What is the bond market repricing?

What to look out for today

Companies reporting on Tuesday, 19 May: Home Depot

Key data to move markets today

JAPAN: GDP

EU: A speech by ECB Chief Economist Philip Lane

UK: Average Earnings, Claimant Count, Employment Change, ILO Unemployment Rate and a speech by BoE Deputy Governor for Financial Stability Sarah Breeden

US: Pending Home Sales and a speech by Fed Governor Christopher Waller

GLOBAL: G7 Meeting

Global Macro Updates

Debt on the agenda. The global fixed-income market is enduring one of its most severe selloffs in years. The 30-year US Treasury yield has climbed to 5.127%, its highest level since June 2007, while 30-year German Bund yields have reached a 15-year peak and Japanese 30-year yields have surged to their highest since the maturity was first issued in 1999. Headlines have been quick to attribute the selloff to fiscal anxieties due to swelling deficits in the UK, Japan and the US. While those concerns are far from unfounded, the more immediate explanation might lie elsewhere: investors have broadly concluded that central banks will tighten monetary policy regardless of whether an entrenched inflationary spiral has yet taken hold.

The catalyst is the conflict in Iran, which has sent oil and energy prices surging and transmitted price pressures deeply into global supply chains. April data confirm the magnitude of the shock, as US producer prices (PPI) jumped 1.4% m/o/m, and the annual PPI rate rose to 6.0%, the largest annual gain since December 2022, driven primarily by a 7.8% monthly spike in energy costs. Consumer prices followed, with CPI rising to 3.8% y/o/y in April, its fastest pace in nearly three years. These figures left little room for the Fed to maintain its prior posture of cautious patience. Markets now price a 53.5% probability of a Fed rate hike this year.

The ECB and the BoE face an analogous predicament. A Bloomberg news survey of economists published on 11 May confirmed that the ECB is expected to deliver at least two quarter-point hikes in 2026, with a June move viewed as virtually certain. The BoE is similarly seen raising borrowing costs two to three times this year. Crucially, policymakers have acknowledged they will act preemptively, before second-round effects such as broader wage pressures or entrenched inflation expectations can be fully assessed.

The fiscal narrative, however, cannot be dismissed as cleanly as some market participants might suggest. It is true that the spread between 30-year and 2-year yields across the US, eurozone and UK remains below one percentage point, and that currency volatility, as measured by the JPMorgan G7 Volatility Index, has declined since March rather than spiking, as one might expect if a full-blown sovereign crisis were underway. The Fed's 10-year term premium has risen consistently this year to 0.70 percentage points this year, yet much of the bond selloff has been concentrated in short-dated paper most sensitive to rate expectations, not duration. These can be legitimate reasons to temper the fiscal alarm in the near term, until they are not.

Additionally, there is another unsettling possibility. Global yields are surging on rate expectations, but compounding debt dynamics may be writing a longer, darker chapter. Fiscal sustainability and monetary tightening are not separate stories, but compounding ones. Real 30-year yields in the US are already hovering near 2.85%, at multi-year highs. At those levels, refinancing costs on already-stretched sovereign balance sheets become genuinely burdensome over time. Japan's debt dynamics, long managed only by the suppression of domestic yields, face increasing stress as the global rate environment shifts. In the US, a fiscal outlook already under pressure could deteriorate further if a prolonged energy shock depresses growth while simultaneously requiring tighter policy. The bond market may not be penalising fiscal credibility outright today, but in an environment where inflation expectations are themselves unanchored, the line between a monetary repricing and a fiscal reckoning is thinner and more fragile than the current spread data alone would imply.

US Stock Indices

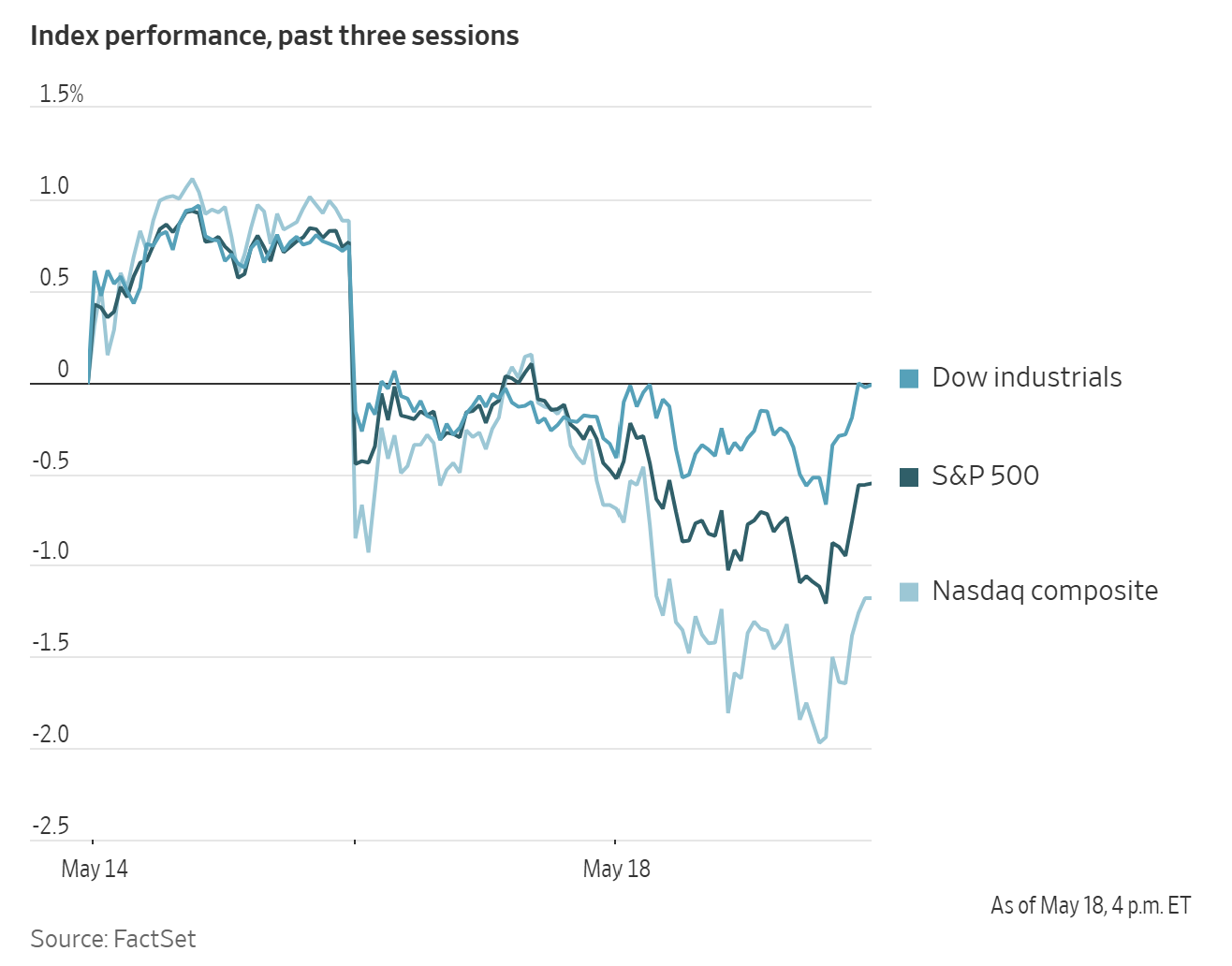

Dow Jones Industrial Average +0.32%

Nasdaq 100 -0.45%

S&P 500 -0.07%, with 4 of the 11 sectors of the S&P 500 down

On Monday the Nasdaq Composite was -0.51%, or 134.41 points lower to 26,090.73. The S&P 500 was -0.07%, or down 5.45 points to 7,403.05. The Dow Jones was +0.32%, or 159.95 points higher, to 49,686.12.

In corporate news, NextEra Energy agreed to combine with rival Dominion Energy in a transaction that would create a $420 billion power group, reflecting strong electricity demand driven in part by AI data centres. According to the Financial Times, the deal would rank as the fourth-largest of all time and would create a US utility company serving more than 10 million homes and businesses from Florida to Virginia. NextEra said on Monday it would pay the equivalent of nearly $76 per share for Dominion in an all-stock transaction that values Dominion’s equity at roughly $67 billion, representing a 23% premium to Friday’s closing price. The implied Enterprise Value (EV) is nearly $124 billion, including $56.7 billion of debt. Dominion shareholders will receive 0.8 NextEra shares for each common share, leaving NextEra investors with 74.5% of the combined company. Dominion shareholders will also receive a quarterly dividend before closing and a $360 million cash payment upon completion of the transaction. NextEra added that the combined group would have 130GW of large-load requests in its pipeline from major power consumers, including AI data centres, while approximately 80% of revenue would continue to come from regulated operations.

Shares of Regeneron fell more than 9% after the company said late on Friday that a late-stage clinical trial of a melanoma treatment had failed to meet its objectives.

A jury rejected Elon Musk’s claims that OpenAI, under Sam Altman’s leadership, had abandoned its public-interest mission by evolving into a for-profit business, finding that Musk had waited too long to bring the case.

The US Supreme Court declined to hear appeals from six pharmaceutical companies seeking to overturn the Medicare drug price negotiation programme, which has generated billions of dollars in discounts on leading treatments.

Publicis Groupe agreed to acquire LiveRamp Holdings for ~$2.5 billion in cash, representing a 30% premium to the company’s closing share price on 15 May. The deal implies an enterprise value of $2.2 billion, including acquired net cash of $379 million, and is expected to contribute to Publicis’s headline profits. LiveRamp CEO Scott Howe will remain in his role and report directly to Publicis CEO Arthur Sadoun, while the company will continue to apply its standard pricing and data collection practices.

S&P 500 Best performing sector

Energy +1.81%, with Baker Hughes +3.25%, SLB +3.20% and Valero Energy +3.10%

S&P 500 Worst performing sector

Information Technology -0.97%, with Corning -6.91%, Seagate Technology -6.87% and Enphase Energy -6.05%

Mega Caps

Alphabet -0.05%, Amazon +0.27%, Apple -0.80%, Meta Platforms -0.49%, Microsoft +0.38%, Nvidia -1.33% and Tesla -2.90%

Information Technology

Best performer: Cognizant Technology Solutions +9.82%

Worst performer: Corning -6.91%

Materials and Mining

Best performer: Amcor +2.18%

Worst performer: FMC -4.38%

Corporate Earnings Reports

Posted on Monday, 18 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Baidu reported Q1 2026 results with revenue of 32.08 bn yuan vs 31.49 bn yuan estimate. Driven by 13.6 bn yuan from core AI-powered businesses while adjusted profit per ADS reached 12.06 yuan vs 11.84 yuan expected, adjusted operating profit hit 3.81 bn yuan vs 3.34 bn yuan estimated and adjusted EBITDA came in at 5.95 bn yuan vs 5.23 bn yuan forecast. Cloud computing demand strengthened while advertising remained weak and US communications regulators flagged security risks for Chinese tech firms.

European Stock Indices

CAC 40 +0.44%

DAX +1.49%

FTSE 100 +1.26%

Commodities

Gold spot +0.61% to $4,565.52 an ounce

Silver spot +2.44% to $77.81 an ounce

West Texas Intermediate +1.50% to $107.25 a barrel

Brent crude +0.09% to $109.31 a barrel

Gold edged higher on Monday, supported by a weaker US dollar.

Spot gold was up +0.61% at $4,565.52 per ounce, after hitting its lowest since 30 March.

The dollar fell -0.31% against major currencies, making greenback-priced gold more affordable for buyers holding other currencies.

Spot silver rose +2.44% to $77.81 per ounce.

US crude futures advanced on Monday, with WTI rising $1.59, or +1.50%, to $107.25 per barrel after gaining more than three percent in the previous session. The June contract is scheduled to expire on Tuesday. Brent crude was also modestly higher, up 10 cents, or +0.09%, at $109.31 per barrel.

Trading in crude and refined products remained highly volatile, largely driven by developments related to Iran. Both WTI and Brent pared their overnight gains following reports that the US had agreed to waive sanctions on Iranian oil during a negotiation period, although that report was later denied by US officials.

A senior US official told Axios that Iran must move beyond symbolic gestures and engage in substantive, detailed discussions regarding its nuclear programme, warning that failure to do so could lead to military escalation.

The US blockade has left the Kharg Island loading terminal inactive for a tenth consecutive day. US Central Command also stated that 85 commercial vessels had been redirected away from entering or exiting Iranian waters.

Earlier in the afternoon, US Treasury Secretary Bessant said the US would grant an additional 30 days of sanctions relief for Russian oil already in transit.

Official data released overnight showed that China’s refinery throughput in April fell to its lowest level since August 2022.

Over the weekend, Ukrainian drones reportedly struck or approached a Russian refinery in Moscow, while video footage appeared to show a fire at the Durykino oil pipeline station in the Moscow region.

The Department of Energy said a record 9.9 million barrels were released from the Strategic Petroleum Reserve last week.

In after-hours trading, oil prices moved lower following comments from the US President on Truth Social. He said that, at the request of Gulf states including Saudi Arabia, Qatar and the United Arab Emirates, a planned military strike on Iran scheduled for today had been postponed because serious negotiations were underway.

Note: As of 4 pm EDT 18 May 2026

Currencies

EUR +0.29% to $1.1657

GBP +0.82% to $1.3429

Bitcoin -2.38% to $77,049.45

Ethereum -3.82% to $2,136.23

The US dollar weakened against most major currencies on Monday as investors assessed whether the Iran conflict was likely to ease in the near term and whether persistently high oil prices could prompt central banks to maintain a tighter policy stance.

The currency had strengthened last week as Treasury yields rose sharply on concerns that higher energy costs would feed into consumer inflation and reinforce expectations of monetary tightening.

The euro rose +0.29% to $1.1657, while sterling gained +0.82% to $1.3429. The dollar index fell -0.31% to 98.96, after recording its strongest weekly performance in three months last week.

The Japanese yen weakened -0.02% against the dollar to ¥158.79 per dollar, marking its lowest level since 30 April.

Japanese authorities intervened several times in late April and early May, helping to support the currency, although the yen has since surrendered much of those gains.

Separately, a government source with direct knowledge of the discussions told Reuters on Monday that Japan is likely to issue debt to help finance an additional budget aimed at limiting the economic impact of the Middle East conflict.

Fixed Income

US 10-year Bond -0.3 basis points to 4.593%

German 10-year Bund -1.8 basis points to 3.152%

UK 10-year gilt -9.0 basis points to 5.092%

Yields on longer-dated Treasury notes climbed to their highest in over a year in overnight trading before easing back, amid a global market selloff in longer-dated bonds driven by war-related inflation concerns.

The yield on the 10-year Treasury note climbed to 4.659% in overnight trading, its highest level since February 2025. It has since retraced its gains and was -0.3 bps lower on the day at 4.593%.

The 30-year Treasury bond yield was up +0.7 bps at 5.127%. It reached its highest level in over a year earlier in the day.

The US Treasury yield curve measuring the spread between yields on two- and 10-year Treasury notes was at 53.4 bps, 1.3 bps wider than Friday.

The shorter-dated two-year Treasury note yield, which typically moves in step with interest rate expectations for the Fed funds rate, was down -1.6 bps at 4.059%. It earlier climbed to 4.105%, its highest in 14 months.

The Treasury Department is slated to auction 20-year bonds on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 13.4 bps of rate hikes in 2026, higher than the 5.5 bps priced in a week ago. Fed funds futures traders are now pricing in a 1.2% probability of a 25 bps rate hike at June’s FOMC meeting, compared to a 2.9% probability of a rate cut last week.

Eurozone bond yields were broadly steady on Monday in volatile trading, following last week’s wider global bond selloff.

The yield on Germany’s 10-year bond fell -1.8 bps to 3.152%, after reaching a fresh 15-year high on Friday following a +12.5 bps rise to its highest level since May 2011.

Italian 10-year government bond yields were little changed, edging -0.1 bps lower to 3.929% after earlier touching their highest level in six weeks, leaving the spread over bunds at 77.7 bps.

Movements in shorter-dated bonds were more pronounced. Germany’s 2-year yield fell -3.8 bps to 2.712%, while the 30-year yield edged -0.3 bps lower to 3.673%.

In the UK, 10-year gilt yields fell -9.0 bps on Monday, after rising on Friday by their largest daily increase since April 2025 amid mounting political uncertainty and growing pressure on Prime Minister Keir Starmer to resign.

Looking ahead, UK April PMIs are due on 20 May, while eurozone PMI data will be released the same day.

Note: As of 4 pm EDT 18 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.