples -1.43%, with Hershey -4.05%, Dollar General -3.36% and Kroger -3.35%

Mega Caps

Alphabet -0.21%, Amazon +2.02%, Apple -0.00%, Meta Platforms +0.23%, Microsoft -0.59%, Nvidia +2.55% and Tesla +0.98%

Information Technology

Best performer: Super Micro Computer +8.79%

Worst performer: Akamai Technologies -16.66%

Materials and Mining

Best performer: Dow +2.55%

Worst performer: Mosaic -2.02%

European Stock Indices

CAC 40 +0.17%

DAX -0.01%

FTSE 100 -0.03%

Commodities

Gold spot -0.34% to $4,747.49 an ounce

Silver spot +0.42% to $75.88 an ounce

West Texas Intermediate -3.40% to $95.63 a barrel

Brent crude -2.10% to $94.44 a barrel

Gold prices experienced a modest decline on Friday, yet concluded the week with gains as the US dollar weakened following the temporary ceasefire between the United States and Iran.

Spot gold fell by -0.34% to $4,747.49 per ounce, marking a weekly increase of +1.54%.

The US dollar declined by -1.49% over the past week, making gold denominated in dollars more affordable for investors holding other currencies.

Spot silver increased by +0.42% to $75.88 per ounce, achieving a weekly gain of +3.95%.

Oil futures ended lower on Friday, marking their most significant weekly decline since 2022, as anticipation grew around upcoming discussions between Iran and the United States that aim to secure a lasting ceasefire.

Crude futures remained close to $100 per barrel amid ongoing hostilities and persistent restrictions on oil transit through the Strait of Hormuz. Concerns about potential supply disruptions in Saudi Arabia continued to influence the market, and prices in the physical market reached record levels.

Brent futures settled at $94.44 per barrel, down by $2.03, or -2.10%. Over the week, Brent contracts fell by -13.41%, following a pronounced selloff after Iran and the US agreed to a two-week ceasefire brokered by Pakistan on Tuesday. This represented Brent’s steepest weekly loss since August 2022.

US WTI crude futures also declined, falling by $3.37, or -3.40%, to close at $94.44 per barrel. The weekly drop of -14.66% was the largest since April 2020, during the pandemic-related lockdowns.

The flow of traffic through the Strait of Hormuz remained at less than 10% of typical volumes, as Tehran cautioned vessels to remain within its territorial waters. Ship-tracking data from Friday indicated that most ships passing through the Strait recently were affiliated with Iran. After talks collapsed over the weekend, President Trump has threatened to blockade the Strait of Hormuz. He told reporters Sunday evening that he ordered the US military to enforce a blockade on the strait from 10 am ET. The US military will implement a blockade of all maritime traffic entering and exiting Iranian ports, but will allow other vessels to transit the Strait of Hormuz if they're not stopping in Iran. The idea is to strangle Iran’s oil revenues and collapse its economy. The measure is also designed to stop Iran from raising revenues by charging safe passage for oil tankers in the vital waterway.

In March, Middle East producers curtailed approximately 7.5 million barrels per day (bpd) of crude oil output due to tightening storage capacity. According to a report from the Energy Information Administration last week, outages are expected to rise to 9.1 million bpd in April.

Despite these challenges, Middle Eastern producers have requested Asian refiners to submit crude oil loading schedules for April and May, preparing for a potential resumption of shipments through the Strait of Hormuz, according to sources familiar with the matter.

On Friday, oil prices stabilised as investors weighed reduced Saudi output against diplomatic progress. The Saudi state news agency reported on Thursday that attacks on the country’s energy facilities have decreased its oil production capacity by roughly 600,000 bpd and lowered throughput on the East-West Pipeline by about 700,000 bpd.

According to Baker Hughes, US energy firms reduced the number of operating oil and natural gas rigs for the third time in four weeks. This week’s decrease brings the total rig count down by 38 rigs, or ~7% compared to the same period last year.

Regarding Russian crude exports, flows remain depressed following recent Ukrainian attacks on the ports of Ust-Luga, Primorsk and Novorossiysk. For the week ending 5 April, Russian exports increased w/o/w but are still down by more than 1.0 million bpd compared to two weeks prior.

Note: As of 4 pm EDT 10 April 2026

Currencies

EUR +0.15% to $1.1719

GBP +0.25% to $1.3458

Bitcoin +1.31% to $73,209.84

Ethereum +2.02% to $2,255.50

The US dollar declined on Friday, marking its most significant weekly loss since January.

The euro appreciated by +0.15% on Friday, resulting in a weekly gain of +1.77%, and closed at $1.1719. The British pound also strengthened, advancing +0.25% on Friday and finishing the week up +2.04% at $1.3458.

The Japanese yen fell -0.21% to ¥159.29 per dollar on Friday, but recorded a modest weekly increase of +0.17%. The US dollar index decreased by -0.10% on Friday, and was -1.49% lower for the week.

Fixed Income

US 10-year Bond +5.9 basis points to 4.340%

German 10-year Bund +7.3 basis points to 3.061%

UK 10-year gilt +9.5 basis points to 4.774%

US Treasury yields advanced on Friday following the release of inflation data, which indicated a significant rise in prices consistent with market expectations. Investors also monitored developments ahead of anticipated peace talks between the United States and Iran scheduled for the weekend.

The Labor Department reported that the Consumer Price Index (CPI) increased by 0.9% last month, marking the largest monthly gain in nearly four years. Over the twelve months through March, CPI rose 3.3%, in line with economists’ forecasts. These figures reflect the impact of the ongoing Iran conflict, which has driven up oil prices, alongside persistent tariff pressures.

Market reaction was relatively muted. Yields initially dipped before reversing course and climbing, as the rise in inflation had largely been anticipated by investors. Yields continued to rise after the University of Michigan’s Surveys of Consumers revealed that its Consumer Sentiment Index plunged to a record low of 47.6 this month, down from 53.3 in March and below the consensus estimate of 52.0. The survey pointed to expectations of further inflationary pressures in the coming year.

The yield on the US 10-year Treasury note rose +5.9 bps to 4.340%, finishing the week up +2.0 bps. At the longer end, the yield on the 30-year Treasury bond increased +3.2 bps to 4.917%, but ended the week nearly unchanged, declining -0.1 bps.

The two-year Treasury yield, closely tied to expectations for the Fed funds rate, gained +3.7 bps to 3.810%. Despite this increase, it was down -2.3 bps for the week, marking its second consecutive weekly decline.

The US Treasury yield curve, measured by the spread between two- and 10-year notes, widened to 53.0 bps, up 4.3 bps from the previous week’s 48.7 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 6.9 bps of rate cuts in 2026, in contrast with the 1.2 bps of rate hikes priced in a week ago. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 1.0% probability.

On Friday, German 10-year government bond yields registered a weekly increase, despite experiencing their sharpest single-day drop in years on Wednesday. This volatility occurred as tensions surrounding the ceasefire between Washington and Tehran intensified ahead of an anticipated meeting between US and Iranian officials in Pakistan.

The yield on the German 10-year government bond climbed +7.3 bps to reach 3.061%, resulting in a total weekly gain of +6.6 bps.

The German two-year yield, highly sensitive to inflation and ECB rate expectations, rose +8.8 bps to 2.609%. Nevertheless, it recorded their second consecutive weekly decline, falling -0.7 bps last week. On the long end of the Bund curve, the 30-year yield rose +8.1 bps to 3.587%, culminating in a weekly rise of +11.3 bps.

Money markets projected an ECB deposit facility rate of 2.6% by year-end, up from the current 2.0%, signalling the likelihood of two rate hikes and a 40% probability of a third increase.

The Italian 10-year government bond yield increased +5.7 bps to 3.830%. In late March, yields reached 4.142%, marking the highest level since July 2024, before declining by -4.5 bps last week.

The yield spread between Italian government bonds and German Bunds narrowed to 76.9 bps, down from 88.0 bps the previous week.

Note: As of 4 pm EDT 10 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.